Nvidia (NVDA -2.86%) has a great investing track record, which makes sense considering its position in the tech world. Because of the central role it plays in the artificial intelligence (AI) industry, it has to interact with many companies to ensure that its products are compatible, and it even forms partnerships when the situation is right. One company it recently promoted was Marvell Technology (MRVL -4.64%). Nvidia CEO Jensen Huang is so bullish on Marvell that he recently asserted that it was on course to be the next trillion-dollar company. Given that it currently sports a $270 billion market cap, it has a long way to go to reach that point, but if it does reach the $1 trillion level, that would be a tremendous result for those who invest in it now.

Since Huang's comments on Marvell at the start of June, the stock has skyrocketed by more than 40%. The question investors must answer is whether that jump captured all of the stock's near-term upside, or if it has more room to rise.

Image source: Getty Images.

Marvell has a range of products

Marvell has two primary product lines that are of interest to AI investors. First is its networking and connectivity hardware; Nvidia has ensured that its own products are compatible with Marvell's here, because those networking solutions are so popular in data centers. Second, it designs ASICs, or application-specific integrated circuits, and it's a bit of a head-scratcher as to why Nvidia would endorse those. ASICs are custom chips that are designed to handle a narrow range of workloads. They are nothing new, but they're becoming a lot more popular in the AI computing world, as they allow companies to tailor a chip to the specific type of workload it is expected to see during its useful life. They can thus be manufactured at lower costs and operate with greater efficiency than Nvidia's graphics processing units (GPUs), which can handle a far broader range of computing tasks. So such hardware poses a direct competitive challenge to Nvidia's primary business.

NASDAQ: MRVL

Key Data Points

This makes an endorsement from Nvidia even more impressive, as it speaks highly of a company that's both a partner and a competitor.

Marvell is clearly involved in an industry that's expected to grow at a rapid pace over the long term, but does that make it a buy?

In the first quarter, Marvell's revenue rose 28% year over year. While that would be a strong growth rate for a company in most sectors, it's a bit slow for a business that's involved in AI. Wall Street expects Marvell's revenue to rise at a 41% pace for the rest of 2026 and a 45% pace next year. That would be a solid improvement, but even that may not be enough to justify its current price tag.

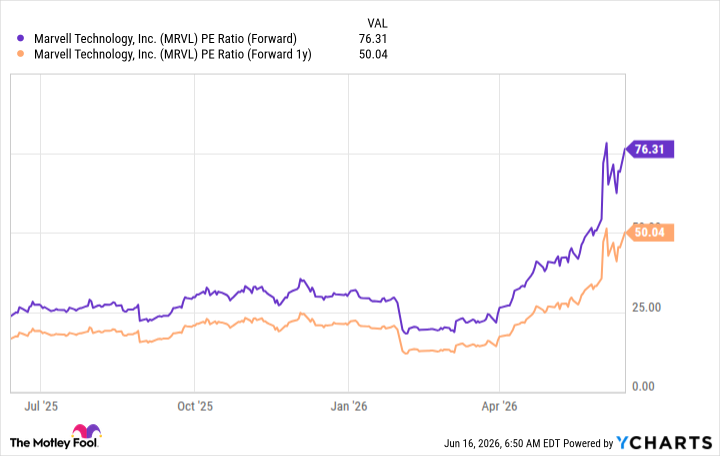

Trading at 76 times forward earnings and 50 times next year's expected earnings, Marvell is far from a cheap stock.

MRVL PE Ratio (Forward) data by YCharts.

Compare that to plain old Nvidia, which trades for 24 times forward earnings and 17 times next year's expected earnings, and Marvell doesn't seem like such a good investment following its recent share price spike.

While Marvell may be a trendy pick right now, it's going to need several years of strong earnings growth to reach the $1 trillion club, and it will be some time before that happens (if it ever does). I think investors shouldn't stray too far from the basics on this one, and should stick with a stalwart like Nvidia instead.