United Parcel Service (UPS 0.08%) investors will have been pleased to see the stock rising after a solid set of results. I've already covered the key points on the third-quarter earnings, and then looked at the five things that management wants you to know about the company's prospects. Now it's time to look at the company purely from the perspective of an investor looking to buy the stock. In doing so, I'll outline the three reasons the stock could start to play catch-up with its rival FedEx (FDX 2.80%) and the market in 2014.

E-commerce brings challenges and opportunities

The reasons for the underperformance of UPS relative to FedEx have already been discussed in more detail. Simply put, UPS was harder hit than FedEx by the severe winter weather last year. However, one development that affects both companies is the burgeoning development of e-commerce deliveries, and in particular, from business to consumer, or B2C, channels.

According to UPS management on its recent earnings call, e-commerce deliveries now make up 45% of its business. Moreover, the indications are that growth will continue to be strong for years to come. For example, eMarketer predicts that worldwide B2C e-commerce growth will be nearly 20% in 2014, and then only drop into single-figure growth in 2018.

In a sense, it's bringing an opportunity and a challenge. It's good in the sense that revenue growth looks assured, but it's also bringing about margin pressures for two key reasons:

-

B2C deliveries tend to be lighter-weight and lower-yielding.

-

Increasing B2C demand in the holiday season tends to create higher peak demand, and UPS and FedEx have both had to increase investment in order to deal with it.

In the case of UPS, the margin pressure is showing up in its U.S. Domestic Package operations (64% of segmental income). The following chart shows how domestic package revenue growth has improved in the last two years (green line) and how operating margin has declined at the same time.

Source: UPS Presentations, author's analysis. 100 basis points = 1%

Going forward, UPS is planning two things in order to try to increase margin and take advantage of rising demand.

First, UPS followed FedEx in announcing plans to increase prices by 4.9% in North America. The new prices will go into effect on Dec. 29 for UPS and Jan. 1 for FedEx.

Second, both companies are shifting to dimensional weight pricing for all their Ground packages. In other words, all packages will now be priced on a combination of weight and size, rather than just weight. The benefits should be that retailers will be incentivized to reduce unnecessary package volumes, therefore allowing UPS and FedEx to increase yields per volume.

The good news is that both companies are making similar changes, so it's unlikely that one will run the risk of losing significant business to the other -- good news for both companies.

B2B growing in North America too

While most of investors' attention was focused on B2C deliveries in the most recent results, business-to-business, or B2B, shipments are quietly growing in line with an improving U.S. economy. CFO Kurt Kuehn said on the recent earnings call: "We were about 45% B2C in the U.S. in the third quarter. Certainly, that number is continuing to grow, although we're seeing, as we've mentioned, good strong robust growth in B2B as the industrial base of the U.S. picks up."

If the U.S. economy is really headed for an industrial renaissance, then UPS and FedEx will surely be beneficiaries. Readers might note that UPS management is going to update investors on its outlook for B2C and B2B growth in the upcoming investor conference on Nov. 13.

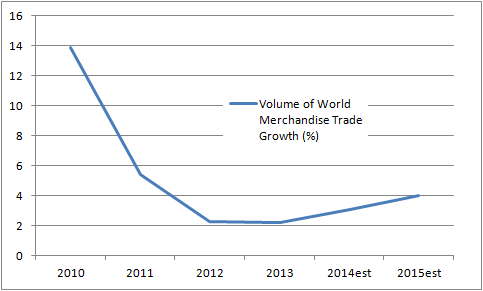

World trade growth

UPS and FedEx are both likely to see the benefit of an increase in world trade. The following chart shows projections from the World Trade Organization, or WTO, that indicate an acceleration of growth in the next two years. Don't get too excited by the high growth rates in 2010-2011; this sort of thing happens when the economy recovers from the low point of a severe recession.

Source: World Trade Organization.

The numbers indicate more growth to come, but readers should note that the WTO recently lowered the 2014 and 2015 estimates to 3.1% and 4% (shown on graph) from 4.7% and 5.3%, respectively -- somewhat of a disappointment.

The takeaway

All told, if UPS and FedEx can get the pricing initiatives to stick without affecting volume growth, then margins could improve, particularly for their B2C package deliveries. Despite some recent setbacks, the global economy is still set to increase its growth rate in 2015, and with the IMF forecasting U.S. GDP growth to strengthen to 3.1% from 2.2% in 2014, UPS could see a nice pickup in U.S. B2B deliveries too. Plenty of things to look forward to in 2015 for UPS.