American Capital Agency (NASDAQ: AGNC) is a better dividend stock than Chimera Investment (NYSE: CIM), and I'm going to tell you why.

Chimera is exposed to credit risk -- risk that its assets will default -- and American Capital Agency has almost none. While American Capital Agency has more interest rate risk, I believe this is more manageable. And lastly, because mortgage real estate investment trusts are driven by their management teams, I trust Gary Kain and American Capital Agency more than Chimera.

Default risk

Investing in higher-credit quality residential mortgage loans, Thornburg Mortgage seemed unlikely to have high numbers of defaults. But in came 2008, and Thornburg became one of several companies to file for bankruptcy as the mortgage market disintegrated into 2009.

On the other side of this story is Annaly Capital Management. Because they invested solely in "agency" securities guaranteed against default from Fannie Mae and Freddie Mac, they rode out the storm and made a killing following the financial crisis.

I take this trip down memory lane because it relates very well to the risk and reward you're getting with Chimera and American Capital Agency. Because Chimera invests roughly 35% of its portfolio in assets that are not guaranteed against default – though at times the percentage has been much higher – they can earn a higher yield on assets. On the other hand, though they receive a lower yield on assets, investing exclusively "agency" securities American Capital Agency is much better protected from a mortgage market downturn like we had in 2008.

Because I believe that the past tends to repeat itself, I rather hold the business that is better protected against the swings in the health of the mortgage market.

Interest rate risk

This isn't to suggest that American Capital Agency isn't taking any risk. To make up for that fact their assets have a lower yield than Chimera, American Capital Agency borrows more heavily against their equity, also called leverage, to magnify returns.

The process works similar to a mortgage on a house. If you put $10,000 down on a $100,000 house, you have a leverage ratio of 10. If the house were to appreciate by 10%, you would earn a 100% return on your equity. The risk is that it works exactly the same if the value depreciates.

For American Capital Agency, it's not the value of a house, but the market value of their currently owned securities. When prevailing long-term interest rates rise, the market value of their securities decreases in value. In the chart below you can see how sharply rising interest rates can effect American Capital Agency's stock price.

While the chart above looks bad, and it is, the company has recently been reducing leverage and shortening the duration of their assets – assets that have a shorter life mature faster and aren't as effected by rising rates – American Capital Agency can mitigate some of these losses.

Most important, while rising mortgage, or long-term, interest rates are a killer for American Capital Agency, what goes up normally comes down, and the company performs extremely well in a falling rate environment. In fact, as rates fell between 2009 and 2011, American Capital Agency created a total return of 158%.

Management

With a greater diversity of assets and a better immunity to rising interest rates, to this point, you could certainly make a case for Chimera being the more enticing business. However, when it comes to management, at least for me, the picture is much more lopsided.

As fellow Fool analyst John Maxfield has said, "Nothing screams bad investment more than an accounting fiasco." In 2011, Chimera had to restate nearly all of its fillings because they overstated net income by a whopping 66%. Despite this issue recently being resolved, as an investor, I want to see Chimera prove they can stay on track before I would consider investing.

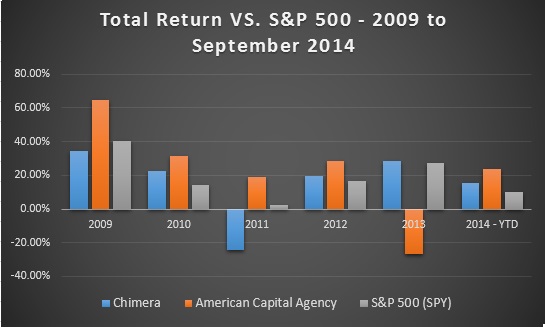

My opinions of the management team at American Capital Agency are quite the opposite. President and CIO Gary Kain, does a fantastic job clearly explaining even the most complex mREIT strategies, his foresight and expertise helps to keep the company ahead of the curve, and has lead the company to outperform both Chimera and the S&P 500 four of the last five years -- and is also currently beating the market.

Bonus: better valuation

As an asset-based business, the price-to-book ratio -- or total assets minus total liability divided by market cap -- is a useful indicator of a mREIT's relative value. Chimera presently has a price-to-book value of 0.95, while American Capital Agency sports a 0.84. This means American Capital Agency's assets are trading for roughly $0.84 on the dollar.

Ultimately, while I think Chimera has big upside, and its ability to target various asset classes and operate with lower leverage gives it an advantage in a rising interest environment. Over time, though, I favor safer assets and stronger management, and for those reasons I find American Capital Agency the better dividend stock.