Space Exploration Technologies (SPCX +15.83%), AMD (AMD -1.21%), and Palantir Technologies (PLTR +10.32%) may seem like an odd grouping of companies. But I have a good reason to consider them together: They're all incredibly overvalued.

While that may sound like a shocking statement, after digging into each stock, that's the reality, and investors sitting on them may want to consider swapping them out of their portfolios for some more reasonably valued counterparts in their industries.

So, just how pricey are they? Let's take a look.

Image source: Getty Images.

SpaceX

Although SpaceX just went public a few weeks ago, I think it's one of the most overvalued stocks on the market. But that's only if you value the company based on what it has already done.

The majority of SpaceX investors are buying into the stock because of what it could achieve under Elon Musk's leadership. That's a fair investment thesis, and it's what has allowed Tesla to remain one of the largest companies in the world despite its business struggles over the past few quarters. If that's your angle, I'm not going to argue, but it doesn't alter the fact that SpaceX's business as it stands now does not justify the company's valuation.

NASDAQ: SPCX

Key Data Points

SpaceX hasn't reported earnings results as a public company yet, so the only information investors have to go on is from its IPO presentation. According to that, in 2025, SpaceX generated $18.7 billion in revenue and reported negative net income. So if we value the company using 2025 sales, that would price SpaceX at 92 times sales.

Even if SpaceX could snap its fingers and become instantly profitable with a 45% profit margin (its stated long-term goal), that would value the stock at 204 times earnings. That's an incredibly expensive stock, and with 2025 revenue growth coming in at only 33%, those numbers don't jibe.

That's not to say SpaceX cannot overcome this with future growth, but even then, a lot of hoped-for growth is already priced into the stock, so I'm avoiding it.

AMD

AMD stock has risen by about 150% so far in 2026. While some of that gain was earned, the rest of it is a real head-scratcher.

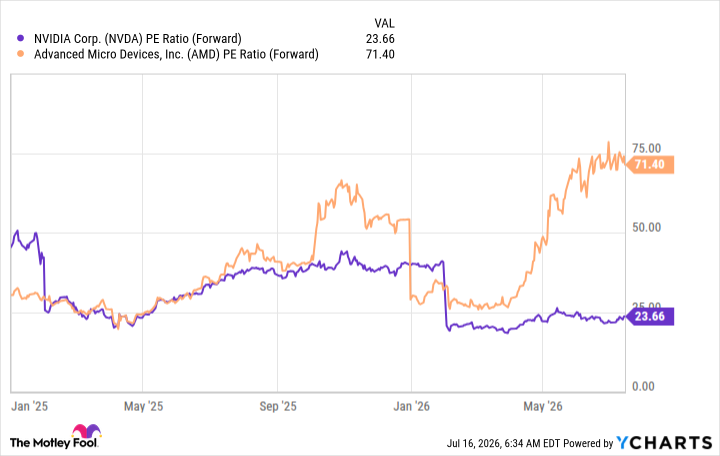

AMD is constantly compared to Nvidia, as these two compete against each other in many product lines, but the most important arena for both right now is the data center market. Nvidia's data center division is far larger and growing much faster than AMD's, which makes it odd that AMD is now valued at such a premium to Nvidia.

NVDA PE Ratio (Forward) data by YCharts.

With Nvidia's growth this fiscal year expected at 82% versus AMD's 43%, the justification for AMD's premium over Nvidia is a mystery. As a result, I think investors would be far better off selling AMD stock and scooping up Nvidia while it's as cheap as it is.

Palantir Technologies

Lastly, there is Palantir, which has been a popular AI stock pick over the past year. Its business continues to excel, and it grew by a strong 85% in the past quarter.

But the problem is that a growth deceleration could be on the way. Wall Street estimates that Palantir's growth rate, which is projected to be 72% this year, will decline to about 45% next year.

NASDAQ: PLTR

Key Data Points

While that's still rapid, it's not enough to warrant the 90 times forward earnings valuation the stock carries. That's an expensive premium for any stock, even one growing as fast as it is today. If Palantir's growth rates start to decline at any time, the market could send its shares lower, as a ton of anticipated success is already priced into the stock.

That makes it a bit of a precarious investment, and I think there are far better AI stocks to invest in than Palantir right now.