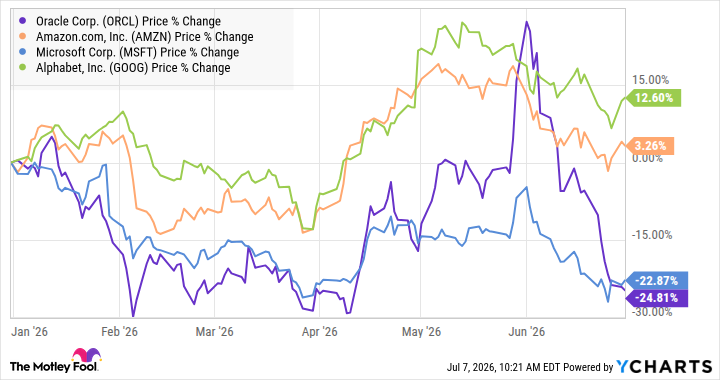

Not all hyperscalers are made equal, and some are made less equal than others. Moving on from shamelessly misquoting Orwell, there's a key point here, and it's demonstrated in the chart below. Oracle (ORCL -0.64%) stock declined 24.8% in the first half of 2026, according to data from S&P Global Market Intelligence. Microsoft (MSFT +2.54%) declined by a similar amount, but, interestingly, both Amazon.com and Alphabet, the owner of Google, are in positive territory. Here's why.

Oracle's decline in 2026

There are two themes to explore here. First, the reality is that forecasts for the construction of artificial intelligence (AI) infrastructure have increased throughout the year. That's the main reason AI infrastructure companies like Vertiv and GE Vernova have significantly outperformed the market and the hyperscalers, like Oracle, whose increased capital spending requirements have pressured their stocks in 2026.

The second reason for the decline stems from something it shares with the other hyperscaler in negative territory, Microsoft: significant exposure to the AI model and technology company, OpenAI.

Oracle, Microsoft, and OpenAI

Microsoft is a major investor in OpenAI, owning about 27% of the company as of the end of March, and earlier in the year, management disclosed that "Approximately 45% of our commercial RPO balance is from OpenAI. "As for Oracle, it and OpenAI signed a landmark $300 billion deal in September 2025. The five-year deal starts in 2027 , in which Oracle will build out AI infrastructure and supply OpenAI with computing power.

Image source: Getty Images.

It was initially well received by the market, but, as the chart below shows, bond markets immediately began pricing in an increased risk of default for Oracle's bonds. For reference, credit default swaps are derivatives that insure the buyer from the risk of a bond's default. They are priced in basis points (whereby 100 basis points equals 1%), so the 170bps pricing of its 5-year bond currently means it costs $17,000 to insure $1,000,000 of Oracle's 5-year debt.

Assuming a 40% recovery rate, the bond market estimates a 2.8% annual default probability and a cumulative default probability of 13.4%. However, the key point is the increase in implied probability after the OpenAI deal.

Data source: S&P Global Market Intelligence. Chart by the author.

Why OpenAI is causing concern

Investors are questioning OpenAI's financial projections, with the company expecting to burn through more than $650 billion in cash through 2030. Moreover, its management expects to generate $280 billion in revenue by 2030 after ending 2025 on an annualized revenue run rate of just $20 billion.

While OpenAI may well hit the revenue target and ultimately start generating cash in 2030, , there's a long way to go, it's a competitive market, and it's far from clear whether its AI models will add the value to justify the infrastructure build-out of Microsoft and Oracle. That's why both stocks declined significantly in the first half.