2014 has marked a terrible year for the offshore drilling industry with shares of Transocean (RIG 1.63%), Seadrill (SDRL), Ensco (VAL), Noble Corp (NEBLQ), and Diamond Offshore (DO), plunging between 35% and 53% due to declining day rates and falling energy prices.

If investors had hoped for a signal of a bottoming in the offshore drilling market Transocean's latest earnings certainly didn't provide any sign of light at the end of this painful tunnel.

Just the numbers

Transocean recorded $2.27 billion in revenue, beating Wall Street expectations by 3.2% but still down 11.3% from last year's quarter.

Net income came in at a shockingly bad $2.22 billion, or -$6.12/share compared to last year's $546 million profit or $1.5/share.

However those horrifying figures are due to a $2.79 billion write down due to a non-cash good-will impairment charge caused by the "deterioration of the market outlook."

When factoring out impairment charge as well as last year's one time charges/benefits the quarter's earnings was $0.96/share, beating Wall Street expectations by 15.7% to 24.7%.

However, despite the earnings beat, Transocean's adjusted earnings per share still declined 30% relative to last year.

Drilling into the numbers

Long-term investors know that any single quarter's earnings aren't nearly as important to an investment thesis as is the overall growth prospects of a company. For offshore oil drillers like Transocean the health of its business requires looking at five key metrics: operating cash flow, fleet utilization rate, revenue efficiency, day rates, and the contract backlog. Looking at Transocean's results from this perspective indicates that the company's (and the industry's) pain is likely not yet over.

Cash flow from operations (a measure of cash generated by normal business operations) was up 38.7%, and the average day rate increased 4.5% over last year's rate. However, all other vital metrics were down and down substantially.

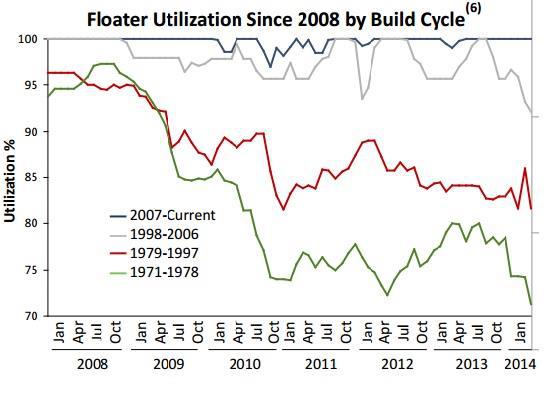

- Fleet utilization 75% vs. 78% last quarter, and declining from 83% during Q3 2013 and 94.9% in Q3 2012

- Revenue efficiency was 92.6% vs. 95% last quarter

- Contract backlog of $23.6 billion vs. $29.8 billion last year

The lower revenue efficiency, which measures actual revenue received versus potential revenue, is a measure of how efficiently an offshore driller can maintain its fleet and declines as a result of increased rig down time. Transocean's revenue efficiency indicates that its aging fleet of rigs, which typically break down more often and require more maintenance than newer rigs, is hurting its bottom line.

This was made plainly obvious by the enormous write down the company reported, much of which was due to declining values of its older equipment.

The aging fleet is also negatively affecting fleet utilization, both in terms of keeping rigs running, but also due to the fact that demand for older rigs is far lower than for newer, safer, and more state of the art rigs.

Source: Pacific Drilling May 2014 investor presentation.

The lower demand for aging rigs, in addition to the large number of rigs Transocean has going off contract within the next two years is the reason Transocean's backlog contracted by 20.8% in the last year. As seen in the below image, Transocean's contract cliff is the worst of any of the major offshore drillers. For example, 10 rigs are currently without contract, idle or cold stacked, (meaning in storage)and only 19% of its most important rig type, Ultra Deep-Water rigs (which contributed 71.2% of its revenue this quarter) are contracted past 2016.

Source: Seadrill Investor presentation.

What to watch going forward

During the conference call Transocean's management warned that the combination of cyclical market downturn caused by an oversupply of new rigs, in accordance with the 27% decline in oil prices over the past 90 days, means that day rates will likely continue to face pressure and force the company to retire and write down additional rigs.

Transocean investors will want to keep a close eye on day rates for new contracts secured, which are expected to decline over the next several quarters. If day rates decline much lower (they have already fallen 11% below management's worst case scenario for its older rigs) Transocean will be forced to retire rigs at an accelerated rate, which would help utilization rates but hurt revenue and operating cash flow.

In addition management announced that its previous plan to spin off some of its older rigs into a separate company called Caledonia, have been put on hold due to challenging market conditions. Caledonia's sale would have provided much needed cash to help Transocean pay off some of its upcoming debt as well as secure its dividend.

That dividend, which currently yields 10.1%, costs the company $272 million per quarter.

Given this quarter's operating cash flow of $882 million and interest expense of $122 million,investors will want to keep a close eye on operating cash flows going forward. If the combination of dividend and interest expense climbs much higher than the current 45% of operating cash flow, then the probability of a dividend cut will increase.

Takeaway

The pain in the offshore drilling sector isn't yet over and seems likely to get worse before it gets better. Transocean's most recent earnings are clear evidence of this and investors in the industry should keep a careful eye on day rates, utilization rates, and operating cash flows going forward for evidence of an eventual bottoming or warning signs of a possible dividend cut. For income investors willing to take on more risk, Transocean represents a potential long-term investing opportunity but potential investors need to be aware of the harsh industry conditions and allocate their holdings in this company accordingly.