At General Electric (GE +0.84%), each fiscal year seems to be marked by a single overarching theme or transition. In 2012, it was a shake-up in its energy business, when GE split this huge $50 billion segment into three different units. In 2013, it was the revival of GE Capital, which could once again transfer large amounts of cash to its parent -- and thereby to GE shareholders.

In 2014, services are the main story at GE, and the "industrial Internet" is the hero. This narrative, as I described recently, has been in the works for roughly two decades, but only recently has it taken center stage.

Through a closer look at the strategy of GE's management team and the financials, we can get a clearer sense of how the services story is unfolding in 2014.

To give to investors, or to invest?

As I mentioned before, last year marked a turning point in GE Capital's dramatic turnaround. Once GE had straightened out its formerly freewheeling banking unit, the $45 billion entity could behave like the cash cow GE hoped it would be.

GE took advantage of the influx of cash from its banking arm and redirected a healthy portion primarily to shareholders in 2013. During last year alone, more than $18 billion was returned to owners through buybacks or dividends, as shown in the chart on the left below:

Source: GE Q3 2014 Presentation, S&P Capital IQ, author's calculations. Numbers in billions.

In 2013, the redistribution of excess cash to shareholders sent the message that dividends were a top priority, and that this company recognized the crisis of confidence that resulted when it cut its dividend in 2009.

But fast-forward to 2014 -- shown on the right above -- and it's a pie chart of a slightly different coloring. GE's investing its extra cash in acquisition-related activities more so than in dividends and buybacks.

In fact, share repurchases and dividends accounted for nearly double the percentage of total capital allocation -- 67% in 2013 versus 35% in 2014 -- than they do through the third quarter just reported.

To be sure, the fourth quarter could tilt the balance slightly since management forecasts total dividends and buybacks reaching at least $11 billion for the year versus the $8.4 billion to date. But it is clear that GE CEO Jeff Immelt is pivoting toward external investment opportunities for now. Most notably, the $13.5 billion deal for France's Alstom stole the spotlight over the summer.

But here's why GE believes Alstom was the right place to put its cash at the right time.

Building a bigger base

GE invested in Alstom for a variety of different reasons -- 10, to be exact. The company outlined them in a presentation in April before the deal even entered into the negotiation stage. The rationale included everything from Alstom's engineering talent to its geographic footprint to its complementary power products like steam turbines.

But the real reasons GE wanted to get a grip on Alstom were its backlog, installed base, and the lucrative services contracts that often accompany those prime assets.

At the time, Alstom had an installed base -- which means products being actively used by customers in the field -- of 350 gigawatts worldwide (turbine supply orders are typically measured in terms of the gigawatts of energy they produce). For GE's power and water division, this would provide a boost of 35% relative to the current installed base of 1,000 gigawatts.

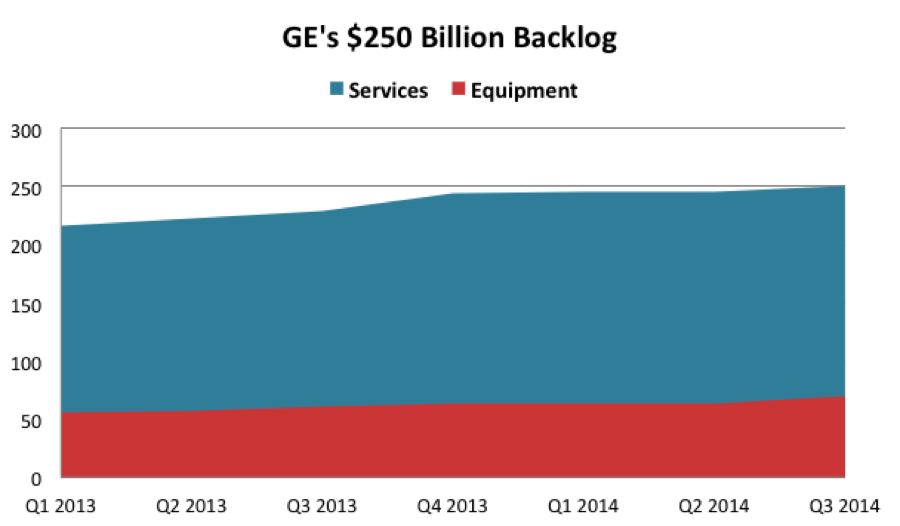

What's more, Alstom's backlog of roughly $38 billion could provide a much-needed catalyst for GE's business in the years ahead. To clarify, that's $38 billion worth of sophisticated products expected to be delivered to customers in the near future, which can be layered on top of GE's steadily growing $250 billion backlog as it stands today:

Source: GE Q3 2014 Presentation. Numbers in billions.

