Last week, Federal Reserve Chair Janet Yellen discussed the future of economic outlooks and monetary policy. While overall there were few surprises, there was one comment that caught my attention:

The timing and pace of interest rate increase ought to, and I believe will, respond to unfolding economic development ... if those were to improve faster than the committee expects it would be logical to expect more rapid increase in the fed funds rate.

While the comment itself is certainly logical, it also seems to indicate the slower the economy improves the longer mREITs -- like Annaly Capital Management (NLY +1.19%) and American Capital Agency (AGNC +1.49%) -- benefit from low and stable borrowing costs.

This is something that's become even more apparent based on Tuesday's comments from the CEO of the Philadelphia Federal Reserve, Charles Plosser. His speech was on taking a more "rules-based" approach to monetary policy, rather than a "discretionary" approach. Plosser explained quite simply that in a rule-based system decisions are more predictable because they're guided by a set of concrete principals. This is opposed to a discretionary approach where decisions are made at the will of the Fed.

Plosser went on to note that a rules-based system creates better communication, leading to more transparency and greater accountability. Ultimately, it's an approach that does a much better job keeping businesses and investors in the loop on policy.

Currently, the Fed does have economic indicators in place that, when met, should spark interest rate "lift off." But even if inflation reaches the 2% personal consumption expenditure (PCE) inflation target and labor markets continue to improve, the Fed still has discretion over if and when it will raise rates.

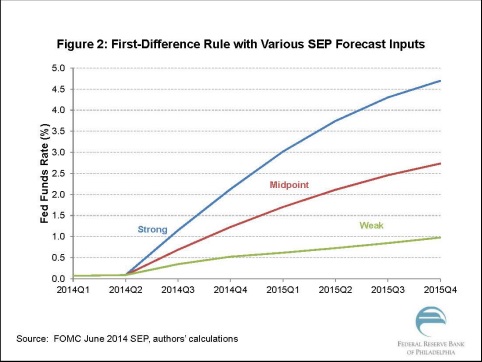

With that said, Plosser has constructed a chart (below) using a series of complex economic models that predict -- as long at the Fed stays true to its targets -- how interest rates may be adjusted based on economic progress. The blue line suggests the "best case scenario" for economic recovery, green is weakest improvements, and red represents the Fed's midpoint projections.

Historically, mREITs have performed poorly during times of rapidly increasing interest rates. This is because increases in the federal funds rate raises borrowing costs, narrowing the difference between asset yields and interest expenses (borrowing costs) -- and, ultimately, puts pressure on profitability.

Therefore, as the chart above shows, the faster the economy improves the more rapid interest rates are likely to rise and the worst the scenario seems for Annaly and American Capital Agency.

Now what?

Annaly and American Capital Agency's hedge portfolios -- derivative contracts used to secure borrowing costs -- have certainly been adjusted since the first quarter. However, it's fair to assume based on Chair Yellen's remarks -- rates will likely stay low longer -- that both companies have moved into more midterm (2-3 years) and longer-term (5-plus years) duration hedge contracts. While eliminating shorter-term duration (0-1 year), which creates an opportunity to take advantage of currently lower funding costs.

Therefore, both companies' portfolios are designed for rates to rise moderately over the next few years -- which matches up best with the red (midpoint) line in Plosser's chart. So, neither company is necessarily rooting "against" the U.S. economy, but rather is better prepared for more steady, compared to rapid or sluggish, growth.

Last word

Ultimately, the pace at which rates rise has little effect on my thesis for either company. Whether interest rates rise in late 2014 or sometime in 2015, mREITs are going to face environmental challenges in the near future. The Fed has been as forthright with their potential actions as anyone could hope, and both Annaly and American Capital Agency should be, and I believe are, as prepared as they can be for what lies ahead.