The memory market is in the grip of what may be its worst supply shortage ever. Contract prices for conventional DRAM soared as much as 95% in the first quarter of 2026, and NAND flash prices have jumped sharply quarter after quarter, all because the artificial intelligence (AI) build-out is devouring every chip the industry can make.

When investors look for a way to play this tailwind, they usually reach for Micron Technology (MU -0.44%). But Micron is far from the only winner.

Three other storage companies -- SanDisk (SNDK -3.68%), Western Digital (WDC -3.81%), and Seagate Technology (STX -4.71%) -- are cashing in too, and their latest results show just how much. But which one has the cleanest exposure to the shortage, and the longest runway, as prices keep climbing?

Image source: Getty Images.

SanDisk: closest to the shortage

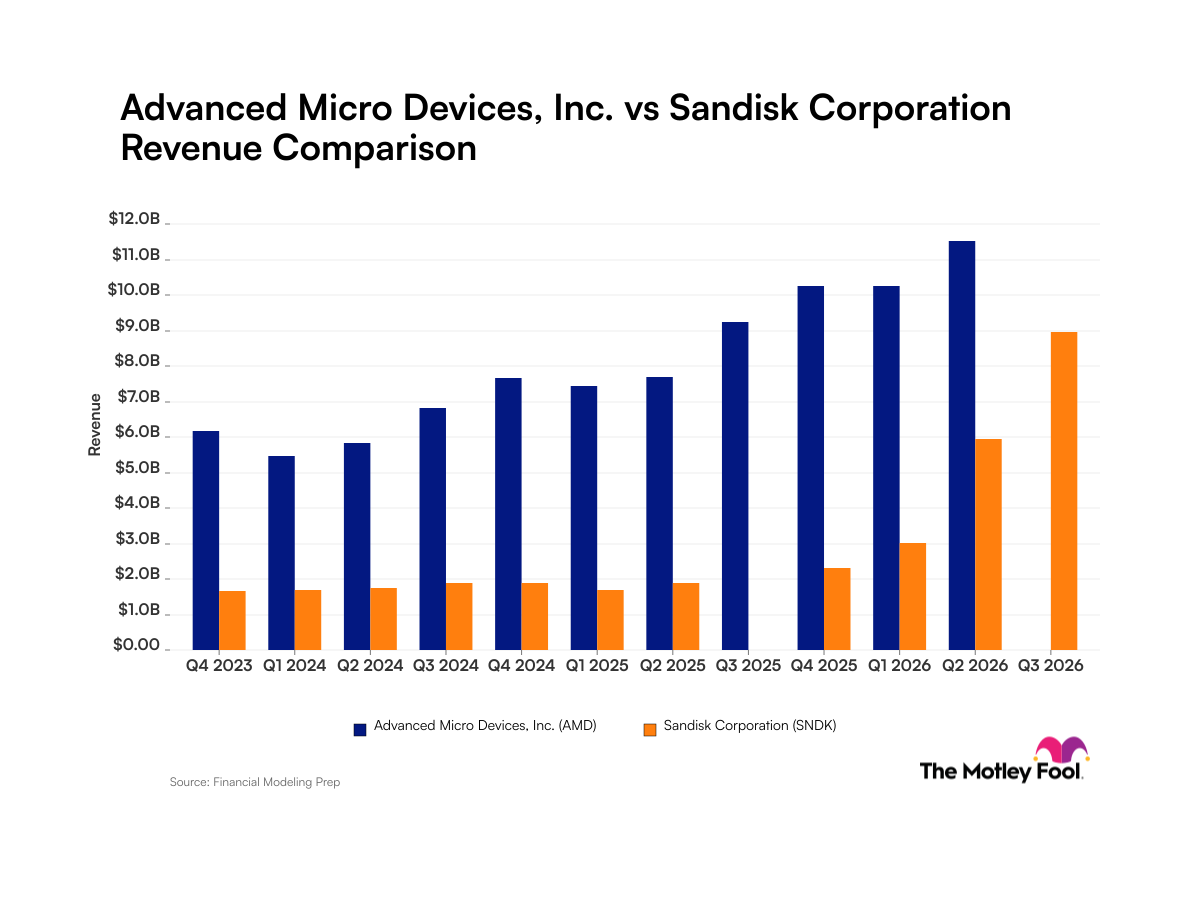

Of the three, SanDisk has the most direct exposure to the squeeze. It makes NAND flash, the chips inside the solid-state drives whose prices are spiking -- and the numbers it posted in its latest quarter are staggering.

SanDisk's fiscal third-quarter revenue (the period ended April 3, 2026) reached $5.95 billion, up 97% from the prior quarter and 251% from a year earlier. The data center business led the way, with revenue tripling -- up 233% sequentially to $1.47 billion, about a quarter of the company's total. Higher prices fell almost straight to the bottom line, pushing non-GAAP (adjusted) gross margin to about 78%, and SanDisk threw off nearly $3 billion in free cash flow during the quarter.

NASDAQ: SNDK

Key Data Points

What makes the runway unusually durable for a NAND maker is how SanDisk is now selling, locking customers into multiyear deals.

"We are also advancing to a new business model built on multi-year customer engagements backed by firm financial commitments," said SanDisk CEO David Goeckeler in the company's fiscal third-quarter earnings release.

At about 75 times earnings, the stock looks expensive. But trailing earnings barely capture the surge, with management guiding for $30 to $33 in adjusted earnings per share in the fiscal fourth quarter alone -- a huge quarterly figure for a stock that is trading at $2,200 as of this writing.

The catch is that these are cyclical-peak profits, and the stock has already soared more than 800% in 2026 as of this writing.

Western Digital: riding the spillover