So, GE recognized the tantalizing opportunity presented by both Alstom's current installed base and the backlog, and it found a way to wrestle the deal out from under its competitor Siemens and woo the French bureaucrats at the same time.

Despite the price tag and the watered-down nature of the final agreement, GE probably managed to come out on top for one key reason: Highly profitable services contracts are the key to GE's future profits, but they can only be sold in conjunction with equipment.

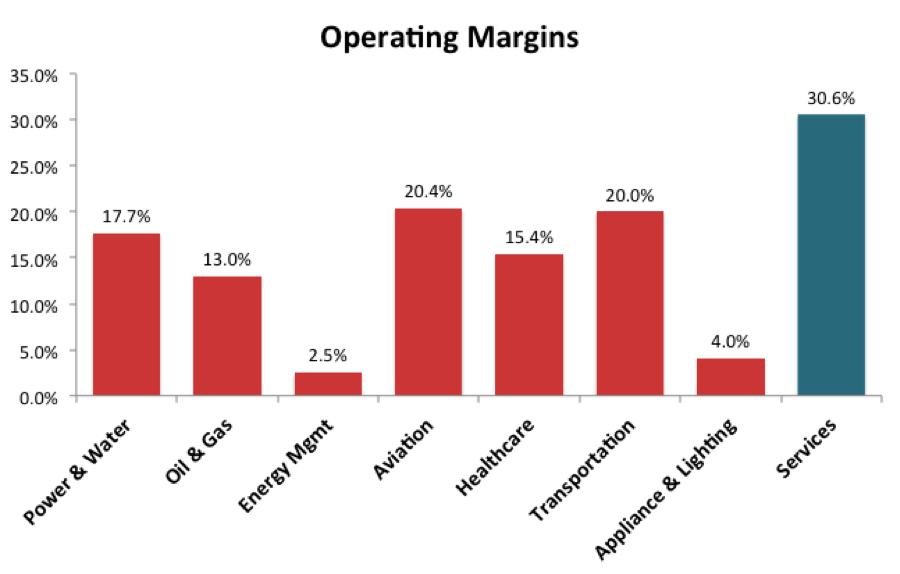

For GE, services are the "blade" in the "razor-and-blade" business model. They're much more profitable than GE's physical products, and they can be sold as an accompaniment in nearly every segment of the business.

The chart below shows how the operating margins from services -- which is not a stand-alone segment but is shown separately for comparison -- tower over the operating margins generated by GE's industrial businesses:

Year to date. Source: GE Q3 2014 Presentation.

Services margins, at 30.6%, are double the weighted segment average of 15.1%. But the two go hand in hand, so a boost in services will drive the overall average upward over time. From 2013 to 2014, for example, GE boosted overall operating margins from 15.4% to 16.3% primarily by leaning into its services opportunities and wringing out some overhead costs.

Why you shouldn't worry as a GE investor

Given the opportunity to enhance profits, it's no surprise that 2014 is shaping up to be the year during which GE gets really serious about services. And, in a roundabout way, the Alstom acquisition is a prime example of this shift.

With Alstom, GE will cast its net a little wider in terms of the current installed base. Equipment backlog will also get a boost. Taken together, these two things allow GE to pitch industrial Internet software services like "Predix" to an expanding group of global customers.

For shareholders like myself, big acquisitions like this one mean there's less capital available for dividends and buybacks. But that's fine with me. GE's reinvesting in an area of the business that generates returns well beyond its cost of capital -- and probably beyond the returns I could find elsewhere in today's market. The opportunity for growth plus a healthy dividend yield of 3.41% is something I'll take any day of the week.