Note: This article was originally published on Jan. 26, 2015, and updated on April 8, 2016.

Ask most people what their net worth is and they probably don't know. Show them how to calculate it and they'll be dying to know how they compare to their peers. In the blink of an eye, "net worth" went from an unknown variable to a characteristic that defines you as a person.

That's not a healthy stance to take. When we become too tied to our financial situation, we can lose sight of everything else that's important in life. As cliche as it sounds, once your basic needs are met, the most important things in life really are free. And for those who don't like such platitudes, tons of research has backed this up.

Image source: Getty Images.

In many ways, viewing your net worth is like watching your weight: it's healthy to set reasonable goals that make sense for you and your current situation. Comparing yourself to others only helps if you're getting started and struggling to get a feel for where you stand.

That's my disclaimer for what I'm about to show you below. Knowing your net worth can -- in fact -- be important, but in a limited scope. It lets you know exactly where you stand financially. It allows you to see if you are making progress to your financial goals. And when it's time to buy life insurance, it helps you determine what level is appropriate for you and your family.

How to calculate your net worth

Net worth is calculated by taking everything you own (stuff, cars, houses, investment portfolios, etc.) and subtracting out everything you owe (college loans, mortgages, credit card debt, etc.). For the purposes of this article, we won't be including pension plans, the cash value of life insurance policies, or the value of household furniture or jewelry in our calculations.

Take a minute and think about everything you own and owe. The things you own are called assets and go on one side of the sheet. The things you owe are called liabilities and go on the other. Take a second and think about your assets and liabilities. Write them down. Use this sheet [opens a PDF] if you need to.

If you're confused about the car you've borrowed for or your house that has a mortgage, put the fair value of those things in the "Assets" category, and the amount you still owe in the "Liabilities" category.

Where do you stand?

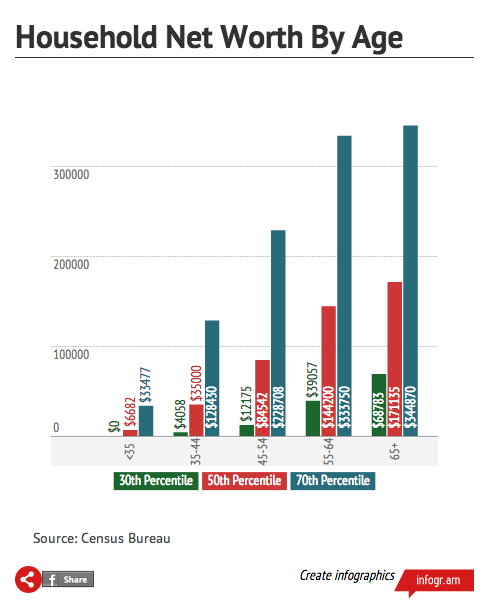

Back in 2011, the U.S. Census Bureaupublished a report breaking down the median household net worth by age and in quintiles. Because I only think comparison is a valuable tool to get a very broad feel for where you stand, I've excluded the lowest and highest quintiles. What's left is the 30th, 50th, and 70th percentiles.

The plain English explanation is this: the 30th percentile means that if you have exactly this net worth, it is greater than 30% of households your age. The same is true for the 50th and 70th percentiles.

So, broken down by age groups, here's what the median American's net worth looks like:

For many in the older age categories, the value of one's house and property account for a large swath of overall net worth. That's important to note, because -- unless you have a hospital and a farm on your property -- your house can't help pay the food and health bills in retirement. Downsizing might make more sense to free up cash. Clearly, the younger you are, the lower your net worth will be. This is not only due to lower salaries and higher student debt loads of the young, but also a result of them taking on new mortgages.

And if you're in the 50th percentile, and over the age of 65, it's important to know that even if all $171,135 of your net worth is in cash and investments -- that will provide less than $7,000 per year in living expenses. That might work for some, especially after Social Security, but for many others it could be a rude awakening.