There is arguably no other sector of the stock market in which the interests of investors and management are more out of whack than with mortgage real estate investment trusts. Companies are surprisingly open about this fact.

Here's an example from American Capital Agency's (AGNC +1.49%) 2013 annual filings: "[W]hile our stockholders bear the risk of our future equity issuances ... diluting the value of their stock holdings in us, the compensation payable to our Manager will increase as a result of future issuances of our equity securities."

The idea that management can boost its pay by diluting company stock absolutely blew me away, and this isn't unique to one company. Rather than being paid for performance, most mREITs are externally managed. This means managers receive a flat fee based on total shareholders' equity.

However, because mREITs pay out 90% of their earnings in dividends, they can't grow equity like normal companies. Instead, the only way for management to increase its pay is for the value of assets to increase -- something executives have little control over -- or by issuing new shares of stock.

Everything about this smells, and I was sure I would find managers carelessly issuing stock despite its damaging effect on shareholders. I was wrong.

Buffett explains it best

In Warren Buffett's 2014 letter to Berkshire Hathaway shareholders, he compares the stock market to a moody farmer yelling out how much he would pay for Buffett's farm. Since Buffett knows exactly what the farm is worth, when the farmer bids too much he sells, and when the bid is too little he holds.

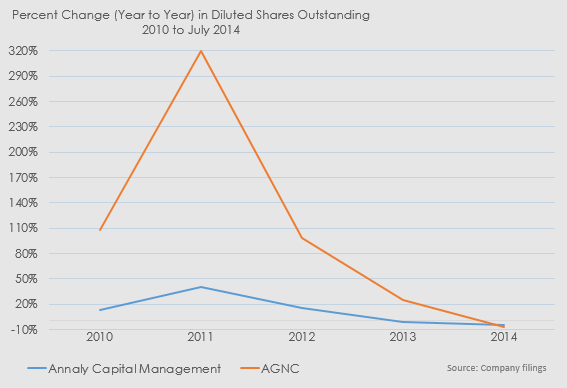

Over the past five years, there have been some good and bad opportunities for Annaly Capital Management (NLY +1.19%) and American Capital Agency to sell new shares of stock.

At the top left, both companies were trading above book value. This means investors are willing to pay more for the company than it was actually worth. While selling new shares means each individual share represents a smaller percent of the company, Annaly and American Capital Agency can use the cash to buy assets that grow earnings. Essentially, you own a smaller piece of a more profitable pie.

In the bottom right, the companies are selling for less than they were worth. In this case, shareholders receive a greater benefit from companies buying back shares. This reduces share count and increases value per share.

Conflict of interest

While it's great for shareholders, buying back shares reduces a company's total equity and decreases management's compensation. Surprisingly, management of both REITs have proven more than willing to take one for the team.

Going public in 2009 -- as opposed to 1997 for Annaly -- is why American Capital Agency's share growth looks dramatically larger.

With that said, when issuing shares was in everyone's best interest, 2010 to the end of 2012, share count grew. However, as Annaly and American Capital Agency slipped below book value the selling of shares came to an immediate halt. In fact, in the first two quarters of 2014, Annaly and American Capital Agency's total shares declined 5% and 7%, respectively.

What it all means

This is a story about misperceiving incentives. On the surface, management has seemingly everything to gain from neglecting the interests of shareholders. In the long term, however, investors will not continue to fund a company that doesn't take care of its shareholders. So, perhaps, the interests of management and investors are more aligned than I assumed, and this is something shareholders should feel good about.