Palantir Technologies is among the top vendors of artificial intelligence (AI) software solutions, and it has been witnessing phenomenal growth in revenue and earnings in recent quarters due to the healthy spending on its offerings by both commercial and government customers.

However, Palantir stock has retreated 33% so far in 2026, primarily due to concerns about its expensive valuation. On the other hand, shares of cloud communications platform provider Twilio (TWLO +24.89%) have jumped by 38% this year, as the demand for the company's AI-focused solutions is now driving stronger revenue and earnings growth.

What's more, Twilio trades at a significantly cheaper valuation than Palantir. Let's look at the factors driving Twilio's growth and check why this AI stock is primed for more gains.

Image source: The Motley Fool.

Twilio's AI products are encouraging its customers to spend more money

Twilio's cloud communications platform enables its clients to remain in touch with their customers through voice, text, chat, video, email, and other channels. The company's application programming interfaces (APIs) help customers integrate these communication channels into their applications.

NYSE: TWLO

Key Data Points

Twilio's APIs have helped clients replace traditional contact centers with a cloud-based platform, reducing the costs and overhead of operating physical call centers. And now, Twilio is providing its clients with AI tools and solutions to enhance their customer service and drive stronger sales.

Twilio noted on its April earnings call that a digital marketing agency used its voice, messaging, and voice AI solutions to build an AI agent. The client witnessed a 39% increase in bookings in three months following the deployment of this agent, generating an additional $8.4 million in revenue. Not surprisingly, Twilio is now witnessing stronger spending by its clients, who can now gain better insights into customer behavior with the help of AI.

Using AI tools is helping Twilio customers increase product adoption, make appointments, reduce fraud attempts, and increase click rates, among other things. As a result, Twilio's dollar-based net expansion rate increased to 114% in the first quarter, up by seven percentage points from the year-ago period.

This metric compares Twilio's total revenue for the quarter to revenue from the same customer cohort in the year-ago period. A reading of more than 100% means that Twilio's existing customers have increased their adoption of its offerings or have increased the usage of its products. Getting more business from existing customers is ideal for Twilio's bottom line, as it won't have to spend additional money on customer acquisition.

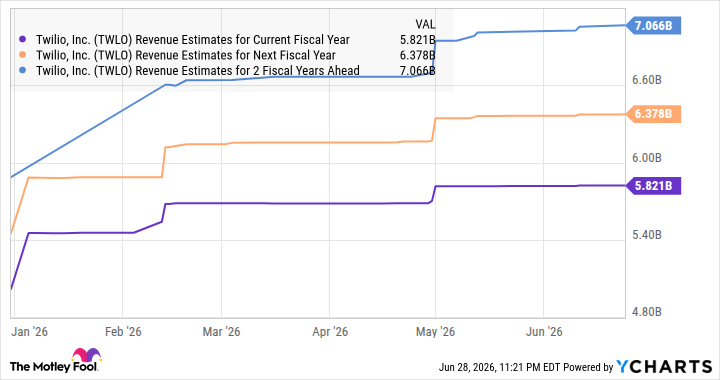

This explains why Twilio's earnings per share increased by 31.5% year over year in Q1 to $1.50. That was well above the 20% jump in its top line to $1.41 billion. What's more, Twilio is now expecting stronger growth in 2026. It now expects revenue to increase by 14% to 15% in 2026 to $5.8 billion, up from the prior expectation of 12%. It is also expecting a stronger jump in both earnings and free cash flow.

However, don't be surprised to see Twilio increase its guidance further as the year progresses. That's because the integration of AI in cloud communications applications will boost its addressable market to $158 billion by 2028. It was earlier anticipating $119 billion in revenue from its core communications and data platform markets.

So, it is easy to see why analysts have been becoming bullish about Twilio's top-line growth prospects.

Data by YCharts

The attractive valuation and earnings growth prospects suggest more upside for investors

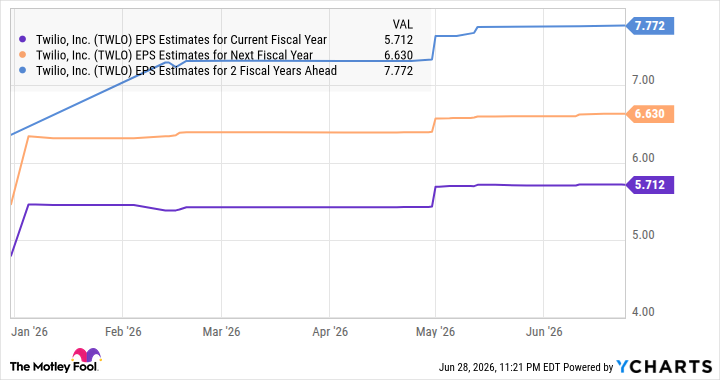

The improvement in Twilio's revenue growth and the company's ability to win more business from existing customers explain why analysts expect healthy, double-digit earnings growth.

Data by YCharts

It won't be surprising if it exceeds those expectations. But even if Twilio's earnings increase in line with consensus estimates and it trades at 34 times earnings after three years (in line with the tech-focused Nasdaq-100 index's earnings multiple), its stock price could reach $264 (based on the $7.77 earnings per share estimate seen in the above chart). That's a potential 37% jump from current levels.

Given that Twilio is trading at 34 times forward earnings, investors are getting a good deal on this growth stock. Also, its sales multiple of 5.7 is almost in line with the Nasdaq Composite index. So, investors looking to capitalize on the AI software market's growth can consider buying Twilio as it offers a nice mix of growth and value.