Clean Energy Fuels (CLNE -15.32%) is the leading supplier of natural gas for transportation in the U.S., with hundreds of stations across the country. Over the past year, the company's stock has been absolutely hammered, even as the core business has grown. Motley Fool contributor Jason Hall met with Clean Energy co-founder and CEO Andrew Littlefair in April 2014 and conducted an in-depth interview that you can read here. Littlefair agreed to a follow-up phone interview, covering the many changes in the industry and to Clean Energy's business since last year.

The transcript follows, edited for clarity and length.

Commodity prices affecting Clean Energy stock price, but short-term movements might be missing the bigger picture

Jason Hall: Andrew, thanks for taking the time to speak today. Let's get this out of the way: The stock price has been hammered since we met last year.

Clean Energy co-founder and CEO Andrew Littlefair. Source: Clean Energy Fuels.

Andrew Littlefair: For us, we are really tightly correlated to oil this year. It's at, like, 95.6% correlation to oil. If you go back to a year ago, it was about 60%. A year before that, it was 30%. The market's got us tied to oil, and I get that, but I don't know that's exactly the right way to look at it. You know, natural gas has come way down, too.

Hall: Yes, it was at $4 per Mcf [thousand cubic feet] for much of last year, and now it's way down.

Littlefair: And that's what we use, and to the context that diesel -- which hasn't come down like oil -- is down. So natural gas coming down from $4 to $2.65 today, that trims $0.18-$0.20 per gallon on the commodity side.

Hall: And you typically buy your natural gas on the spot market. You do hedge some for certain contracts, but the majority is at market prices, correct?

Littlefair: Right. Most of it is spot-market; we don't hedge hardly any. We have a couple of legacy [deals] where we've bought some gas futures, but it's really tied to a contract, so it's sort of a pass-through. So we are benefiting from the spot market [for natural gas] coming down.

They are laying some of these rigs [for natural gas drilling] down, so you're going to have some impacts associated with gas, and it's winter -- I keep watching these poor folks in Chicago and Boston shoveling snow -- but as we get into March and April, it wouldn't surprise me at all if we saw natural gas prices remain low.

Hall: A concern I have with the oil and gas industry is ... so we are starting to see rigs come off of the oil wells. Do you think some of these independents start moving over to gas production?

Littlefair: No -- that's the only reason the gas won't totally fall out of the bed. I don't think you'll see oil rigs go drill for $2.50 gas. And when you lay down some of those rigs -- and they're coming down fast -- that could impact some gas that comes up as a byproduct of oil production.

Basically, we're neck-deep in gas. That's just where we are. There was some concern about a year ago -- the polar vortex -- gas reserves were at a five-year low. Some people thought we would have $5 natural gas, but you know, they filled up the reserves pretty good.

Overall business continues to grow despite oil price collapse

Hall: Let's talk about where things are with the overall business.

Littlefair: I know the deal with oil prices plummeting has sort of covered it up, but the business is doing well. The company is strong. The balance sheet is strong. Our core business grew at about 21%. We continue to grow. We had our biggest year ever in the refuse sector. I'm sure we will talk about this later, but we haven't had a single customer tell us "we're outta here" because oil prices are down.

Clean Energy isn't losing customers to gasoline or diesel. Source: Clean Energy Fuels.

We are a little different than some of the businesses in our sector: We have a recurring revenue stream. If some guy buys a natural gas trash truck, he's not going to change that thing to diesel. He might not be saving the $1.90 per gallon he was a year ago, but he's still paying $1.30 less than diesel, and he's going to keep that truck for 10 or 12 years.

We haven't seen any backing away in that segment; in fact it's the strongest it's ever been. We saw the biggest growth in that particular segment [refuse] of our business that we've ever had, and that's going to look pretty good going forward.

It's the same case in the transit sector. There are some significant deals in the works for public transit. That's good, because we are in that business. Not everybody in this industry can say their core business is growing 20%, 21% like we can.

Let me be candid: If you were to tell me we would have $44 oil for the next few years, that would start to have some impact. Let's not kid ourselves. But diesel here in California [Clean Energy is based in Southern California] is $3.16 per gallon. It's come down from $4, but it hasn't come down like gasoline, and we are still able to offer those heavy trucking operators a savings.

Heavy trucking adoption slow, but showing some growth

Hall: Let's talk more about heavy trucking.

