Detroit's largest solid waste services provider Waste Management (WM -0.47%) gloats about the fact that its dividend yield is in the top 10% of the S&P 500. True the company has been a good dividend payer, and has kept investors happy with regular increases. But in an industry where revenue prospects are at best modest amid weak waste volume growth and competitive pricing environment, can Waste Management protect its dividend? Already last year its dividend payout ratio went through the roof as the company took a hit on profits due to heavy impairment charges. How safe are Waste Management's future dividends?

Source: Waste Management.

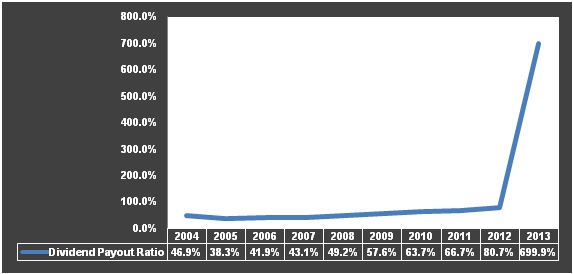

Dividend payout ratio

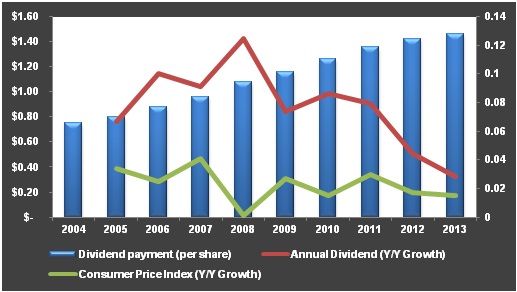

The company's board of directors has approved a 2.7% increase in quarterly dividend to $0.375 per share, which works out to an annual dividend of $1.50 per share. The company's dividend yield is 3.3%, higher than the industry average of 2.4%. With this increase, management has doubled its dividend rate compared with what it paid 10 years ago. During this period Waste Management made sure to keep dividend growth above inflation rate, to make investors see growth in real terms. The chart below shows the company's dividend increase vis-à-vis the U.S.'s annual inflation growth rate.

Data source: Morning Star and U.S. Consumer Price Index. Chart made by author.

Waste Management's dividend payout ratio has also increased over time. Generally, investors are happy with a high payout ratio, but in 2013 there was an abnormal increase as the company took a one-time impairment charge of $1 billion on writing down goodwill in its electricity business as well as some landfills, waste-to-energy facilities, and investments in waste diversion technology companies.

However, management does not expect such charges to recur in 2014, and expects earnings to be in the range of $2.30-$2.35 per share, compared with $0.21 per share in 2013. This puts 2014 dividend payout ratio in the comfortable range of 64%-65%. According to Marc Lichtenfeld, author of a best seller "Get Rich With Dividends: A Proven System for Earning Double-Digit Returns", any ratio that equals to or is lower than 75% could be considered safe.

Data source: Morning Star. Chart made by author.

Free cash flow

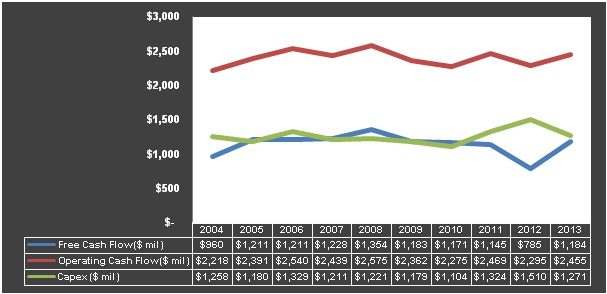

Waste Management generates free cash flow quite consistently, which supports its dividend payments. Free cash flow has remained above $1 billion in eight out of the last 10 years. This comes from steady operating cash flows which reflect the company's continued focus on improving yield (revenue impact from pricing actions), reducing costs, effective working capital management, and disciplined capital expenditures. Waste Management has been able to restrict its annual capital spending within $1.5 billion in the last 10 years, except 2012.

To continue to keep a tight rein on capital expenditures, management has taken various initiatives. There are monthly reviews of capex requests, part of executive incentives are tied to free cash flow improvements, and there's focus on improving the internal rate of return for each line of business. Waste Management wants to keep its capital expenditures between $1.2 billion and $1.3 billion in 2014. It's increased its guidance for free cash flows generation and expects it to be in the range of $1.4 billion-$1.5 billion, up from $1.3 billion that it expected prior to the first-quarter results.

Data source: Morning Star. Chart made by author.

Growth prospects

Growing revenue is a big challenge for Waste Management as waste volumes are seeing stunted growth in the U.S. post the 2009 recession. It saw an 11.9% revenue decline in 2009. Though it picked some momentum in 2010-2011 and revenue grew at around 6%-7%, the growth has come down to about 2% since 2012.

In the first quarter, Waste Management saw a modest 1.8% revenue growth, which came solely from the 2.6% increase in average yield as volumes were down 1.8%. Core pricing was up 4.2% during the quarter as the company realized better prices in most lines of businesses. Given that the first quarter is seasonally weak, volumes could improve in the upcoming quarters and management expects prices to stick. For the full year the company estimates 2% positive impact on revenue from yield and 1% negative impact from volumes.

Despite weak revenue growth, Waste Management did a good job with earnings in the first quarter. Earnings per share grew 22.5% to $0.49 per share. The company is focusing on contracts with good yield, technological improvements, and aggressive costs cutting. This should support earnings growth over the coming quarters.

From a more long-term perspective, Waste Management is aiming to boost its presence in developing countries. It already has a significant stake in a waste management company in China -- the country with the planet's largest population from which it expects the next wave of growth. By 2020, it expects to handle more than 20 million tons of waste, 67% higher than the 12 million tons of waste processed in 2012. This could help sustain the company's earnings momentum in future.

Foolish takeaway

Waste Management has diligently maintained its track record of growing dividends, keeping up investor confidence. The company's free cash flow continues to remains strong to help support the trend. It's also taking concrete steps to maintain sound growth in profitability, despite soft industry conditions. With secured dividends, Waste Management's looks attractive for value investors.