New production technology such as fracking and horizontal drilling being used in America's shale formations has left the nation awash in cheap natural gas. With oil-based fuel such as diesel rising in price, the prospect of running America's trucking fleet on cheap, clean, and domestic fuel (with all the positive geo-political implications that come with energy independence) seems tantalizing. Companies such as Clean Energy Fuels (CLNE +6.82%) and Westport Innovations (WPRT +0.50%) offer investors a chance to get in on the ground floor of a market whose potential seems staggering. Consider these facts:

- America's class eight (33,000 lbs+) fleet is 3.2 million strong and 200,000 trucks/year are replaced.

- The average 18 wheeler gets 6 mpg and drives 45,000 miles (100,000 for long-haul trucks), consuming 7,500-16,700 gallons of fuel.

- The average price of diesel is $3.95/gallon, natural gas sells for $2.30/DGE (diesel gallon equivalent). This represents a potential $12,400-$27,600/truck in annual fuel savings.

The case for natural gas as a replacement fuel for the trucking fleet is obvious and the specific growth catalysts are strong. However, the obstacles against them continue to grow.

The case for Clean Energy

Including buses, airports, garbage trucks, and heavy duty trucking, the potential annual market for natural gas as a transport fuel is 30.5 billion DGE. Clean Energy Fuels is working hard to build out natural gas fueling infrastructure:

- over 400 fueling stations nationwide.

- 120+ highway stations to service long-haul trucking

- 26,000+ vehicles fueled daily

In addition, the company is strengthening relationships with key partners such as Waste Management, Republic Services, Flying J, Westport Innovations, and GE. It also recently announced major contract agreements with metro-transit authorities in Las Vegas, LA, and Dallas to supply a total of 42 million DGE to 2,850 natural gas-powered buses.

The case for Westport Innovations

With just over one million class 8 trucks expected to be delivered from 2013 to 2017, the potential for sales is enormous if the adoption rate can grow from its current 0.8%. Westport bulls are hoping that class 8 adoption will follow the garbage truck trend (adoption up from 3% in 2008 to 60% in 2013.)

It has joint ventures with truck engine giant Cummins, Ford, Volvo, as well as the Chinese company Weichai. In addition, the company just announced an agreement with Tata Motors (the largest car maker in India) to launch a new natural gas engine in several vehicles.

The potential market for Westport's engines includes not only truck engines but also locomotives, ships, mining machinery, and oil rigs -- pretty much anything that runs on diesel, Westport can replace with a natural gas burning engine. This creates immense optionality for the company, assuming that management can execute on its growth strategy.

Obstacles to growth

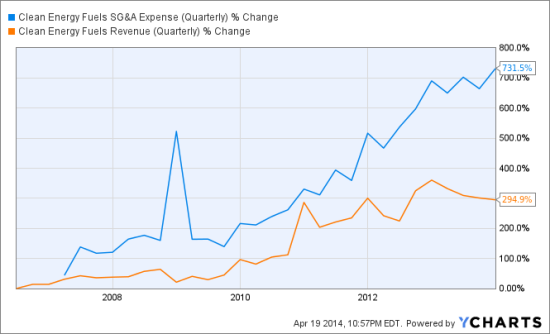

Clean Energy Fuels is facing the troubling trend of general administrative expenses as a percentage of revenues climbing over the last six years (to 45% of adjusted revenue).

Source: YCharts

With competition from giants such as Shell (which is also building a natural gas fueling infrastructure) the company's accelerating cash burn rate means the company will run out of money midway through 2016. That's just in time for $145 million in debt to come due.

Meanwhile, Westport (which was targeting 3%-5% class 8 market share in 2014) just warned that sales of its Cummins-Westport 12 liter is likely to be 40% lower than previously expected. This poor guidance doesn't bode well for the company achieving its truck market penetration goal.

Though the potential market for Westport and Clean Energy Fuels is vast, the reality is that adoption of natural gas trucking is simply not taking off despite the recent record low cost of natural gas. With the EIA predicting natural gas prices to be in a long-term upswing (due in part to upcoming LNG exports), there is little reason to believe that the conversion of the nation's trucking fleet will accelerate in the face of mounting fuel costs.

Both companies are likely to grow, but Clean Energy Fuels' mounting losses in the face of slowing revenue growth (adjusted for now expired federal tax credits 2013 revenue shrank by 8%) and upcoming debt repayments foretell ominous prospects for share price appreciation. Westport's situation is better, with the potential to be EBITDA-breakeven in 2015. However, as the struggles of both companies show, the hyper-optimistic growth case for these companies has proven false.

Bottom line

When it comes to Clean Energy Fuels and Westport Innovations, both might survive and prosper. However, investors must ask themselves if the decreased capital gains potential is sufficient to compensate for the risks mentioned above. With energy investment alternatives such as Schlumberger (37% discount to historical PE), Kinder Morgan Energy Partners (7.2% yield + 6% distribution growth), and Seadrill (safe 12% yield and a P/E of 6), investors can likely make market-crushing total returns over the long-run (while generating serious income).

Investors should ask themselves if Clean Energy Fuels or Westport Innovations can generate returns superior to these alternatives. If so, then I would advise any position be small. These investments should be only part of a well diversified speculative portfolio (which itself should be no more than 10%-20% of one's total equity holdings).