The results of the FCC's recent AWS-3 auction made one thing extremely clear: AT&T (T -2.92%) and Verizon (VZ -2.01%) are desperate for spectrum. With DISH Network's efforts helping push the total price up by as much as $25 billion over original estimates, both of the big carriers spent what was necessary to get the spectrum they needed. AT&T and Verizon spent $18.2 billion and $10.4 billion, respectively, in the auction. Comparatively, T-Mobile (TMUS -0.48%) remained relatively conservative, spending $1.8 billion in the auction. That's slightly more than originally expected, but less than expected after the auction took off.

This points to the biggest advantage the smaller carriers -- T-Mobile and Sprint (S +0.00%) -- hold over the big guys. They have much more capacity per subscriber. Note that this includes undeployed capacity, like Sprint's 2.5 GHz holdings, as well as the newly purchased AWS-3 spectrum.

Capacity constraints

After the auction, AT&T and Verizon hold an estimated 38% of the industry's network capacity. For two companies that combine to take 73% of the industry's revenue and approximately two-thirds of wireless connections, it's easy to see how they're capacity constrained.

As more people start streaming video and music over their wireless connections, the ability to provide stable network performance is key. As such, AT&T and Verizon will likely keep strict caps on their data plans. In fact, if you look at pricing for those plans, there's a disincentive to purchase capacity over 20 GB. Both companies may further adjust pricing for higher data capacity plans to limit allocation. If they elect to compete on data allocations, service will suffer.

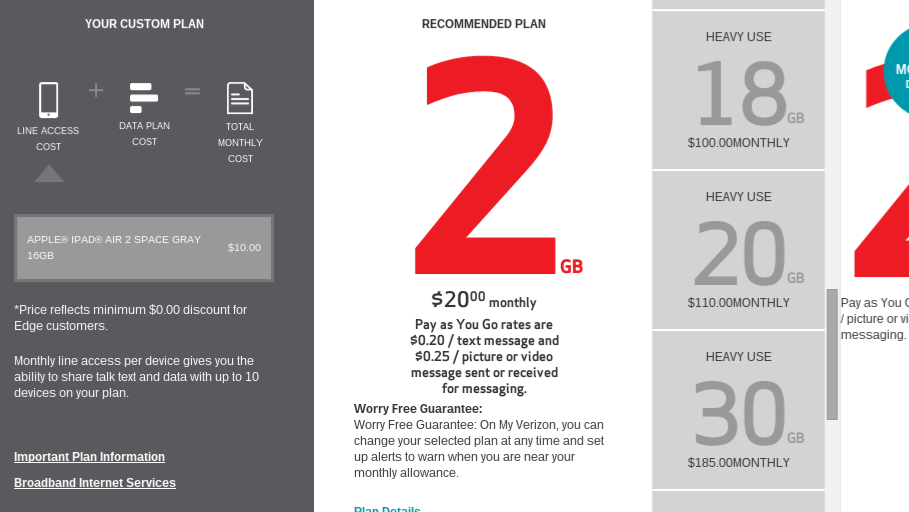

Verizon charges $75 more for the next 10 GBs of data after the first 20 GBs average $55. Source: Verizon.

That opens the door for Sprint and T-Mobile to attract more customers. While both of the companies' networks still lag behind the bigger carriers (now only slightly), they're much closer in large metropolitan areas, where capacity issues surface. This may be especially problematic for Verizon, which missed out on spectrum for large cities like New York, Boston, and Chicago in the AWS-3 auction.

Cash constraints

The problem gets worse for AT&T and Verizon when you consider the amount of leverage already built into those businesses. Both companies have been furiously selling off non-core assets in order to raise cash without taking on more debt. AT&T in particular is on the hook for its $18 billion spectrum purchase, as well as about $50 billion in potential acquisitions, including its plans to buy DirecTV.

Both companies are looking to control capital expenditures in order to increase free cash flow in 2015. AT&T plans to save $3.5 billion on capex, while Verizon is shifting spending more toward its wireless business.

Still, their cash constraints will limit their ability to make deals to purchase or license additional spectrum capacity. It could open the door for T-Mobile or Sprint to make favorable deals with the bigger carriers to swap spectrum like T-Mobile and Verizon did last year.

Opportunities for Sprint and T-Mobile

Holding excess capacity opens up a few opportunities to Sprint and T-Mobile. We saw one such opportunity recently, when both companies reportedly agreed to a deal with Google, in which Google is reportedly preparing to sell wireles service directly to consumers. The deal allows Sprint and T-Mobile to monetize their excess capacity through a wholesale deal for Google's planned MVNO [mobile virtual network operator agreement].

With the cash flow coming in from licensing capacity, both carriers will be able to accelerate the rollout of their undeployed capacity, or build up funds for the upcoming 600 MHz incentive auction. Either way, it puts them on a path to catch up in coverage to the bigger networks and win more customers.

That should scare AT&T and Verizon investors, as they risk losing revenue share if they don't continue to spend heavily on building out their networks and increasing capacity.