Littlefair: The price differential has come down. We might not be able to give that $1.50 per gallon savings,, but we are still able to get in the $1 range in cost savings. We are focused on doing things to help drive down the incremental price of the trucks. We are doing a lot more today than we were the last time you and I met.

We talk a lot about shippers like Procter & Gamble and others telling the trucking companies they work with that they want to move to natural gas, but one challenge that has emerged is a shortage of drivers. That's putting pressure on the shippers, and freight rates are actually going up because of demand. I think this is the main concern today.

I'm not saying you won't see some decide to stay with diesel, but what's more likely as we're working with these trucking companies is they may come back to us looking for lower fuel costs, and we do what we can. I would say that the general trucking -- and refuse and transit -- they don't think you're going to have super-cheap oil for a very long time.

Hall: They know how the volatility works.

Brent Crude Oil Spot Price data by YCharts

Littlefair: They've seen it [in the past]. And I'm not saying that they have a crystal ball, but most of them know they we will have more expensive oil in the second half of the year than we do now.

Hall: That's the general consensus, but what it's going to boil down to is American producers, and how fast they take their foot off the gas [and slow oil production].

Littlefair: And they're doing it. Historically, when you see this kind of a drop in the price of oil, the U.S. responds by cutting 50% of the rigs. I think last week we saw the biggest weekly reduction in the rig count in a long, long time. The week before that was pretty big. So you're starting to see these things come down.

Some of the bigger names -- I can't really say anything specific today -- but some of the big truck operators are starting to move ahead with orders for natural gas trucks now. These guys look out into the future and see that natural gas still makes sense.

NG Advantage and Joint venture with Mansfield offer exposure to new markets

Hall: Let's talk about NG Advantage.

Source: Clean Energy Fuels/NG Advantage.

Littlefair: We bought a controlling interest. In the Northeast, there are places where there are no pipelines, and you have industrial users and hospitals that use fuel oil.

Hall: I had a 100-gallon oil tank in my cellar when I lived in Massachusetts. I'm very familiar.

Littlefair: Those of us out here in the West just can't imagine it. NG Advantage -- it's pretty exciting -- they use our IMW [Clean Energy's compression manufacturing business] equipment, and the customers are really big customers.

For instance, we won a recent deal with one customer worth 10 million gallons a year. When we won the deal, they figured a 40% savings versus fuel oil. With oil prices further down, they figure they'll still save 30%.

For the end users -- one example is a local hospital up there -- they might spend $400,000 to outfit their facility to use natural gas, but they'll save that much versus fuel oil in the first year.

Hall: So versus transportation, where the payback for more expensive NGVs [natural-gas vehicles] can take several years, the payback is faster?

Littlefair: It's pretty quick. And what's nice for us is the volume is big. The Milton [New Hampshire] station, I announced last week, did 53,000 gallons in one day.

Hall: Are there any concerns about throughput at the stations that supply NG Advantage?

Littlefair: Not at all, as long as we manage the timing on resupplying customers and fill-ups. And we have the advantage of having other stations in the area that we could use to meet demand.

There's a good guy that's running it; he has a big stake in it. Our focus is to add one or two large industrial customers every year [as anchor customers to support new stations], and we will have a pretty good business.

Hall: Let's talk about expanding that business, versus, say, the America's Natural Gas Highway [ANGH] stations, where there are still dozens of built stations that aren't open yet.

Littlefair: To start off, this is contracted volume. So you're not talking about building a $10 million "spec" station. You're starting with a [base] load from an International Paper, or you've got a few hospitals lined up, that sort of thing.

It's the same thing with our Mansfield partnership.

Hall: Let's talk about that.

Littlefair: We're not spec-ing any of those stations. We opened our first one in Doraville Ga., with 33 trucks the first month.

The interesting thing about Mansfield is, they take diesel and gasoline, and drops it off at customers that have back-lot fueling locations. They're pretty big -- they do 3.5 billion gallons per year, using 900 haulers that make 3,500 deliveries daily.

He's [Mansfield owner Michael Mansfield] built that thing into a pretty big thing. The nice thing about Mansfield Clean Energy Partners is that the focus is putting stations at terminals, where these trucks go to pick up fuel on a daily basis.

