On the hunt for dividend income? Look no further than this company you may have never heard of.

The bank worth buying

Banks have rightfully drawn the ire of investors of late, and many have wondered if banks should be avoided altogether as investments.

Source: Flickr / c_ambler.

But there are always exceptions, and for investors looking for a company that pays a reliable dividend with remarkable safety and a proven ability to generate returns to shareholders, then they need to look no further than New York Community Bancorp (NYCB +0.81%) -- which delivers a 6.5% dividend -- and there are three key reasons why.

1. Supreme safety

NYCB operates predominantly in the niche New York City multi-family loan business -- lending to apartment buildings and the like -- with 70% of its total loans held for investment in this one area.

The company focuses on making loans for buildings "that are subject to rent regulation and feature below-market rents," which are "made to long-term property owners with a history of growing their cash flows over time by making improvements to the apartments and common areas in their buildings which, in turn, enables them to increase the rents their tenants pay."

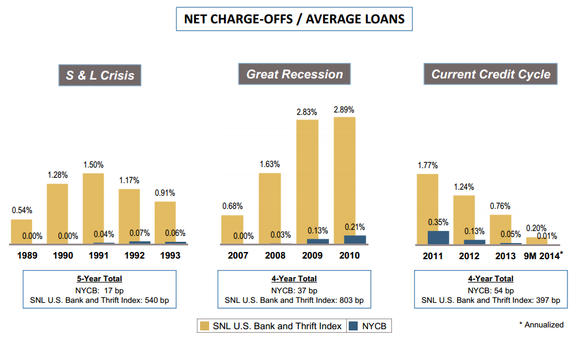

As a result of such a unique and defined business model, the company has become a market leader. And thanks to its expertise in this space, it has also been one of the safety banks over the last 20 years, with an unheard of net-charge off rate -- the amount of loans a borrower defaults on -- of 0.04% since 1993.

And this has been true in the best of times and the worst of times:

Source: NYCB Third Quarter 2014 Investor Presentation.

Thanks to questionable lending practices, banks can often be some of the riskiest investments on the market, but that simply isn't the case with NYCB.

2. Incredible returns

There is always a trade-off between risk and return, so knowing NYCB has been among the safest banks, it is easy to assume it hasn't generated the returns investors would hope for.

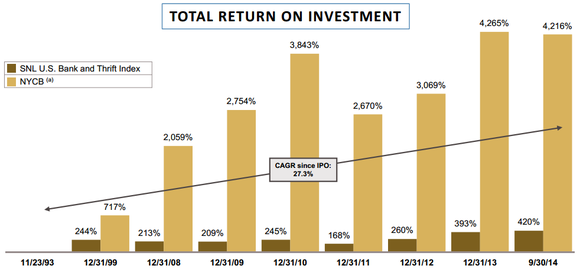

But that simply has not been the case, and from the time it went public in November 1993 until the end of September of this year, it has delivered and astonishing return of 4,216% to its initial shareholders:

Source: NYCB Third Quarter 2014 Investor Presentation.

As you can see, this is more than 10 times greater than that posted by peer banks over the same time period.

Investors must know it isn't just that the disciplined underwriting practices have insulated NYCB against risk, but those very same practices have enabled the company to pay a steady and reliable dividend, which has also propelled it to provide incredible returns.

3. Incomparable efficiency

The final thing that should put NYCB on investors radars is its incredibly efficient operations. Its efficiency ratio -- which measures the cost of each dollar of revenue -- of 43.3% in the third quarter was more than 20 percentage points lower than the 63.8% posted by all banks in the SNL U.S. Bank and Thrift Index.

As fellow Fool contributor and Senior Banking Specialist John Maxfield noted:

There are an endless number of metrics one can use to pick a bank stock. But none is more important than the efficiency ratio ... It's worth noting, moreover, that the relationship between high returns and a low efficiency ratio goes beyond the obvious. Namely, because banks with lower ratios are innately more profitable than their less efficient peers, the former have less incentive to stretch for yield by underwriting dubious loans.

In other words, in one of the most consequential measures of a bank's profitability, NYCB handedly outperforms its peers.

And when you throw in the fact that despite its outperformance, NYCB currently trades at a very reasonable 2.2 price-to-tangible book value multiple -- versus the peer average of 1.8 according to S&P Cap IQ -- then that is simply icing on the cake.

Of course, past performance is no guarantee of future success, and there are a lot of companies with massive dividends, but if you were looking to find one to buy today, you'd be hard pressed to find a better investment than New York Community Bancorp.