Timing the market is often the cause of underperforming the market, and even losing money. However, it's also been said that buying great businesses at good prices is central to long-term market-beating returns. Let's take a look at five stocks that have had a rough month. Are these "falling knives," or is Mister Market just putting great businesses on sale?

Industrial to leisure: No industry is safe

Profits outside the box

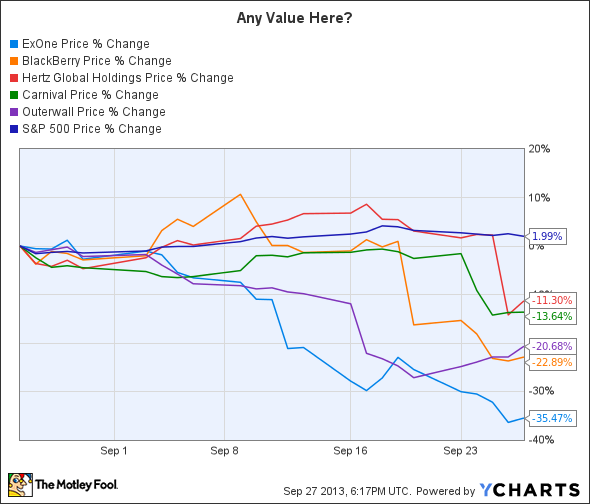

You may not recognize the name Outerwall (OUTR +0.00%), but their more than 40,000 Redbox kiosks, and the tens of thousands of green Coinstar machines are a familiar sight in many grocery and other large retail establishments. The company is projecting continued moderate growth, but updated guidance, revising down for the remainder of the year, has largely been the cause of the decline.

While there are some positives, including the company's plans to buy back up to $100 million in shares, and the expansion into coffee machines, called Rubi via its partnership with Starbucks' Seattle's Best brand, it's tough to predict sustained growth with credit transactions and streaming taking customers away from change machines and physical media. The company's partnership with Verizon, Redbox Instant for streaming video, doesn't get much mention by either company. And with Verizon's recent purchase of the remaining stake in Verizon Wireless from partner Vodafone, it's tough to see Verizon putting much focus on this initiative for the foreseeable future.

From a valuation perspective the trailing P/E ratio is below 12; however, it's still hard to predict outsized, market-beating returns moving forward. A great price for a good company doesn't usually lead to big returns.

Less on leisure

Both Carnival (CCL -0.48%) and Hertz (HTZ +0.00%) are feeling the pinch of reduced consumer spending on travel, and projecting this to continue at least for the remainder of the year. Hertz is down almost entirely on reduced guidance for the remainder of the year. However, as the Fool's Brian Pacampara states in the article, shares are still up over the past year, and richly valued.

Carnival is expecting its business to decline over the remainder of the year, and costs to increase. From the latest earnings release(bold mine):

"Fourth quarter constant dollar net revenue yields are expected to be down 3 to 4 percent compared to the prior year. Net cruise costs excluding fuel and impairments per ALBD for the fourth quarter are expected to be higher by 3.5 to 4.5 percent on a constant dollar basis compared to the prior

year, which is primarily due to increased advertising expenses and costs associated with the previously announced vessel enhancement initiatives."

Declining sales plus increasing costs doesn't equal a great buy.

Object lesson in letting go

BlackBerry (BBRY +6.91%) is done as a public company. Chances are the acquisition by Fairfax Financial for $9 per share will happen. However, there's a valuable lesson that we can learn from what's happened to the once-dominant smartphone maker. Bulls decried the loss of market share as temporary, and that the company was just one phone away from returning to glory. Many pointed to its strong balance sheet, lack of debt, and large cash position as strengths that would see the company through the hard times, and that shares were really just "cheap."

Ignoring the strong evidence that the company's advantages in security for enterprise customers wasn't enough to keep the company relevant led to major losses for long-term shareholders that ignored the writing on the wall. When Warren Buffett stated "our favorite holding period is forever," he didn't say only holding period.

One to buy

Shares of ExOne (XONE +0.00%) are down more than 40% from August's high, but are still nearly double from the IPO price early this year. While this is no stock on "sale," the potential this 3D printing company offers is significant. The Fool's Rich Smith highlighted how a recent "sell" rating by Credit Suisse was partially responsible for pushing shares lower. And where Rich is not convinced that ExOne deserves what is still a very richly valued share price, there are a handful of reasons why the current share price may not be as much of a premium as it appears, from the second quarter earnings release:

- Company guidance is only $48 to $52 million in annual sales this year, double the year before.

- Net losses were reduced by 68% versus the year-ago period, on strong margin and revenue growth. If this continues as projected, next year will be profitable by a large margin.

This is a tiny company with great big potential. Just recognize that it will be a bumpy ride, and start small.

Last thoughts

The real concern with all of these companies is that it's hard to predict revenue and profit growth with any certainty. And without profit and revenue growth, shareholders tend to get left out in the cold. What makes ExOne a notable exception is simply the enormous upside possibility. While it may not be any easier to draw a line from the current company to future returns, if the company does perform even modestly well, the investment could be very rewarding.

And if the growth is as explosive as it could be, we're talking about a life-changing investment opportunity.