Master limited partnerships are pass-through entities, which means they pay out most of their cash to investors and must issue massive amounts of debt and capital to fund growth. Keeping track of this debt often entails looking at long lists of senior notes and maturity dates (like the kind in SEC filings), and quite frankly, if you're not careful, it'll put you to sleep.

That's why we're telling the Kinder Morgan Energy Partners (NYSE: KMP) debt story in three charts instead. To help keep things in context, we'll compare Kinder Morgan's data to two of its peers along the way: Energy Transfer Partners (ETP +0.00%) and Enterprise Products Partners (EPD +0.58%).

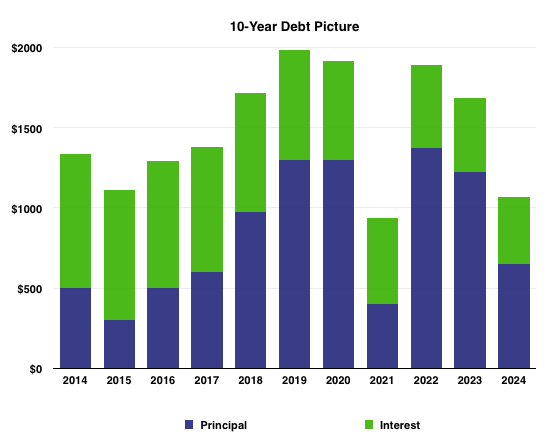

1. 10-Year debt picture

Before we overwhelm ourselves with debt-related computations, we should know exactly what we're dealing with at Kinder Morgan for the next ten years. The chart below gives us just that, detailing the partnership's principal and interest payments per year for the next decade.

The blue bars reflect the amount of principal due each year, while the green indicates how much Kinder Morgan will pay in interest on its fixed rate debt. The one thing this doesn't capture is the partnership's revolving credit facility, or any floating rate bonds it has issued, because those rates may change.

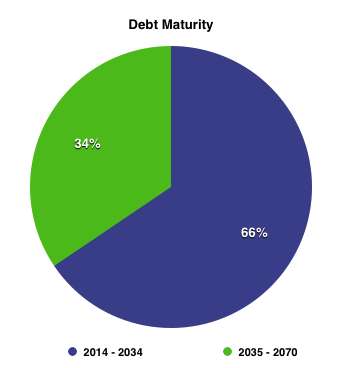

2. Debt maturity

Evaluating when a company's debt matures can tip you off to a couple of things. First, debt that matures decades from now is more desirable than debt that matures tomorrow. This is especially true right now, when many energy companies are spending big-time dollars bringing major infrastructure projects online. Those new projects will be up and running -- and generating cash -- before its bill comes due. The one caveat to this is the impact duration has on interest rates: The longer the maturity, the higher the rate.

Here's how Kinder Morgan's debt breaks down over time:

Source: Company filings

You can see that the partnership doesn't have to start thinking about paying the principal on 34% of its debt load for another twenty years, at least.

Now let's look at the same statistics at Kinder Morgan's competitors. Enterprise Products Partners beats Kinder Morgan in the debt maturity category, as 46% of its debt matures after 2034. As for Energy Transfer Partners, 32% of its debt matures after 2034. Clearly Enterprise is the best of the lot in this regard, but Kinder Morgan is no slouch. Especially when you consider that other MLPs, like Buckeye Partners, for example, have 87% of their debt maturing in the next 20 years.

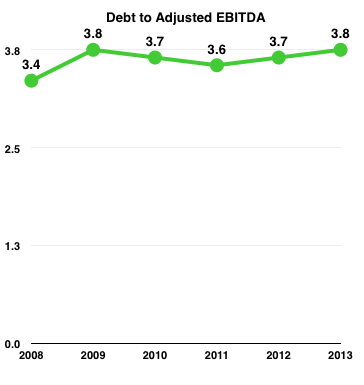

3. Debt-to-adjusted EBITDA

Now that we've got a better handle on what Kinder Morgan's debt looks like, we've come to the obvious question: Is KMP generating enough cash to pay it? For that we consider the debt-to-adjusted EBITDA ratio.

Source: Company presentation. 2013's figure is a Kinder Morgan estimate.

You can see that Kinder Morgan's estimate for 2013 is 3.8 times debt to EBITDA. That's a solid ratio for an MLP, and in fact Enterprise Products Partners sports the exact same number, while Energy Transfer Partners comes in higher, at 4.2 times.

This metric is simple, but important. Not only does it indicate a partnership's ability to pay its debts, but credit agencies rely on it when they issue ratings. Standard & Poor's, for example, does not take kindly to ratios higher than 4.0 to 4.5 times debt-to-adjusted EBITDA for investment-grade master limited partnerships. Credit ratings tie directly to the interest rates on a partnership's debt, increasing the importance of a healthy ratio.

Bottom line

Examining the 10-year debt outlook, debt maturities, and debt-to-adjusted EBITDA ratio for a master limited partnership, shows you how important a good debt story is to its future success. Too much debt can ruin a credit rating if your MLP isn't generating enough cash, making capital more expensive and hurting competitiveness down the road. Successful investing in this space is all about finding an MLP that strikes the right balance between issuing enough debt to spur growth, and developing projects that will generate enough cash to pay it off.

Aside from debt, yield is another common MLP trend. Here are 9 other high yielders