While PNC (PNC -1.24%) has a market value approaching $40 billion, and more than $300 billion of assets on its balance sheet, there are a wealth of things that fly under the radar about this bank. Let's dive into seven facets that may escape the first glance of any investor.

1. It owns 22% of BlackRock (BLK +0.00%)

Now the world's largest publicly traded investment firm with more than $3.8 trillion in assets under its management, BlackRock actually began as a subsidiary of PNC in 1995. While BlackRock went public in 1999, PNC retains a 22% ownership stake.

Last year, that investment earned PNC $395 million, and contributed to 11% of the bank's business segment net income. This year has brought further gains; BlackRock stock has risen 32%, and PNC has received earnings of $220 million from it through the first six months of 2013, compared to $178 million last year. In fact, while PNC accounts the value of Blackrock at $5.8 billion, the company reports that its actual market value was $9.2 billion last quarter.

2. It's aggressively pursuing expansion in the Southeast

After completing its acquisition of RBC's U.S. retail bank in 2012, PNC began to aggressively push into new markets in the Southeastern part of the country. As a result, it has seen all segments of its business expand in Alabama, Florida, and Georgia, as well as North and South Carolina.

In the Southeast, its Retail Bank has seen its consumer accounts go up 6% over the last year, while average loans have gone up 10%, and its new mortgage originations have gone up 41%. Its Corporate & Institutional Bank has grown clients by 42%. Finally, its Asset Management Group has almost doubled its primary clients added per quarter. Half of them came from referrals in Q2 2013, versus just 19% in Q2 2012, proving that, beyond getting new customers, it is gaining their trust.

3. PNC's automobile loans have ballooned since 2011:

Source: Company Earnings Reports

In 2011, automobile loans represented only 7% of PNC's total consumer loan portfolio. In its most recent quarter, however, they represented 12%, showing that it is growing its automotive lending portfolio much faster than its other types of consumer loans. PNC noted that this gain was the result of an expansion of its sales force, and an increase in relationships with dealers, highlighting its desire to expand this lucrative business.

4. It's aggressively expanding its Corporate & Institutional Banking group

Since 2011, PNC has seen the assets attributable to its Corporate & Institutional Banking group grow 38.5%, from $81 billion, to $112 billion. In the same period, its total assets have only grown by 15%; the assets of all its other business segments combined have only grown 4%.

Many may think of PNC as a consumer-centric bank. If asset size is any indication, however, the company is clearly committed to its corporate clients, which now represent 37% of its assets, compared to just 25% made up of consumers.

5. It has a much lower price-to-tangible book value ratio than its peers

Source: YCharts

Investors apparently aren't willing to pony up the same kind of dough for PNC relative to what they pay for its peers. This is especially odd, considering its returns are similar to those of competitor BB&T, even though it is cheaper relative to its book value. While this may not be an indication to buy PNC, it certainly calls into question why investors are willing to pay more for BB&T.

6. It holds more than $7.5 billion in health-care loans

PNC is one of the only banks that breaks out its commercial loans to include those in health care. While the $7.5 billion top line is certainly high, it has juiced this amount by more than 50% since 2011:

Source: Company Earnings Reports

Considering the health-care industry is poised for major change, PNC could be positioned to become the market leader and see major benefits.

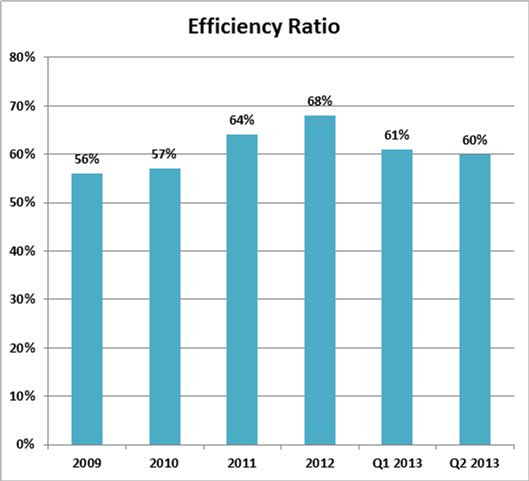

7. It's getting stingier

PNC's efficiency ratio -- expenses divided by revenue, a number you always want to be low -- rose for three years in a row. Yet, through diligent expense management, PNC has watched that number decline dramatically over the last two quarters, which should lead to greater profitability down the road:

Source: Company Earnings Reports

Each of these points should teach you something new, interesting, and encouraging about PNC. While on their own, these facts wouldn't make a case to invest in the company, they are all certainly worth noting as you craft your own investment hypothesis.