Today I would like to try to illustrate the difference between picking a good company and picking a good stock. I recently wrote about how I have a short position in Amazon.com (AMZN -1.09%), and then went on to express my belief that Amazon has a bright future. No, I'm not off my meds. I just get this recurrent feeling of deja vu when I look at Amazon, and I'll try to explain the reason for this sensation in the corniest way I can come up with.

Once upon a time

A long time ago in an enchanted world referred to as the 1990's, little boys and girls had no Internet. Then, thanks to the tireless work of Al Gore (among others), this lost world began to slowly get connected computer by computer, and the worldwide web was born. Stock traders recognized the unprecedented economic opportunity that the Internet would create and began buying up shares of any "Dot Com" that moved.

Many of these companies, such as Pets.com and TheGlobe.com, were not profitable and never would be profitable. However, there were many companies with excellent business models that actually were very well-positioned to capitalize on the long-term Internet boom. Today I'm going to talk about one of these companies, and I'm going to call her "Goldilocks."

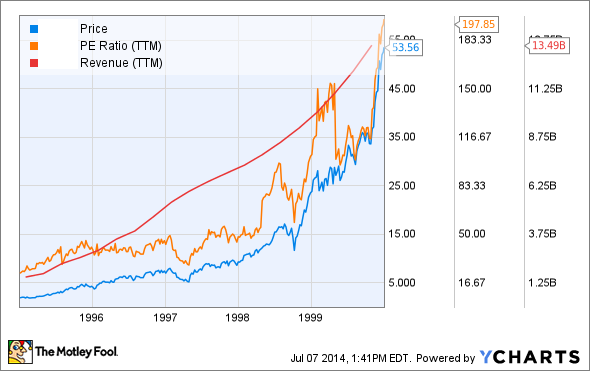

In the 1990′s, Goldilocks manufactured computer networking equipment, and her products were in high demand. Investors piled into Goldilocks' stock because they could see that her products would play an integral part in the expansion of Internet connectivity that started in the 90′s and would last indefinitely. To investors, Goldilocks looked like one of those rare companies an investor could buy and hold until retirement and never have to worry about. Let's take a look at some of Goldilocks' numbers at the time.

A quick glance at Goldilocks' share price and revenue from 1995-2000 paints a beautiful picture. With annual revenue that exceeded $13 billion by the dawn of the new millennium, this company was far from a mom-and-pop operation. And yet, the future remained so bright that many of Goldilocks' shareholders thought that its revenue would continue to grow rapidly for decades to come. It seemed clear that the Internet was the future, and Goldilocks' products would remain in high demand indefinitely.

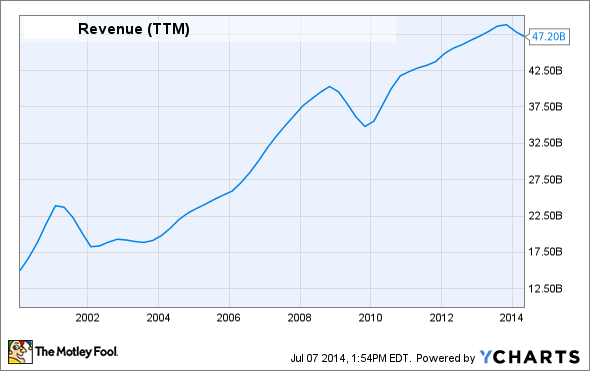

The good news for Goldilocks' shareholders is that they were right about the future of the business. Here's a chart of Goldilocks' revenue from January 2000 to date.

Revenue has more than quadrupled to over $47 billion, with no sign of a slowdown anytime soon. That porridge tastes just right. Clearly the company has continued to perform exceptionally well over the last 13-plus years. But if you joined the other shareholders in ignoring that orange line on the first chart, you might be surprised to see what Goldilocks' stock has done since 2000.

No, that graph is not upside down. That porridge is cold. Let me summarize: for the past 13 years, Goldilocks' revenue is up about 250%. For that same period, the S&P 500 is up 34.5% as a whole. And finally, Goldilocks' share price is down well over 50% for that 13-year period.

A nearly limitless number of metrics are available for stock analysis, but I'm a big fan of keeping things simple. At the end of the day, the only two things that matter about a stock are the performance of the company and the price of the stock. If a company does not perform, it's typically only a matter of time before its stock price reacts poorly. And if a stock gets too expensive relative to the earnings that the company is generating, it's typically only a matter of time before the stock price reacts poorly.

And now for the big reveal...

For "Goldilocks," which readers might have recognized as Cisco Systems (CSCO +0.15%), the performance of the company was not to blame for the collapse in share price. The Dot-Com Bubble euphoria that drove Cisco's P/E ratio to 200 was to blame. That large of a multiple for that large of a company has repeatedly proven to be unsustainable over the long term, and Cisco was no exception.

And that brings us to Amazon. Let's first look at a chart of some numbers on Amazon.

Amazon is the standard-bearer for worldwide Internet retail, and I would be foolish to argue that Amazon will not continue to dominate the online marketplace for decades. However, it seems equally as foolish to me that investors are currently paying well over 500 times earnings for shares of Amazon stock.

Will Amazon follow in Cisco's footsteps?

History has shown with Cisco and countless other examples that large-cap stocks cannot maintain such high P/E ratios for extended periods of time, regardless of how well the companies perform. Maybe Amazon will prove to be the exception to the rule, but I'm certainly not betting on it.