Wall Street is really warming up to Netflix's (NFLX 0.20%) business model. Just three months ago, the analysts covering the stock guessed it would earn $1 in second-quarter profit, or double last year's haul. Today that average estimate is $1.15 a share, which is above the company's own guidance and would represent a 135% leap, year over year.

With that rising profit outlook a big driver behind the stock's 40% rise since April, how can investors be so confident that Netflix will deliver when it posts earnings results on Monday, July 21?

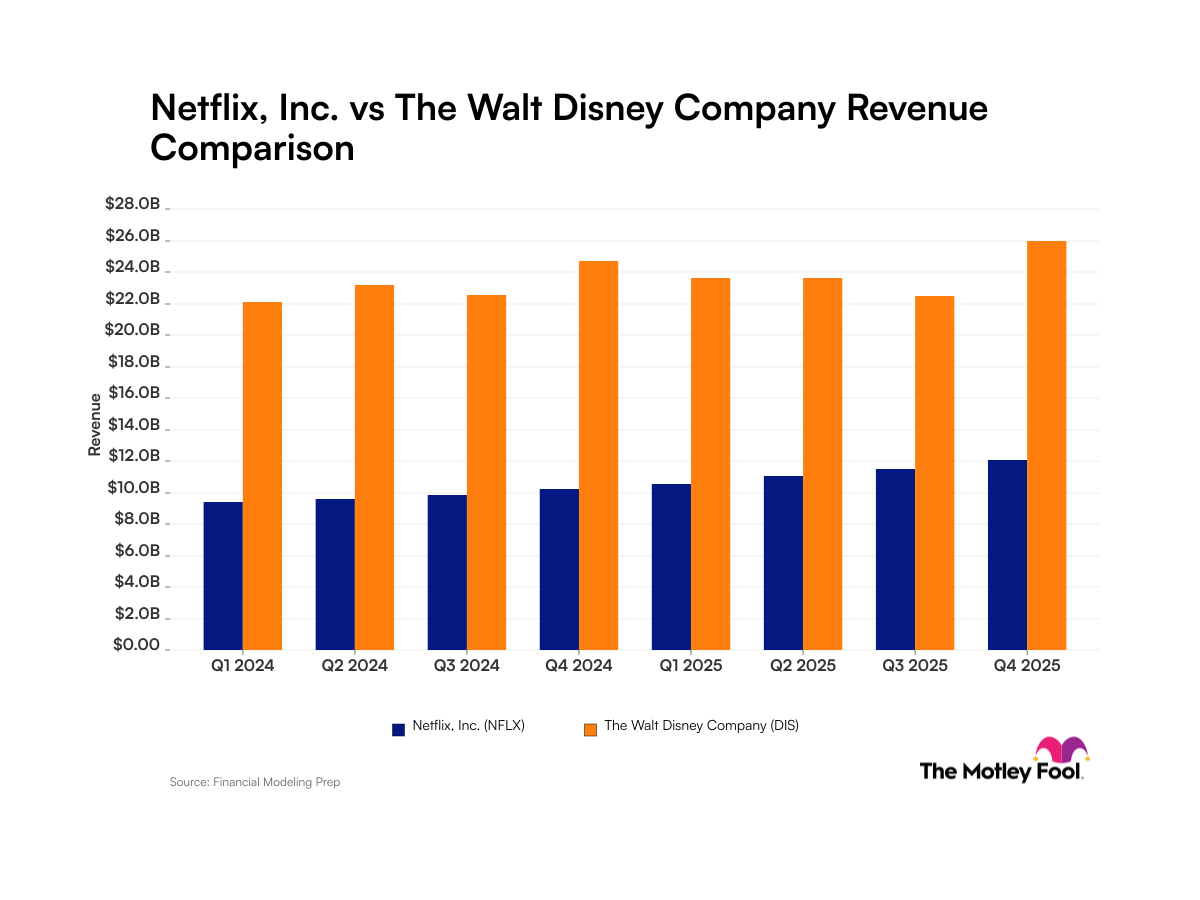

Overseas turning point

An improving international business is one big reason for that confidence. The expansion into markets like Latin America and the U.K. has been expensive for Netflix. A year ago the overseas business cleaved $70 million out of operating profit, for a depressing negative 40% contribution margin overall. Netflix's domestic streaming, by contrast, generated a 22% contribution margin as membership revenue in the U.S. came in far above content spending.

However, the international business has been improving all year. Last quarter Netflix lost just $35 million outside the U.S., for a negative 13% margin. In fact, the second quarter will likely mark a key turning point where international losses finally stop siphoning profits from the domestic business.

Source: Company financial filings. Q2 is Neftlix's forecast.

Investors can't expect that happy trend to continue for long, though. Netflix plans to launch a new expansion into Germany, Austria, Switzerland, France, Belgium, and Luxembourg beginning later this year. That move will drag profits down again, but Netflix's experience suggests that those new markets will reach breakeven quickly, in as little as two years.

The value of a dollar

Meanwhile, Netflix's U.S. business is becoming a profit machine. Contribution margin hit 25% last quarter and, if you believe management's forecast, should reach 27% in the second quarter. CEO Reed Hastings' team has been careful to manage the growth in content spending so that it has consistently trailed revenue growth over the past 10 quarters.

Source: Company financial filings.

Profitability could improve even faster in the second quarter, though, thanks to help from Netflix's first price hike in years. Sure, the boost from that $1 monthly fee increase will be tiny, as it only impacts 500,000 (or so) new members out of a subscriber base of 35 million. Still, the profit benefit will increase over time, and Netflix has plenty of other opportunities to raise its average revenue per user, including tiered streaming plans.

An earnings beat?

Given the positive trends in the U.S. and overseas businesses, Netflix is sure to post a big profit gain next week. But could earnings actually beat Wall Street's lofty expectations?

An upside surprise would likely come from higher-than-expected subscriber growth in the U.S., which is admittedly doubtful. After all, management has a strong track record when it comes to forecasting membership gains: It hit last quarter's 2.25 million additions right on the nose. And Netflix said in April that this quarter should be the weakest of the year, with only 500,000 new domestic signups.

Still, the company is in uncharted waters with its exclusive series like House of Cards and Lilyhammer entering second and third seasons. Its marketing plan in the second quarter leaned heavily on the popularity of season two of Orange Is the New Black, which launched in June. If that show worked surprisingly well as a membership draw, then Netflix has a good shot at beating earnings estimates for the fifth quarter in a row, despite those high expectations.