BreitBurn Energy Partners (BBEP +0.00%) has been paying a monthly distribution to investors since the start of 2014. At the time, CEO Hal Washburn said the company made the change from quarterly payouts to "more efficiently return capital to investors and satisfy growing demand for investment options paying monthly distributions. We believe that being responsive to our investors is an important part of our business." Since the first monthly payout in January, the company has actually raised its distribution twice as its growth plans bear the fruit of an ever-growing income stream for its investors.

BreitBurn Energy Partners 101

Investors new to BreitBurn Energy Partners should know that it's an upstream master limited partnership, or MLP. Upstream refers to the ownership and operations of oil and gas wells, while an MLP is a tax-advantage corporate structure. The combination of the two provides the generous distributions paid by BreitBurn and its peers.

BreitBurn Energy Partners is one of the largest upstream MLPs in the sector, and it's about to get even larger via the acquisition of fellow upstream MLP QR Energy (NYSE: QRE). Once that deal closes, the combined entity will be the largest oil-weighted upstream MLP and will have a strong, geographically diverse asset base, as shown on the following map.

Source: BreitBurn Energy Partners Investor Presentation.

Drilling down into the monthly distribution

The key to BreitBurn Energy Partners' monthly distribution is its ability to generate sufficient cash to keep the income flowing. In evaluating MLPs, the key number is the distribution coverage ratio. The following chart shows that this ratio has fluctuated quite a bit at BreitBurn.

|

Distributable Cash Flow |

DCF Per Unit |

Coverage Ratio | |

|---|---|---|---|

|

2q14 |

$52,746,000.00 |

$0.43 |

0.86 |

|

1q14 |

$60,272,000.00 |

$0.50 |

1.00 |

|

4q13 |

$55,419,000.00 |

$0.46 |

0.93 |

|

3q13 |

$64,564,000.00 |

$0.64 |

1.31 |

|

2q13 |

$48,248,000.00 |

$0.48 |

1.00 |

|

1q13 |

$32,130,000.00 |

$0.32 |

0.67 |

|

4q12 |

$38,736,000.00 |

$0.45 |

0.95 |

|

3q12 |

$44,008,000.00 |

$0.53 |

1.10 |

Source: BreitBurn Energy Partners press releases.

On average, the coverage ratio over the past two years was 0.98 times, which is a little weaker than we'd like to see. An even 1 is really the minimum we want here, as it suggests the company is paying out 100% of its available cash flow. A ratio of 1.1 times or more would be ideal as it would provide a much larger margin of safety. BreitBurn Energy Partner's ratio, thus, is certainly cause for caution.

That being said, acquiring QR Energy will boost BreitBurn's distributable cash flow per unit -- so much so that the company feels comfortable enough to boost its payout by another 3.5%. Future acquisitions should further boost the company's cash flow to support maintenance and additional growth of the payout.

Finally, the company's strategy for growing its income stream to investors is not based solely on acquisitions. The company is beginning to focus on horizontal drilling in the Permian Basin and recently announced a deal to boost its acreage in the play. Drilling these high-returning wells should increase the company's cash flow and coverage ratio

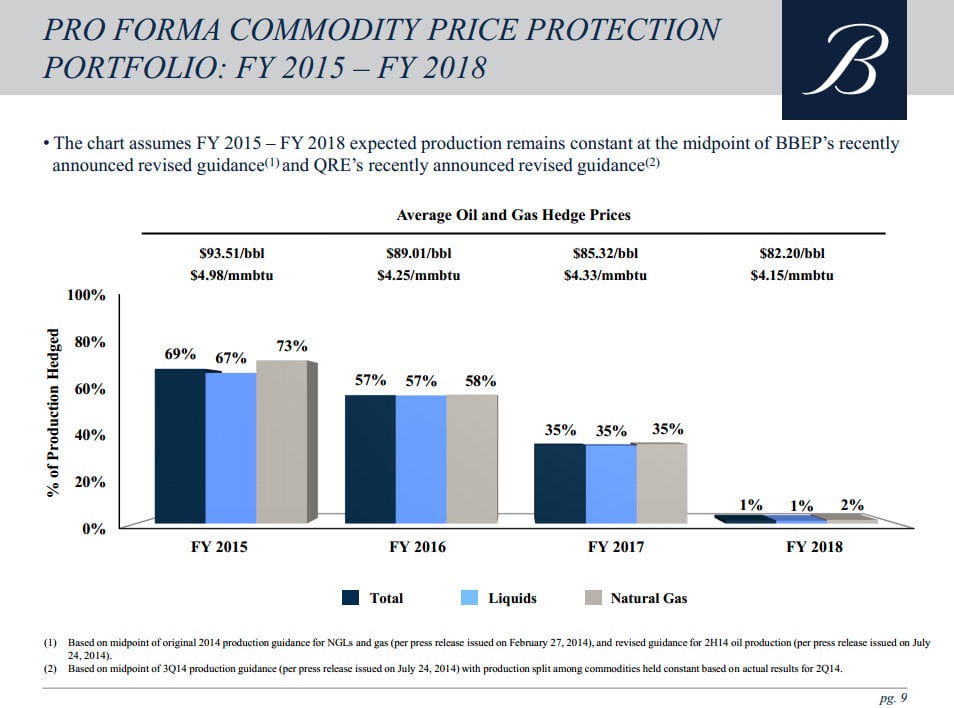

However, if there is a concern regarding the security of its cash flow, it's BreitBurn's exposure to oil and gas prices. While the company hedges a large portion of this exposure, the following chart shows that only 69% of its 2015 production is protected, and that drops to 57% for 2016.

Source: BreitBurn Energy Partners Investor Presentation.

The biggest concern here is that 33% of the company's higher-margin liquids production is at risk next year if oil prices don't bounce back. This unhedged production could impact the company's distributable cash flow, which could put its current distribution rate at risk.

BreitBurn Energy Partners offers investors a generous, oil-fueled monthly income stream. While that generosity might be a bit excessive given its exposure to oil prices, it's a risk that could pay off if oil prices return to previous highs.