Later this week Visa (V +0.58%) will announce its earnings from the last three months, and there are three things investors need to keep an eye on.

What does it think of its own stock?

As previously noted, both Visa and MasterCard have been aggressively repurchasing stock over the last few years.

And through the first six months of its 2014 fiscal year -- the year concludes for Visa on September 30 -- Visa repurchased $2.2 billion worth of its common stock at an average price of $208 per share. And during the first three months of the year its $1.1 billion in repurchases cost the company $217 a share.

With that in mind, the second three months of 2014 were tough from a stock standpoint for Visa. As shown below, Visa traded below what it paid for its stock every day during the first three months of the year:

As a matter of fact, half of those days witnessed the stock being traded for less than $208 per share.

So having said all that, it will be interesting to see exactly what Visa thought of its own shares. Did it boost its repurchases as its stock fell? Or did it lower its own valuation?

There is the possibility it simply executed the same amount regardless of the price, but it will be worthwhile to take note of what it thinks of its own stock.

What exactly is it investing in?

When discussing the first three months of the year, one of the most interesting remarks from the CEO of Visa, Charlie Scharf, came when he said Visa continues "to make substantial investments in products and services that will drive our future growth."

And just last week there was the announcement of Visa Checkout, what it describes as "a quick and easy payment service that enables consumers throughout the United States, Canada, and Australia to pay for goods online, on any device, in just a few clicks."

In short, it replaces V.Me by allowing individuals registering their credit or debit cards and their shipping information under a single username and password, and check out across a variety of sites.

Earlier this month I wondered exactly what Visa was doing with V.Me, and just a few days later we learned the answer.

Many have suggested the payment industry is poised for rapid change, and Visa Checkout appears to be one very good way to do this. But instead of saying the company is making "substantial investments," in these areas, it would be fascinating to know not only what it is doing, but how well these innovations are succeeding.

Can the growth continue?

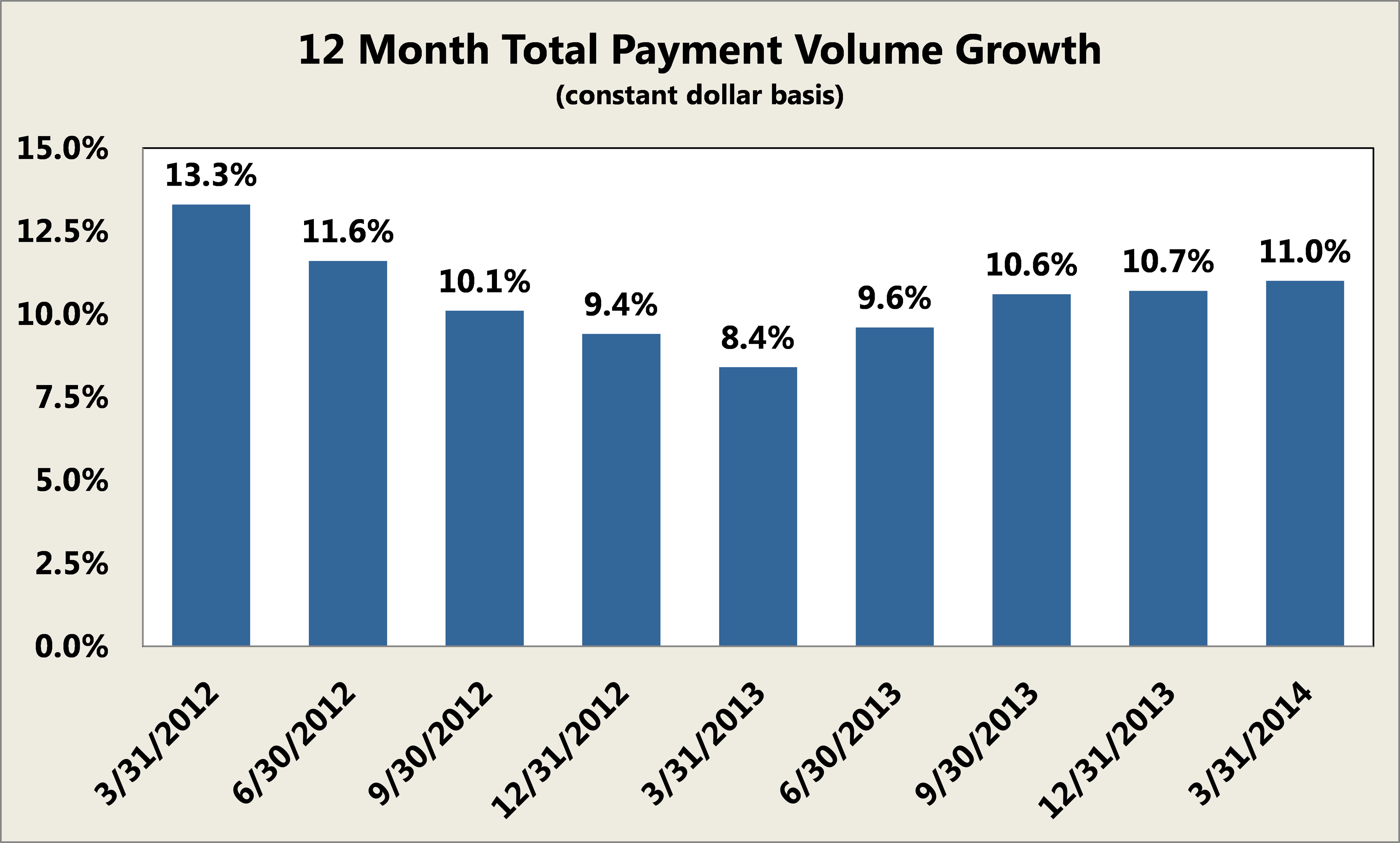

Many people assume since Visa is such a big name, its days of massive growth are behind it. Yet as shown in the chart below, the growth of its total volume of transactions on a constant dollar basis -- excluding inflation -- has only continued to rise over the last year:

Source: Company Investor Relations.

With that in mind, it will be important to see how this growth -- and the corresponding impact to its bottom line -- is progressing. Since Visa is such a common product and a household name -- not to mention it facilitated $7.1 trillion in transactions over the last 12 months -- many have thought its days of impressive growth are well behind it.

But if its volume continues to grow faster and faster on both a dollar and percentage basis, then it could mean its future growth runway is even longer than any of us imagined.

There is a lot to like about Visa and the prospect of its future if it thinks highly of its own stock, continues to innovate, and exhibits impressive growth, and these are the three things I'll be watching when it announces earnings this week.