Just last year enthusiasm was ballooning for aviation manufacturer Boeing (BA -3.33%) which sent its share price soaring 80% higher, even becoming the best performing Dow component during 2013. Boeing's share price continued to soar despite many headlines highlighting the problems caused by Boeing's 787 Dreamliner -- whether it was traveling folks dealing with grounded airplanes or the investing community dealing with production delays and budget overruns.

After an incredible run in 2013, though, Boeing's share price has been reluctant to move higher this year. Will the company's second quarter earnings, due out on Wednesday, be enough to revive Boeing in 2014?

What are the expectations

Let's get the dreary Wall Street estimates out of the way, before taking a look at some key factors for Boeing's second quarter.

According to Yahoo Finance, the average analyst estimate for Boeing's Q2 earnings-per-share is $2.01, which is a 20% hike compared to last year's second quarter. Revenue is expected to reach $22.36 billion, which would be a meager 2.5% gain, compared to last year's second quarter.

Beyond these short-term figures, there are more valuable factors for investors that are interested in Boeing's long-term investing thesis.

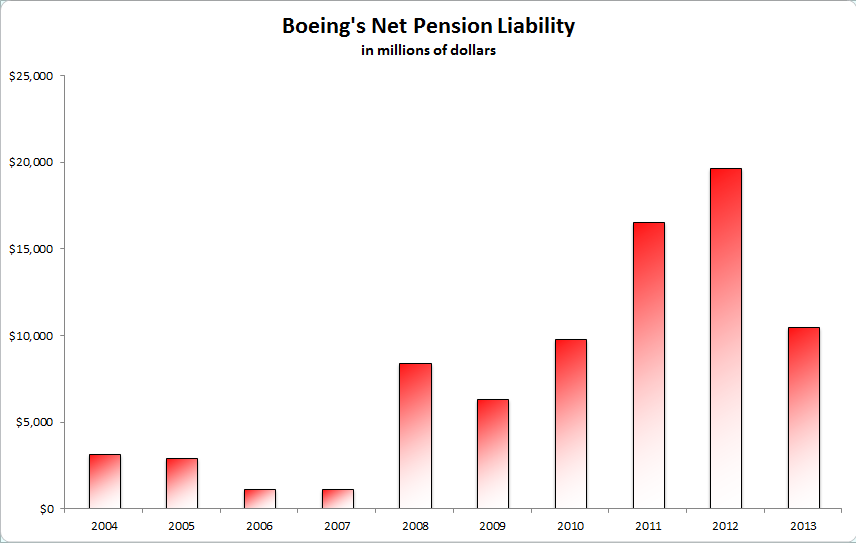

Pension liability

One of the biggest concerns with Boeing is its large pension liability, something many large industrial companies are battling.

Chart by author. Information Source: Boeing's SEC filings.

Boeing was able to knock its pension liability down significantly last year, however, it's still a huge and very costly obligation. Consider that in the most recent quarter Boeing's pension expense was slightly more than $1 billion. To help put that in context, that $1 billion pension expense is roughly twice the amount that Boeing's dividend cost in the same quarter.

For the full year 2014, Boeing is projecting that its pension expense will check in around $3.2 billion. Put another way, that's the same amount that management plans to spend on research & development this year, and just slightly more than its capital expenditures which are expected to be roughly $2.5 billion.

Investors will cheer the day that Boeing's pension fund is fully funded, or fully de-risked, so that its cash flow can be used for shareholder friendly events, such as a larger dividend or share repurchase program. Until that happens, investors would be wise to keep an eye on Boeing's quarterly pension contributions and expenses.

One other factor investors should be paying close attention to will be additional insight to Boeing's accelerated production.

787 Dreamliner in final assembly. Source: Boeing

Production hiccups?

Boeing delivered 161 commercial aircraft in the first quarter, and according to the company's website it has delivered 181 in the second quarter for a total of 342 commercial aircraft. Despite the increase, from the first quarter, rumors have spread that Boeing has had trouble keeping its 787 Dreamliner production pace at 10 aircraft per month which could hinder the company's ability to reach its guidance of 715-725 commercial aircraft deliveries this year.

Boeing's focus to accelerate production across its commercial aircraft lineup is critical if the company is to convert its massive backlog of commercial orders, valued at $374 billion at list prices, into additional revenue, cash flow, and profits.

"They need to continue to crank 787s out and get cash flow on them," said Jim Reed, co-manager of the Global Equity Fund at Scout Investments, according to Reuters. "And they need to move from producing 10 787s a month to 12 a month, like they say they're going to do" by mid-2016."

Boeing's operating margin on its commercial aircraft hit 11.8% in the most recent quarter, 40 basis points higher than last year's first quarter and the highest mark in a year. Investors would cheer an increased figure in the second quarter and it would reassure investors that rumors about multiple production hiccups were overblown.

Bottom line

Ultimately, Boeing is very well positioned for long-term investors and very few companies can offer the impressive backlog of orders, for revenue transparency, that Boeing does. Furthermore, management projects global demand for commercial aircraft over the next two decades to reach 36,770 new airplanes. That would be a staggering value of roughly $5.2 trillion, of which Boeing would be well positioned to earn more than its fair share.

However, there are no short-cuts for Boeing and its investors; the company must iron out production kinks this year and continue piling cash into its pension fund before its share price moves higher.