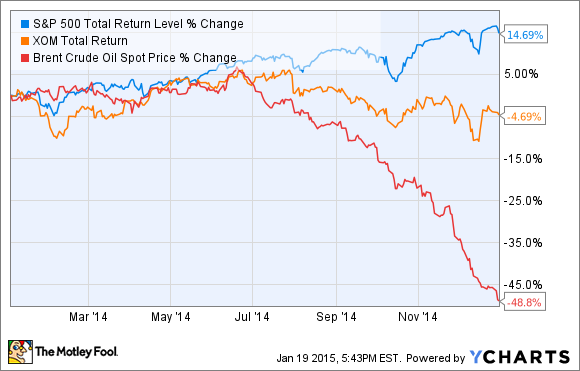

There was no joy in Mudville last year for energy investors, thanks to the epic tumble in oil prices that started in the summer. Even ExxonMobil (NYSE: XOM), the standard bearer of the entire industry, the one company with the complete business model built to handle commodity price swings, saw its stock value drop by 7% even as the S&P 500 rose by an impressive 14.7%.

What made this especially discouraging for ExxonoMobil was that 2014 was supposed to be a period of transition for the better. But the party was spoiled by nervous investors who fear the oil rout might be deeper and longer than many of us would care to think about.

Just when things were starting to look good

Leading up to 2014, ExxonMobil and many of its peers were spending way too much money in an effort to grow production. Unfettered spending was so 2008, when the price of oil reached up to $130 a barrel and the world was terrified that we were on the cusp of peak oil. Just before 2014, though, stable oil prices around $95-$105 a barrel meant excess spending for production would eat into free cash flow big-time.

Source: ExxonMobil Investor Presentation.

In response to the changing price climate -- and the anger of some shareholders -- ExxonMobil announced that 2013 would be a peak year in capital spending, and that the company would spend less over the next couple of years as several major projects came online. This would allow the company to generate more free cash flow to give back to shareholders.

This was actually starting to take place, too. Through the first nine months of 2014, the company generated $19 billion in cash flow from operations -- 61% more than the free cash flow generated in all of 2013 and enough to cover its planned dividends and pre-approved share buybacks.

Source: ExxonMobil Investor Presentation.

Oil prices, the giant-slayer

Despite these promising signs, the fall of oil has taken its toll on ExxonMobil's stock. For the most part, the impact of the near-50% plunge hasn't really sunk its teeth into the company's earnings yet. In the third quarter, ExxonMobil collected earnings-per-barrel equivalent of $18.85, which was not that far off the first quarter's per-barrel earnings of $21.35. Also, the company offset some of these losses with big earnings increases in its refining and chemical operations.

ExxonMobil's fourth-quarter earnings will give us a better idea of exactly what oil prices mean to the company's overall earnings. The average price of Brent crude in the fourth quarter was in the $75-$80 range, significantly higher than where we are today but a sizable discount to the third-quarter price.

What a Fool believes

In some ways, ExxonMobil chose the perfect time to focus on free cash flow in 2014. With oil prices plunging, it's encouraging that capital spending was already winding down and will not have as significant an impact on the cash flow statement. Hopefully, the combination of its vertically integrated business model and its efforts to minimize capital spending will mitigate the impact of declining price realizations for the coming year.