Before getting into the discussion of energy and chemical company Occidental's (NYSE:OXY) second-quarter performance, it's probably worth talking just a bit about relative valuation and what that means for buyers versus holders.

Covering as many energy companies as I do, ranging in size from ExxonMobil (NYSE:XOM) to Apache (NYSE:APA) to Bill Barrett (NYSE:BBG) and Brigham Exploration (NASDAQ:BEXP), the "best" idea at any given time is fluid and ever-changing. That's just the way the market works; my opinions about the best companies don't change often, but my opinions on the best stocks at a given time do. That doesn't mean that an investor should hop around from one stock to another on a month-by-month basis; rather, it just means that someone looking to put new money into the sector should find the best opportunity possible at that point in time.

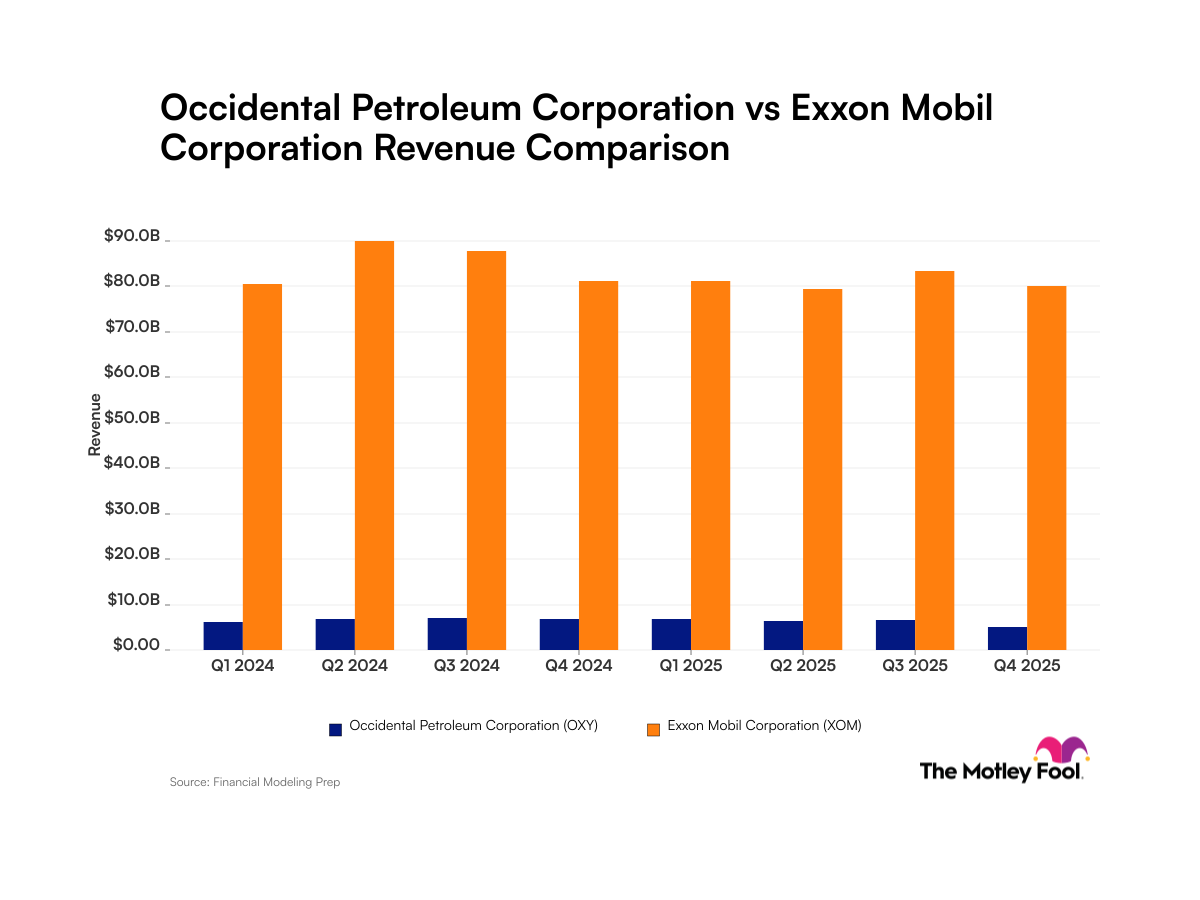

With that out of the way, Occidental had a difficult quarter but a solid one. I wish that the company included more operating information in its financial press releases, but that doesn't change the fact that revenue was up 36% or that core earnings rose more than 50% this quarter. As has been the case for a while now, oil and gas continue to be strong performers, with high realizations (prices) and rising production (up 18% this time around).

Of course, even though Occidental has competitive finding and developing costs and a good global production platform, that's not the most interesting piece of recent news. Rather, this company suffered the wrath of the Ecuadorian government and had a productive asset seized. In response, the company has taken a charge to account for the lost value, but management still seems optimistic that it will someday recover that asset.

In the meantime, Occidental is one of those energy companies that I like well enough as a company, but current valuations aren't quite as enticing on a relative basis. It's not a bad idea to hold, but investors looking to put new money into oil and gas can probably find a better value if they shop around a bit.

For more Foolish thoughts on the energy sector:

- What More Can Occidental Petroleum Do?

- Does ExxonMobil Mark the Spot?

- Apache Continues to Pump Out Value

Let our investing newsletters energize your portfolio. You can check out our entire suite of newsletters by clicking here .

Fool contributor Stephen Simpson has no financial interest in any stocks mentioned (that means he's neither long nor short the shares).