In the artificial intelligence (AI) world, Nvidia has a dominant market position. Its GPUs are best in class and have powered countless AI workloads, and will continue to do so for some time. However, GPUs have incredible capabilities that aren't always utilized when deployed in settings where workloads are repetitive and predictable. That's why some AI hyperscalers are turning to custom AI chips to minimize their run costs.

None of the AI companies can do this on their own, which is why they partner with companies like Marvell Technology (MRVL +3.88%) and Broadcom (AVGO +1.71%). These two companies help their clients design custom AI chips, known as application-specific integrated circuits (ASICs), alongside networking equipment to connect everything together.

That's a booming business, but which of these two stocks is the better buy? Let's find out.

Image source: Getty Images.

AI is a new business unit for each company

Both Marvell and Broadcom have other products beyond their AI-focused businesses that get investors excited.

Broadcom offers a wide range of products, including mainframe hardware and software, virtual desktop software, and cybersecurity solutions. Marvell is a bit more focused on the chip side of the industry, and also makes networking chips for mobile devices, controller chips for solid-state drives, and a host of other products.

NASDAQ: MRVL

Key Data Points

However, AI is the big focus for both businesses (and for investors). There is a huge market opportunity available, and each is looking to seize it.

The biggest takeaway from their custom AI chip businesses is the customers. Marvell's primary ASIC customers are Amazon and Microsoft, which use Marvell to help design their Trainium and Maia chips, respectively. Broadcom's client base includes Alphabet, Meta Platforms, OpenAI, and Anthropic. Those are some of the biggest names in AI, but which is the biggest boost?

NASDAQ: AVGO

Key Data Points

I'd have to give this segment to Broadcom, because of all of the custom AI chips out there, the most successful is Alphabet's Tensor Processing Unit (TPU). Time will tell whether other offerings from Amazon and Microsoft can catch up to the success Alphabet has had with a TPU, but until it does, I think Broadcom gets the nod here.

Winner: Broadcom

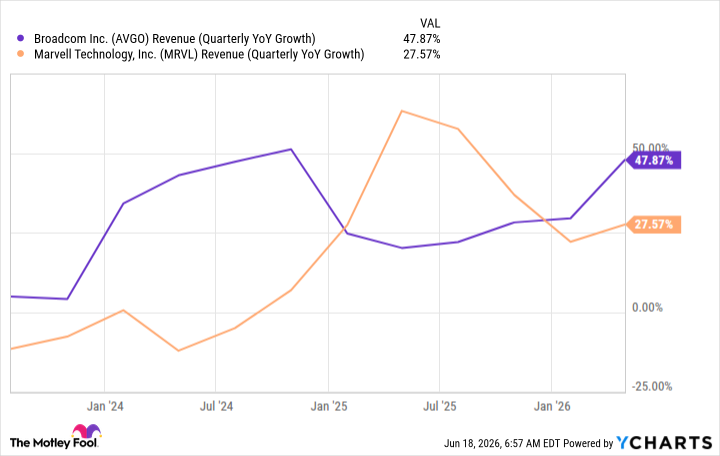

Broadcom is growing faster

From a growth standpoint, Broadcom also has the edge.

Data by YCharts.

It's not by much, but Broadcom is barely beating Marvell. But what about the future? For the fiscal year 2026, ending in October 2026, Wall Street expects Broadcom to deliver 66% revenue growth. For fiscal year 2027, that figure is similar, at 62%. For Marvell, whose fiscal year 2027 ends in January 2027, analysts expect 41% growth in fiscal year 2027, followed by 45% growth in fiscal year 2028.

That's a pretty clear-cut win for Broadcom, as Wall Street is far more bullish on its future.

Winner: Broadcom

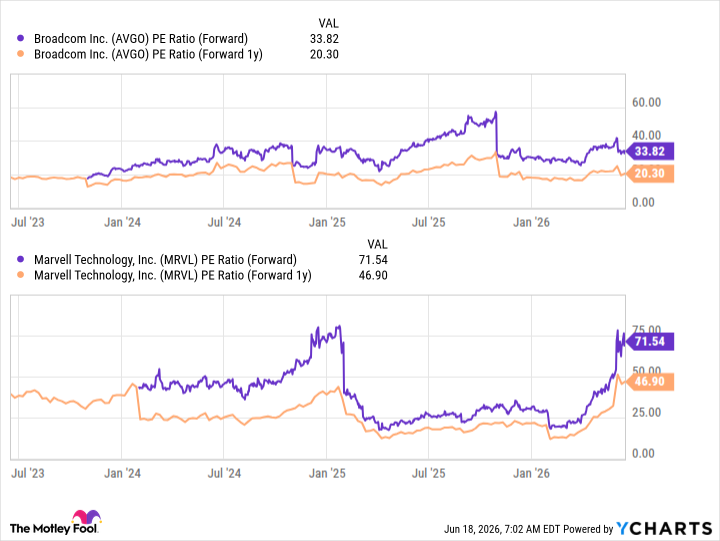

The stock valuation is the final factor

Despite Broadcom holding a lead, if its valuation is too high, then Marvell can easily be the better buy. Although Marvell's outlook isn't as strong as Broadcom's, it's still good enough to warrant considering it as an investment. However, the market has gotten far too bullish on Marvell's stock, mainly due to Nvidia's recent endorsement.

Data by YCharts.

Broadcom trades at 34 times forward earnings, which is lower than Marvell's valuation when fiscal 2028 earnings estimates are used. That's just far too high a price to pay for a stock when Broadcom has a stronger client base, a better flagship custom AI chip, and strong revenue growth projections.

Broadcom is the runaway winner here, and I think it should easily outperform Marvell over the next five years.

Winner: Broadcom