After a midweek reprieve yesterday, stocks added to the week's losses today, as the S&P 500 (^GSPC +1.08%) retreated by 0.8%, while the narrower, price-weighted Dow Jones Industrial Average (^DJI +0.14%) fell 0.6%.

Consistent with the those declines, the VIX Index (^VIX +2.32%), Wall Street's "fear index," rose 10% today, to close at 13.99. (The VIX is calculated from S&P 500 option prices and reflects investor expectations for stock market volatility over the coming 30 days.) Given that the Cypriot circus is in town, it's entirely possible we will see that figure rise between now and Monday, which is the deadline by which the European Central Bank is requiring Cyprus come to an agreement with its lenders.

Stocks for the long run in nine months' time

Jeremy "Stocks for the Long Run" Siegel is bullish on stocks. What gave it away? On CNBC this afternoon, the Wharton School professor raised his year-end target for the Dow to 17,000. (He also said he expects the S&P 500 to rise to 1,700.) Siegel has done some useful work on long-run asset returns -- certainly enough to know that nine-month price targets for equity indexes are better than useless. The random component of stock returns over such a short period absolutely overwhelms any meaningful attempt to make a single-point estimate. Does his forecast even make sense as the average value of a range of outcomes? Let's take a look.

Now, Dow 17,000 at year-end would require a 30% annual rise in the index. Is that possible? Definitely. A 10% rise in year-on-year forward earnings estimates, combined with an 18% rise in the P/E multiple, would do the trick. Is it likely? Let's start with earnings: Given earnings estimates for 2013 that already look extremely bullish, I think a 10% increase from the current base for 2014 estimates is the very most we can hope for.

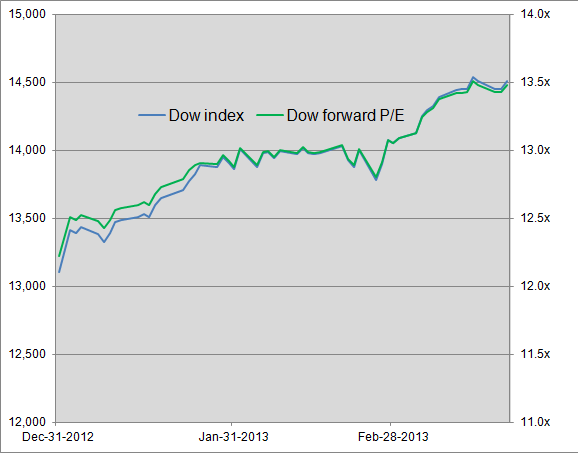

On paper, an 18% rise in the P/E multiple looks easy enough to achieve from current levels and, indeed, as of Wednesday's close, we are better than halfway there, with a 10.3% increase in the P/E. As the above graph shows, that's the factor (ie. valuations) that have driven gains in the index so far this year. Still, that rise has already required a genuine thawing in investor risk aversion that began last June. Whether it can continue may end up depending on decisions taken in Nicosia, the capital of Cyprus, over the next three days.