The growing adoption of artificial intelligence (AI) is driving a sharp increase in demand for cybersecurity software as enterprises seek to protect their valuable data and digital applications. CrowdStrike's (CRWD +0.10%) Falcon platform is one of the industry's most popular all-in-one solutions, and its capabilities continue to expand to meet the needs of the AI era.

Last Wednesday evening, CrowdStrike posted an incredibly strong set of operating results for its fiscal 2027 first quarter (which ended April 30), yet its stock plummeted 14% by market close on Friday.

Simply put, while the long-term opportunity for cybersecurity vendors is obvious, CrowdStrike is trading at sky-high valuations, and the result is an uncomfortable risk vs. reward situation for investors.

Image source: Getty Images.

Falcon protects businesses entering the AI era

The cybersecurity industry was more fragmented in the past, meaning businesses had to buy products from different vendors to achieve adequate protection. This left holes in their defenses and resulted in slower incident responses. Those sorts of lags are now more dangerous than ever because malicious actors are using AI to rapidly find and exploit vulnerabilities. That's why unified solutions like Falcon are the only way forward.

Enterprises can choose from 33 Falcon modules (products) to build their ideal cybersecurity solution. Plus, with the Falcon Flex subscription option, they can set a fixed budget and then add or remove modules as their needs change without negotiating a new contract with CrowdStrike. This makes it a strong option for businesses that are gradually adding AI to their operations, because this technology requires a different approach to security.

Next-Gen Identity Security is one of Falcon's newer modules. It enforces a zero-standing-privileges policy when humans and AI agents interact with an enterprise's sensitive internal data, regularly revoking their access and forcing them to reauthenticate. This ensures hackers can't hijack control of a single AI agent and gain indefinite access to that data, reducing the likelihood of a catastrophic breach.

NASDAQ: CRWD

Key Data Points

Then there is Falcon's AI Detection and Response (AIDR) module, which uncovers unauthorized AI applications or agents running within an enterprise's network. It also tracks every input and output across all trusted AI applications in the organization, so it can identify malicious prompts that might be entered by someone trying to steal data or orchestrate a breach.

AIDR experienced a whopping 250% sequential increase in its annual recurring revenue during the company's fiscal 2027 first quarter. CrowdStrike CEO George Kurtz said he has never seen a product scale that quickly, and he believes it could become one of the company's largest-ever opportunities.

Revenue growth just accelerated

CrowdStrike generated $1.39 billion in revenue in the first quarter, topping management's forecast of $1.36 billion. That was a 26% year-over-year increase, marking an acceleration from the 23% growth the company delivered in the fourth quarter, so the business is carrying real momentum.

It also ended fiscal Q1 with a record $5.5 billion in annual recurring revenue, up 24%. Falcon Flex made an incredible contribution, with its annual recurring revenue almost doubling to $1.9 billion. In other words, more new and existing customers are opting for the flexible subscription option.

The strong top-line results prompted management to increase its full-year annual recurring revenue guidance by $50 million to $6.54 billion (at the midpoint of the forecast range), but none of this was enough to prevent a sharp drop in CrowdStrike stock after the earnings report.

CrowdStrike's high valuation makes it a tough investment

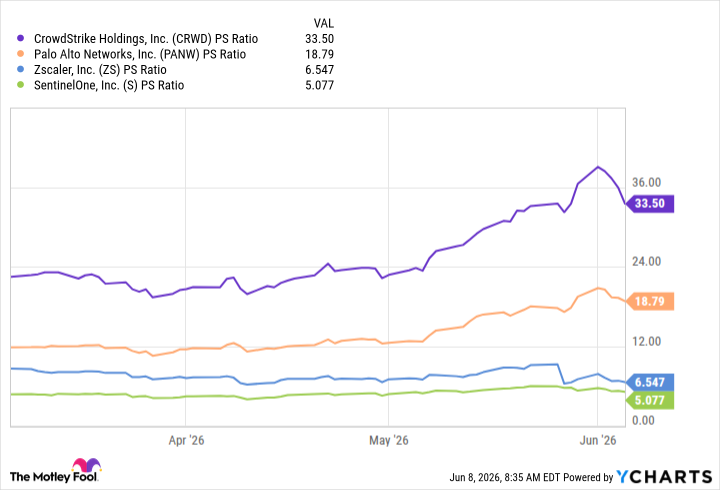

Despite its recent 14% dip, CrowdStrike's price-to-sales (P/S) ratio remains sky-high at 33.5 -- significantly more expensive than its core rivals.

CRWD PS Ratio data by YCharts.

As a result, it might be difficult for CrowdStrike stock to rally to new highs in the short term, so investors looking for gains in the next few months might want to steer clear. However, there could still be a case for owning CrowdStrike for the long term, as the company believes it can grow its annual recurring revenue by 263% to $20 billion by the end of fiscal 2036.

If the company achieves that goal, its stock might actually be relatively cheap on a forward basis. Plus, that would still only be a fraction of what CrowdStrike believes is a $325 billion long-term opportunity in the cybersecurity industry.

In summary, whether investors should consider buying CrowdStrike stock depends entirely on their time horizon.