A recent Barron's article, which predicted that the price of oil will fall to $75 per barrel during the next few years, has caused a stir among oil investors.

The author believes that with U.S. domestic oil production surging and global oil consumption stagnating, supply of oil is going to rise faster than demand, putting downward pressure on prices.

Barron's has a valid argument. Unconventional oil discoveries have unlocked 30 years of extra supply during the past five years, and the prospect of peak oil now seems like a distant memory. Still, as the world continues to grow, over the long term more and more oil will be required, so there are two sides to this argument.

Nevertheless, it would be helpful to know how much the oil industry's major players, such as ExxonMobil (XOM 0.04%), Chevron (CVX 0.32%), and ConocoPhillips (COP 1.84%), will suffer if the price of oil falls to this worst-case scenario figure.

Easy to figure out

To help investors, most oil and gas companies include an estimate within their outlook forecasts of how sensitive their earnings are to changes in the price of oil and gas. For example, Exxon's management has previously stated that a $1 change in the price of Brent oil, the global benchmark, would result in the company taking a $350 million charge to upstream earnings. So, if the price of Brent fell from $100 per barrel to $75, Exxon would take an $8.75 billion annual charge to upstream earnings. Exxon reported upstream earnings after tax of $27 billion for full-year 2013.

Overall then, if Barron's $75 oil prediction comes true, ExxonMobil could see a 32% slump in upstream earnings, or a 22% decline in overall operating income.

Meanwhile, according to ConocoPhillips' August 2013 shareholder presentation, the company's management believes that a $1 change in the price of oil would see the company's annual net income take a hit of between $75 million to $85 million in the case of Brent, and $30 million to $40 million in the case of WTI.

Conoco reported a net income of $9.1 billion for full-year 2013, so a $25 fall in the price of oil, once again using the $100 per barrel average, would cost the company between $1.9 billion and $2.1 billion, or approximately 20% of net income. It would appear that ConocoPhillips is in a better position than ExxonMobil to ride out the lower oil price.

Still, Chevron would appear to be in the best position when it comes to falling oil prices as the company is one of the lowest-cost, highest-profit producers operating within the U.S.

Lower cost, better positioned

The U.S. is an essential growth market for Chevron, and the company has numerous projects coming on stream within the region through to the end of the decade. In particular, some of Chevron's biggest projects in the U.S. include the Jack/St Malo, Big Foot, Tubular Bells, Mad Dog II, and Stampede deepwater oilfields in the Gulf of Mexico.

Additionally, Chevron has 10 large projects commencing construction/production, and a further 13 smaller projects also under consideration, all within North America through to the end of 2020. Luckily, with all these projects coming on stream during the next few years, Chevron is well placed to profit, as the company is one of the cheapest upstream producers within North America. What's more, Chevron's low-cost operations mean that the company will be in a great place to ride out falling oil prices.

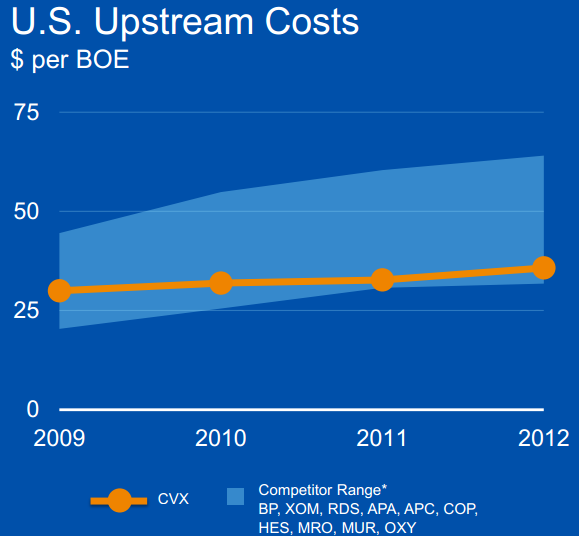

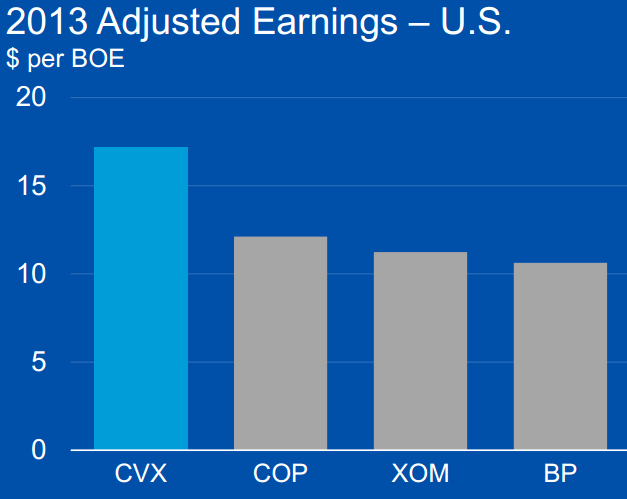

Indeed, for 2013, Chevron reported the higher adjusted earnings per barrel of oil out of any of its peers, as seen in the chart below, and the company also reported costs per barrel of oil extracted at the lower end of the range for the region, also shown below.

Source: Chevron investor presentation

These figures are encouraging, as they imply that, if the price of oil were to fall to Barron's predicted $75 per barrel, then Chevron would continue to report higher margins than its peers. It could be said that, with such wide margins, Chevron is well placed for $75 oil.

Foolish summary

All in all, $75 oil would be painful for Chevron, ExxonMobil, and ConocoPhillips, but it would not be disastrous. It's likely that all three companies will see a near 20% reduction in upstream earnings if oil were to fall to $75. In the U.S., however, Chevron is well placed to ride out weak oil prices as the company has some of the lowest lifting costs in the country.