Western Digital doesn't make memory at all -- it makes hard disk drives (HDDs). But the same shortage is working in its favor. With solid-state drives now prohibitively expensive, cloud and AI customers are buying every high-capacity hard drive they can find, and Western Digital has effectively sold out its 2026 capacity.

NASDAQ: WDC

Key Data Points

The result was a fiscal third quarter in which revenue rose 45% year over year to $3.34 billion, with adjusted gross margin reaching about 51%.

"Virtually every AI workload, from training, inference, agentic AI to physical AI, creates data that is stored persistently and cost-efficiently on HDDs," said Western Digital CEO Irving Tan in the company's fiscal third-quarter earnings release.

The shares are up more than 290% in 2026 as of this writing.

Seagate: record margins and a dividend

Seagate's new Mozaic platform, built on a technology that packs more data onto each disk, is lifting margins just as demand outstrips what the industry can supply.

NASDAQ: STX

Key Data Points

Seagate's fiscal third-quarter revenue rose 44% year over year (and 10% from the prior quarter) to $3.11 billion, with adjusted gross margin of 47% -- a record for the company. Seagate also produced $953 million in free cash flow, which it used to pay down debt and keep funding its dividend.

The stock trades at nearly 100 times earnings, but that figure reflects profits still climbing out of an industry downturn rather than the earnings power implied by the current boom. Like its peers, Seagate has surged, more than tripling in 2026 as of this writing.

Which has the best exposure?

All three are cashing in, and all three now have years of demand locked up. But they aren't equally exposed to the shortage driving all of it.

Western Digital and Seagate are riding a knock-on effect: because memory turned scarce and expensive, buyers flooded back to hard drives. It's a powerful and surprisingly durable tailwind -- but an indirect one. SanDisk, by contrast, makes the very chips whose prices are climbing, so it arguably captures the shortage most directly, and its shift to multiyear contracts gives it unusual visibility for a cyclical business.

I believe this makes SanDisk the purest way to play the memory shortage among the three. Just don't lose sight of the risk that comes with it: SanDisk's profits, and its stock, are riding a cycle that won't keep climbing forever.