I'm sure you've heard the saying, "things are not always what they seem." That's what we have with RadioShack (RSH +0.00%). As a value investor, I've wanted to love this stock for a couple of years now; it's constantly showing up on net-net screens, it's in the news as a "dead" company, and rival Best Buy (BBY +3.51%) has managed one of the great turnaround stories in retail.

The two, Best Buy and RadioShack, appeared to be in similar death spirals, and then 2013 came, transforming Best Buy into a new company.

Source: YCharts

I am still a bit skeptical of the 200% run up in Best Buy's stock year to date. But the question remains, why can't RadioShack do the same? All of this has led me to do some deep thinking as it relates to electronics, books, and e-commerce.

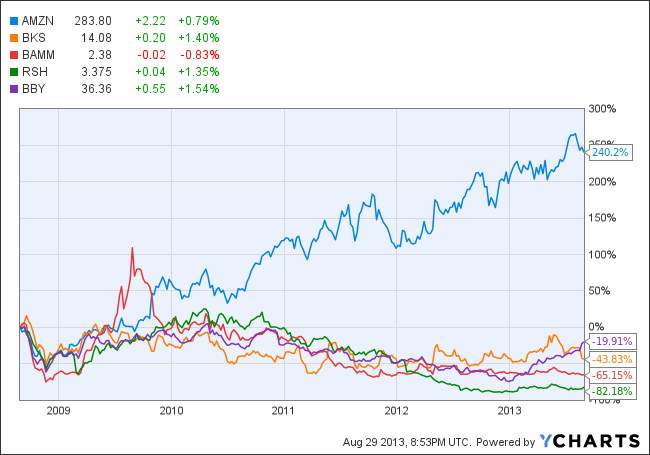

Amazon.com (AMZN 0.73%) has forever changed the book industry. It's doing the same with electronics. Amazon has soared, while the book and electronics retailers have suffered over the past decade.

Source: YCharts

First, Amazon started offering the ability to buy books for cheap online. Then came the ability to read books online and via tablets/e-readers. Now the book industry is struggling to survive. Borders went bankrupt back in 2011, and Books-A-Million has seen its EPS fall from $1.88 in 2005 to a $0.26 loss in fiscal 2013.

I can see the parallels in the electronics industry. Circuit City closed its doors back in 2008, and now RadioShack and Best Buy are left to battle it out in the electronics-retail industry. RadioShack has seen a similar decline to Books-A-Million, with EPS dropping from $2.08 in 2004 to a loss of $2.06 over the trailing 12 months.

But back to why RadioShack can be deceiving. The stock trades around $4.00, but it has $4.33 in cash per share on the balance sheet. Its debt, however, is a tough pill for investors to swallow, with nearly $7.20 per share in debt.

On the other hand, Best Buy may be able to continue muddling through, as it did manage to generate $2.5 billion in free cash flow during fiscal 2012. But RadioShack has negative free cash flow of $111 million and suspended its dividend payment back in 2012. And RadioShack's debt-to-equity ratio is 140%, while Best Buy's is 46%.

Smartphones

So Amazon is killing the Best Buy-RadioShack model by selling laptops and TVs, but there's another problem on the horizon: smartphone saturation. Both Best Buy and RadioShack get around 50% of revenue from the smartphone market. ComScore believes that 60% of Americans already have a smartphone. And as UBS telecom analyst John Hodulik has famously said: "Everybody has got a smartphone."

Yet, the likes of RadioShack and Best Buy are still focusing on smartphones, with Best Buy rolling out small mobile stores. A focus on low-margin smartphones should put further downward pressure on margins. Margins have been on the downhill slide, with Best Buy's operating margin going from 5.4% in 2008 to 4.5% in 2010, and then 2.1% in fiscal 2012. The same is true for RadioShack; its operating margin went from 7.6% in 2008 to -2.7% over the trailing-12 months.

Moody's also has a poor outlook on RadioShack. The corporate rating is down to Caa1. Moody's notes "the overall business strategy of the company to reverse the decline in profitability has not gained any traction. Moody's expects that the 2013 retail operating environment will remain challenging and the increasing price competition within the wireless- mobility sector, including wireless carriers, will continue to pressure RadioShack's profits."

Bottom line

Both of the electronics-retail stocks look incredibly cheap, with Best Buy trading at 0.3 times sales and RadioShack at 0.1 times. Compare this to Amazon's 1.9 times. However, I think both of these retailers have too many headwinds, including a saturation in the smartphone market, which also happens to be a low-margin business for the retailers. Meanwhile, although the valuation appears expensive, I would not be betting against Amazon, especially with Jeff Bezos at the helm.