So Mansfield already works with 900 of these truck operators, so in a way they are the shipper, and we are in the early throes of Mansfield working with the haulers he contracts, to talk about making the switch to natural gas.

Hall: As I understand it, Mansfield is the dominant behind the gate supplier, right?

Littlefair: That's right. So if you're a company with 150 trucks hauling fuel for Mansfield every day, you're likely to listen if they want to talk about switching to natural gas.

And it's not like we're reinventing the wheel here. They know who the potential customers are. Our part of the exercise is building the stations, and to know the economics of where the stations will work. We've already done a lot of the work to identify where we target it. And it should be a nice business for us. We're already building our second station. Eventually this will be a nice vertical for us, and with a captive audience.

Hall: In a way it's like some of that transit business, where you own it because of the locations of your stations, versus the retail stops that can be more subject to competition.

Littlefair: I see it like our airport stations. If we get the contract with the airport, we get the terminal buses, we'll also get the hotels, and often the taxis as well. It's not easy for someone to build a $2 million station around the corner.

So once you put a station in at these fuel terminals, you're way ahead of the crowd.

Hall: So it's a pretty durable competitive advantage.

Littlefair: Yeah. You won't see crazy growth on it; it's going to be slow and steady. We are doing it with a methodical approach. But it's another vertical market for us, with one of the biggest names in the business [in Mansfield].

Refuse, on the other hand, we will build or upgrade around 40 stations this year. That business just continues to grow.

Taking steps to strengthen capital position; improve cash flows

Hall: Let's talk about capex [capital expenditures], and how you are going to deal with the rate of cash burn. You've funded a lot of stations that aren't paying anything back right now.

Littlefair: As you know, we've spent a lot of the money needed on the ANGH network, and some strategic locations we believed were important. That money has already been spent. We aren't faced with spending another $100 million to build that, or with any of our other markets.

I know there's concern. People will say, "Oh, my God, they always spend $100 million every year, and they've only got so much left. They're gonna run out of cash to fund the business." I get that. Capex this year -- I've said it before -- 2014 was around $85 [million] or $90 million, and this year will be less. I'm not going to let you steal all my thunder for the earnings call, but it will be a lot less.

Hall: And looking back at last year, initially you planned to spend $135 million, before cutting that back early in the year to the $90 million target.

Littlefair: So if you look at what we have on hand, in addition to our cash we will spend, we will also have some grant money that will help pay to build stations for some customers. But from our cash we will spend, it will be much less in 2015.

Hall: And as you said, that capex will fund expansion that's tied to new business, not speculative.

Littlefair: That's right. It's all stuff where we have contracts where customers are committed to buy fuel from us. Also in there will be some capital to open some ANGH stations. We have to commit $50,000 or so each to get them ready, and at some stations that we are adding CNG [compressed natural gas], and some of our CNG stations where we are adding LNG [liquefied natural gas].

Now, when you look at where we stand [with capital], we got the renewal on the VETC -- and it's now called the "Alternative Fuels Tax Credit" -- that came in at around $27 million or more. We will recognize it in the fourth quarter. And we also sold our share of the McCommas landfill in Dallas. Essentially it was a good deal, and that will add a lot of cash back. So we ended the year with close to $215 million in cash, so that's kind of where it starts.

Status of GE contract for liquefaction plants for LNG

Hall: Let's talk about the General Electric Co. relationship -- specifically the deal for new liquefaction plants that was signed several years ago. Right now it doesn't look like you'll need that LNG volume anytime soon, and that deal was set to come due soon.

Littlefair: We made that deal with GE a couple of years ago, and at the time, we thought trucking would grow faster than it has, and we weren't altogether sure how much LNG we would be able to source around the country. When we first started sourcing it, we were buying from six locations. Today it's 27 different locations. We have a guy who's done a [good] job lining up as much as 485 million gallons per year of LNG supply.

I still think we are going to need those plants, but with the truck market slow, and us having done a good job lining up LNG supply, GE agreed to give us a two-year extension on pulling the trigger on the plants. We weren't ready to make a decision at the end of the year (when the GE deal originally required), and we continue to have a good relationship with GE.

Hall: So it made sense for you and GE both to ...

Littlefair: Just push it out.

Hall: OK.

Littlefair: You know, GE didn't want me to go build a plant that wasn't going to be utilized, either.

Hall: That makes sense.

