Remember when Citigroup (C 1.82%) was a "dividend stock?" Those were the good old days.

Citigroup has watched its stock price jump more than 30% so far in 2013, and its earnings per share have risen by 73% this year compared to where they were in 2012. Still, it has maintained its measly $0.01 per-quarter dividend -- however, in 2014, that may change to the delight of shareholders.

Income-hungry investors certainly wouldn't be wise to consider an investment in Citigroup, as it has one of the lowest dividend yields in the industry, and it pales in comparison to some of its better-known peers:

|

Dividend Yield | |

|---|---|

|

Wells Fargo (WFC 0.84%) |

2.7% |

|

JPMorgan Chase (JPM 0.91%) |

2.7% |

|

US Bancorp (USB 0.36%) |

2.4% |

|

Bank of America (BAC 1.15%) |

0.3% |

|

Citigroup |

0.1% |

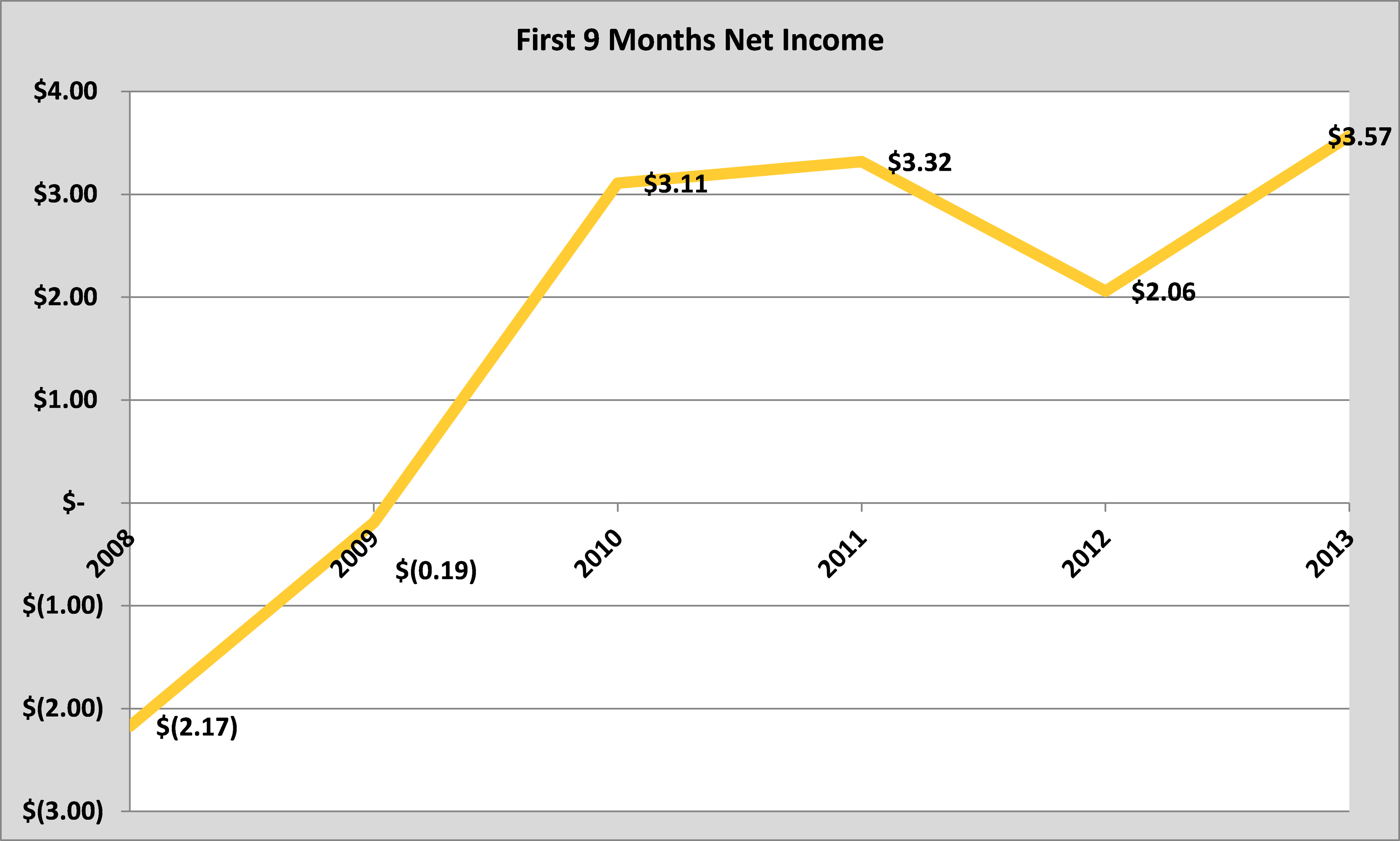

But after a rough 2012, Citigroup has seemingly begun to turn the corner and, through the first nine months of 2013, it has watched its net income rise well above where it was last year at this time, and well above the losses that were seen in 2008 and 2009:

Source: Company Investor Relations

Yet, despite this growth in its earnings per share, Citi hasn't adjusted its dividend above the $0.01 per quarter that it began paying out almost two-and-a-half years ago in May of 2011, following its stock split. Consider that in the 10 quarters since then, it has reported a total of more than $8.62 in earnings per share, but only paid out $0.10 in dividends.

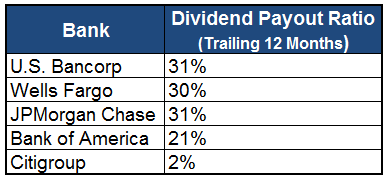

As a result, Citigroup has one of the lowest dividend payout ratios (the money it distributes back to shareholders in the form of dividends) in the industry, as shown in the chart below:

Source: YCharts

As you can see, it isn't as though Citigroup's low dividend yield is the result of its earnings power, but, instead, its seeming reluctance to give that money back to shareholders.

It is vitally important to note here that, as a part of the Federal Reserve's Comprehensive Capital Analysis and Review (CCAR), all banks in turn have to have their dividend and share buybacks approved by the Fed. The Federal Reserve notes it will only approve these for "institutions whose capital plans it approves and who demonstrate sufficient financial strength even after making the planned capital distributions to continue operating as financial intermediaries under stressful economic and financial conditions."

In fact, when asked about Citigroup's dividend on the most recent earnings call, CEO Mike Corbat noted that the company has a preference for buying back more shares than paying a dividend, so long as it's trading below book value, which is the case today as Citigroup's price-to-tangible book value stands at 0.97.

However, Corbat also added somewhat cryptically when talking about the trade-off between buybacks and dividends; "[b]ut at that point, we also understand that we, to some degree, need to be mindful and, over time, continue to address the dividend issue. So we'll look at those trade-offs as we approach."

Although the company is slowly executing on a $1.2 billion stock repurchase plan announced in April of this year, it isn't unreasonable to think that it may still consider upping its repurchase amount in 2014. However, because the stock is incredibly close to trading exactly at its price-to-tangible book value, and it will likely eclipse that barrier in 2014, it also isn't unreasonable to think that Citigroup will move away from share repurchases and request to up its dividend in 2014.