Palantir Technologies (PLTR +2.99%) is widely regarded as a top-tier artificial intelligence (AI) company, but opinions are mixed on whether it is a good investment. In prior years, the bulls have won the argument, as Palantir's stock has delivered solid returns year after year.

But the bears may be right in 2026 -- the stock has declined by about 20% year to date. Overall, it's more than 30% below the peak it touched late last year. Yet even in the wake of that contraction, there are concerns that its valuation is too high.

For a while, the company's valuation was of little concern to some investors; all that mattered to them was its growth. Palantir had a similar sentiment, but investors seem to be shifting toward a more profit-focused mindset. Fortunately, Palantir is highly profitable and generates loads of cash each quarter.

The problem is, the stock is valued at a high price-to-earnings ratio. But does this pose further risks to the stock price, or are high premiums likely to remain the status quo for Palantir over the long term?

Image source: Getty Images.

Palantir is expensive, no matter how you look at it

Palantir rose in popularity because it was one of the first businesses to seamlessly incorporate AI agents. It's best known for its AI-powered data analytics software, but the ability for clients to automate processes with its AIP product took its offering to the next level, and revenues soared.

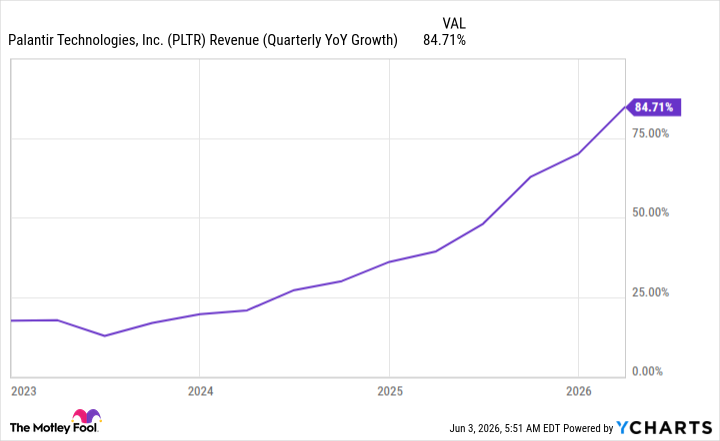

PLTR Revenue (Quarterly YoY Growth) data by YCharts.

Palantir is still in a growth acceleration phase of its business, but once its growth starts to slow, that could cause further problems for the stock. Wall Street analysts are already projecting just that: The consensus among those covering Palantir is for revenue growth to come in at 80% in Q2 and 69% in Q3.

Palantir has long outperformed expectations, so its growth deceleration may or may not arrive in the near term, but it will happen eventually. And rapid growth is the one thing keeping this stock priced at premium valuations.

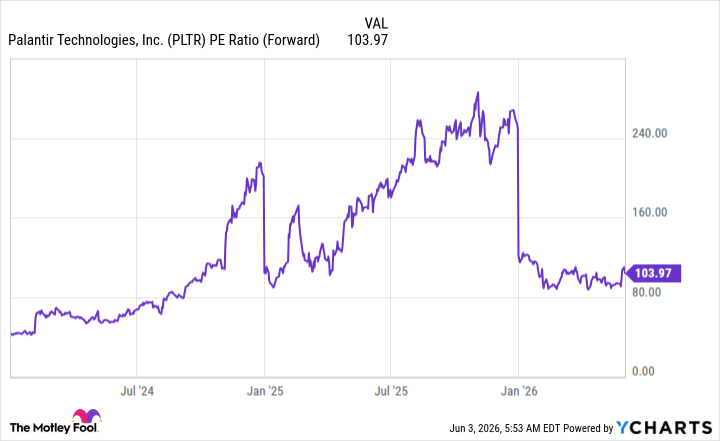

PLTR PE Ratio (Forward) data by YCharts.

Last year, it traded at above 200 times forward earnings. Now, it's down to 104 times forward earnings, but that still makes it one of the most expensive stocks on the market. Normally, when it comes to fast-growing tech stocks that are trading at expensive valuations, some of the upside baked in is based on the assumption that the company can improve its profit margins. Most companies that are growing their top lines as fast as Palantir is are not yet optimized for profitability. However, during its latest quarter, Palantir had a net income margin of 53% -- a level that ranks in the upper tier of publicly traded companies.

NASDAQ: PLTR

Key Data Points

That suggests that it lacks the ability to expand margins much further, which means that in order to justify its current market cap, Palantir must grow its way into it. A valuation in the range of 30 to 40 times forward earnings would be reasonable for a business like Palantir -- to hit that, it will have to increase its earnings by 150% to 200% even after hitting 2026's expected growth. That's a lot to ask, especially after the initial phase of AI deployment has wrapped up.

I think that represents a major risk for the stock, and before investing here, investors should consider how much growth Palantir would have to put up from here simply to be reasonably valued at today's share price.