More on heavy trucking, and the competitive landscape

Littlefair: Let's talk a little bit about ANGH. When I first read your email to Tony [Kritzer, Director of Investor Relations] where you called the ANGH "bad" so far, I almost had a nervous breakdown. I started shaking when I read that.

Hall: [Laughs] It hasn't been bad?

Littlefair: You know, if I had it to do all over again, maybe we do it a little later, or maybe build a few less stations based on the speed of the trucking industry. But having said that, we changed the discussion between the shippers and the truckers.

We had to take a lot of flak last year, and then there was misinformation about CNG versus LNG that we had to deal with, but we will be announcing some of our biggest LNG deals ever this year. I'm not ready to call it yet on ANGH. At this point we continue to see mostly regional haul business, but we are slowly starting to see the long-haul users increase interest.

In 2013, we had 22 of the ANGH stations opened, and we opened 16, with two opened so far this year, with another 10 in the process of opening. That means soon we will have 46 unopened, and hopefully by the end of the year it's 20-something unopened.

And actually, this business is not so fun for a bunch of my competitors right now. We keep track of the competition. Now a lot of these guys really aren't competitors -- you have small or regional players who open one or two CNG stations at a Circle K ...

Hall: They don't have any benefits of scale.

Littlefair: And no expertise. To build an $800,000 station at a Circle K and try to go line up business from local fleets, that is just brutal. You're going to see a lot of these guys in between who have announced some planned stations end up putting them on the shelf. When the smoke clears, it's going to be pretty clear that we are the leader.

Operating costs, debt, and looking forward

Hall: So looking ahead ...

Littlefair: In a nutshell, we are going to watch our capital, open all of the ANGH that we can, predicated on truck deployments, and build stations that are contracted on "anchor tenants," which has always been our core business model. We will continue to grow the core markets.

In the last year, we have reduced overhead.

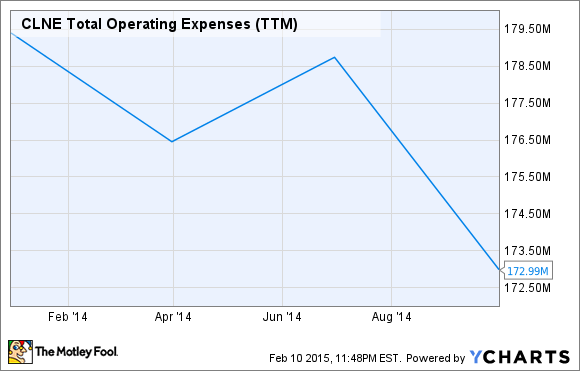

Hall: I have seen a trend over the past year where operating expenses have come down.

CLNE Total Operating Expenses (TTM) data by YCharts

Littlefair: That's right. And as much as I hate to do it, we had to trim headcount to right-size some things at the end of the year. So it will continue to come down.

You'll see SG&A [sales, general and administrative expenses] somewhat flattish in 2015, with volume growth again. So SG&A percent will come down to more normal levels. We're not taking our eye off that ball.

Hall: What about debt?

Littlefair: We have the notes that we owe on, with the 2016 converts. We are in close communication with the owner of those notes. Without saying too much, we have a plan to address the overhang of those 2016 notes. Once we take care of those, we have notes due in September of 2018.

Hall: You have three and a half years to grow cash flows to hopefully handle some of that concern.

Littlefair: That's right. Look, we're not whistling past the graveyard here. Looking at our balance sheet, and looking at our growth -- would I like to have $100 oil? You bet. But we're doing all the right things to keep ourselves in fighting shape.

Hall: I continue to see your fundamentals look better. Operating expense is down. Based on what you say, it will be two years in a row where capex is down dramatically. Volume is going up. It's also good to hear you have a plan in place to address the debt concern.

Littlefair: Don't get me wrong. I hate the stock price.

Hall: I can imagine -- you've lost more than my entire net worth ...

Littlefair: Yeah, well Mr. [co-founder and largest shareholder T. Boone] Pickens isn't particularly happy about taking a $10 hit on 22 million shares himself. This has been a difficult period, but I own more shares today than any time in the past few years. We'll get it back. I'm not going anywhere.

Hall: Andrew, thanks again for talking with us. Best of luck.

Littlefair: Thank you, Jason.