Bring up retirement planning and one of the first things a lot of people will think of is Social Security. And while this important social safety net plays a major role in retirement, a recent Pew Research Center survey shows that the majority of people of all ages -- and more than 86% of young people -- believe that Social Security will pay either reduced or even no benefits when they retire.

Source: Pew Research

In light of this, you'd think an increasing number of people would be saving for retirement, but it looks like that's not the case. A recent Bureau of Labor Statistics study reported that only 48% of people who worked in the private sector participated in an employee retirement plan. Let that sink in for a minute. Of the approximately 117 million private-sector workers in the U.S., potentially up to 61 million don't participate in a retirement plan through their work.

Let's dig deeper into the data, because there are some troubling trends at work, especially if the fears of the majority -- that Social Security won't be able to support them in retirement -- become a reality. With that said, if you fall into the category above, there are things you can do now to change your situation for the better, even if you don't have access to a retirement plan at work.

One-third of private-sector workers don't have access

According to the BLS data, only about 65% of all private employees have access to a retirement plan at work, compared to 89% of state and government employees. Filtering further down, 74% of private full-time workers have access to a plan, versus 37% of private part-time employees. Furthermore, it's important to note that this includes both Defined Benefit plans such as pensions, that are wholly funded by the employer, as well as Defined Contribution plans, like 401(k) plans that are typically funded from both employee and employer contributions.

Looking further, when combining the private sector with state and local government employees, only 64% of full-time employees participate in a retirement plan at work. So we are talking about 43 million full-time workers not saving for retirement through their employer, with 26 million of them not participating because their employer doesn't offer a plan.

Service industry workers tend to have the lowest retirement account participation rates. Source: Annette Bernhardt via Wikimedia Commons.

Small business employees, low-wage earners least likely to participate

Only about half of those that work for businesses with less than 100 employees have access to a retirement plan, and barely more than one-third of those employees are participating.

Of those whose wages are in the lowest 25% -- the group that is also most at risk of poverty in retirement -- less than one-quarter participate in a retirement plan. Of this group, only 41% have access to retirement through work, and only 53% of those with access participate.

Trying to reason out the "whys and why-nots"

While there are a lot of reasons people may choose not to participate in a employer-sponsored retirement plan, the following three come to mind as likely:

- Can't afford to

- Afraid of losing money

- The investment choices are bad. I can do better on my own

Starting with the first reason, the reality is, most people just can't afford not to contribute at least something if you have access to a plan. The majority of plans available are 401(k)'s, which will actually reduce your taxes, because the deductions reduce your taxable income. Furthermore, there is significant data that shows how people tend to adjust to reduced take-home pay when contributing to a defined contribution plan. Last but not least, since most employers will match a portion of your contributions, you are leaving a lot of money on the table. I'll show you how much just below.

When it comes to fear of investing, this is another situation where the data doesn't support this popular concern. The 24-hour financial news cycle bludgeons us with constant and largely meaningless data that's more about attracting viewers than anything else. The data, on the other hand, shows that long-term stock investing is one of the best tools that most people have access to, when it comes to creating wealth. While the short-term volatility can be scary, the long-term growth of corporate earnings has meant an average annualized return for the stock market of around 8% over the past 50 years.

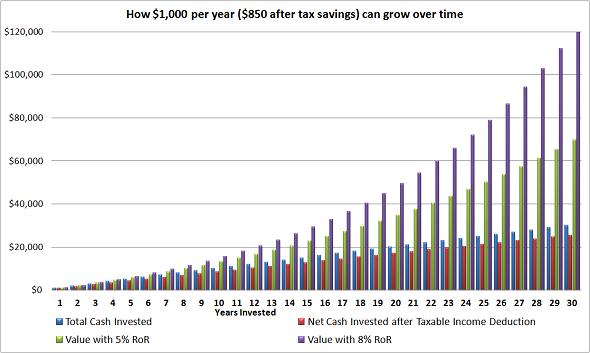

What does 8% annualized mean? It means you double your money about every nine years. Saving $1,000 per year at 8% return over a 30-year career, would net $122,000. Even a 5% rate of return would turn that $30,000 into $69,000. Furthermore, the tax savings would mean your actual "out of pocket" would really be about $25,500.

Even small amounts of money over time can make a big difference in later years.

Bad investment choices in your company's retirement plan? Well, there's some validity to that, as there is evidence that many mutual funds -- which make up the majority of investment options in retirement plans -- tend to underperform the market. However, the benefits of a 401(k) often far outweigh the detriments.

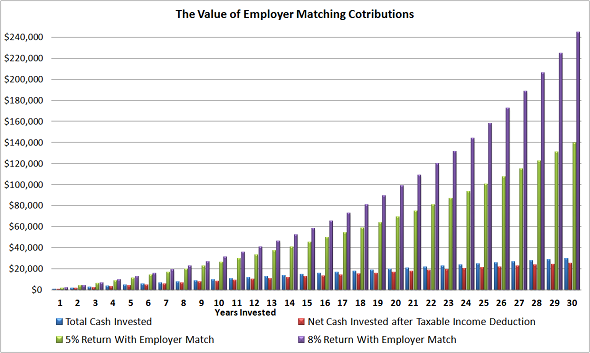

How important are employer contributions? According to a Department of Labor study, employees contributed $185.7 billion to Defined Contribution plans in 2011, while employers added $122.1 billion, good for almost 40% of total contributions. Between the tax benefits and the employer match, it's downright hard to fathom why anyone would not contribute at least something. Here's how powerful employer matching funds can be over time:

Just to emphasize the point:

That's turning $25 thousand into a quarter-million.

But even a small amount -- $50 per month -- can make a huge impact in retirement. Over 30 years, we're talking $73,000 at an 8% rate of return, from only $18,000 in contributions.

Options for those without a retirement plan

Around 26 million full-time employees don't have access to a retirement plan through work, but that doesn't mean you're left out in the cold. Alternatives like a traditional or Roth IRA will let you save up to $5,500 ($6,500 if you're 50 or over) every year for retirement.

And much like a 401(k), your contributions to a traditional IRA can reduce your taxable income, depending upon how much you earn. While a Roth IRA doesn't reduce your taxable income, it grows tax-free, like a traditional IRA. The biggest benefit of a Roth is that you don't pay taxes when you take distributions in retirement. Furthermore, it's easy to open an IRA with an online broker, and you can set it up to automatically take the contributions from your bank account on a schedule.

Long-term outlook

The majority of people believe that Social Security will pay smaller benefits in the future than today, but the same survey also reported that a solid majority of people -- this is the interesting thing -- across every age group, believe that benefits should not be cut. Either way, relying solely on Social Security for retirement is both risky, and almost a guarantee that you won't have the quality of retirement you want.

No matter your age -- only a year into your first job, or a few years from retiring -- setting aside as much as you can for as long as you can will improve the quality of your retirement. If you can take advantage of an employer-sponsored plan, fantastic. If you don't have a company plan, or can't contribute very much, that's no excuse to do nothing. The power of compounding returns will grow any amount of money over time.