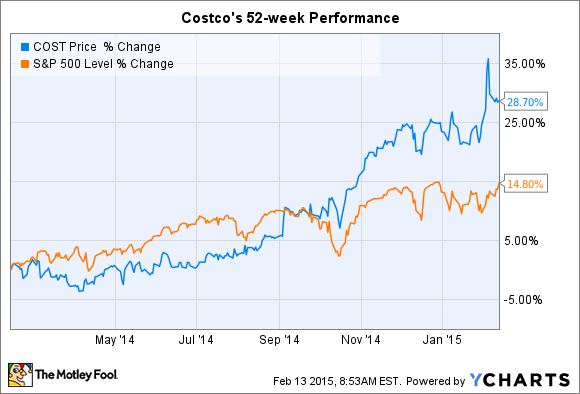

Costco's (COST 0.13%) stock touched an all-time high this week of $151. It then quickly dropped after the retailer sent out a $5 per share special cash dividend to investors.

Even with this week's fall, the stock has trounced the S&P 500's performance. Costco's valuation also hit a rich new high at 31 times trailing earnings.

But at least one Wall Street pro thinks that shares have more room to run this year. Morgan Stanley analyst Simeon Gutman recently boosted his price target on Costco's stock to $163, which would equate to a further 10% gain from here. Let's take a look at why Gutman is so bullish, and whether $163 per share makes sense in light of Costco's business momentum.

All about the millennials

In his price target hike, Gutman focuses on dismantling the bear argument that Costco has a looming demographics problem. The warehouse giant currently enjoys an affluent customer base that skews older. And while that's good news for the business right now, it points to sales growth declines over the long term unless Costco can find a way to appeal to younger shoppers.

Further, Costco's results could take a hit if and when more millennials start filling its aisles. With lower spending power and less brand loyalty than its existing subscriber base, young shoppers threaten to drag down average check sizes and renewal rates for the business as a whole.

Source: The Motley Fool

But Guzman argues that Costco's business should do fine as it transitions into serving more millennials. Yes, they'll spend less -- to start. But over time their spending power will grow, as will their connection to the Costco brand. Soon enough they'll start to resemble the company's current member base. And whatever the business loses with lower average spending in the short term should be made up in volume: Millennials represent the fastest growing segment of the industry.

Costco has already become more appealing to younger shoppers. Its organic foods business, for example, has doubled in the past two years to over $3 billion of annual sales, around 3% of the business. Management sees that gain as just a beginning. Organic and natural foods should quickly climb to a much larger portion of sales as the supply chain allows for stocking more bulk products in the category.

Meanwhile, operating results haven't shown any evidence of slacking even though the company is picking up organic food fans. Renewal rates climbed toward an incredible 90% last quarter and Costco's same store sales beat all national retailing chains including Whole Foods and Kroger.

A moving price target

But is Costco's stock price already reflecting most of that good news? I think it is, at least in terms of profits. Wall Street expects the retailer to earn $5.17 per share through this fiscal year, for a 12% improvement over 2014. Profit growth was nil that year, but bounced around between 13% and 18% in the four preceding fiscal years.

Sure, Costco deserves a premium valuation. It has a track record of outperforming peers. And its world class management team is focused on delivering long-term growth. But the stock can't keep growing faster than the business forever. A 10% price gain implies expansion in Costco's valuation further above 30 times trailing earnings. So, while another big gain in the stock is possible, I wouldn't count on it given the current rich valuation.