Not all dividend stocks are created equal. Consolidated Edison (ED 0.61%) has proven year after year that it's got what it takes to keep pulling profit for your portfolio. But dividend stock investments can be dynamite or dinosaurs depending on when you buy. So is ConEd worth its weight? Here's what you need to know.

An aristocratic asset

Any corporation can dole out a dividend. Some sneaky companies will even use them as investor candy, invigorating interest at the expense of long-term value creation. But a dividend aristocrat like Consolidated Edison is about as good as it gets. ConEd earned its aristocratic status by increasing its dividend for more than 25 consecutive years -- 40, to be exact. But dividend dynamite can still be a dud if you buy at the wrong time. Let's dive deeper to see whether ConEd can keep delivering for decades to come.

Stock analysis

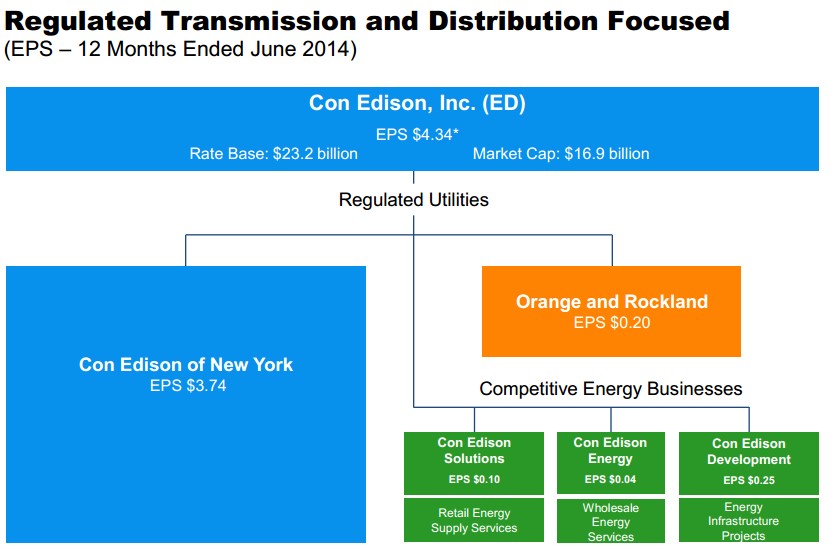

When it comes to dividend stocks, Consolidated Edison checks all the right boxes. As a utility, over 90% of its earnings come from regulated companies. With 3.3 million electricity customers and 1.1 million customers spread across New York, that's a laudable load of steady sales.

For investors, that means a government-assured return on equity for all ConEd's electricity sales. And while no one's expecting New Yorkers to boost energy consumption by 100% next year, those slow and steady earnings are exactly what income investors need for their dividend dreams to come true.

Recently, ConEd's stock growth has hit a soft spot. While it maintained much of its value through the worst of the Great Recession, prices are currently sitting at 2011 levels.

Source: YCharts

In general, dividend stocks have lulled in the past couple years. As the U.S. economy picks back up, investors have pulled slow-moving dividend stocks from their portfolios in favor of fast-moving, high-reward (but also high-risk) stocks.

For longer-term investors, this creates a unique value opportunity. With tried and true track records, dividend stocks are usually priced for perfection. But currently, Consolidated Edison is sporting some surprisingly reasonable ratios. A 13.2 P/E (price-to-earnings) ratio is one of the lowest of its sector, while its 1.3 price-to-book ratio puts ConEd on par with other utilities. That lower stock price has also pushed Consolidated Edison's current dividend yield to a fantastic 4.4%, the third-highest among all S&P 500 dividend aristocrats.

And looking ahead, its debt-to-equity ratio of nearly 1 is below average for utilities, an important consideration as the Fed flirts with raising the interest rate target -- essentially making debt more expensive to manage. Consolidated Edison isn't only good on the books. It's expanding its natural gas generation and distribution business, pouring over $1 billion into storm hardening investments over the next few years and expanding both its energy efficiency and renewable energy programs.

Time to buy Consolidated Edison?

Source: Consolidated Edison, Inc .

Fellow Fool Morgan Housel calls "time" the one remaining edge you have on Wall Street -- and that's especially true for dividend aristocrats. Thrill-seeking traders have left Consolidated Edison underappreciated and undervalued. For long-term investors, now is the perfect time to electrify your portfolio with a piece of ConEd.