When the banking industry fell from its peak at the onset of the financial crisis, Bank of America (BAC +1.57%) arguably took more bumps and bruises on the way down than any other institution.

The stock tanked. Management grossly mishandled public relations during fiasco after fiasco. Customers were put on the backburner as the bank hunkered down.

While many of those bruises have healed, and some of those mistakes have been forgiven, recent surveys have found that the bank still has a long way to go to win back consumer confidence and thrive in the long term.

The public has spoken

Most recently, J.D. Power's Self-Directed Investor Satisfaction Survey found Bank of America's Merrill Edge investment brokerage to be the second worst of the major self directed brokerages. Wells Fargo's (WFC +2.31%) Wells Trade scored the worst. Last year, the two companies were also the bottom two; however, B of A found itself in the bottom spot, and Wells Trade was second-worst.

Poor customer satisfaction is nothing new for Bank of America, though. It's come to be a fact of life for the bank in the post-financial crisis world.

For example, Bank of America led the Zogby Analytics and 24/7 Wall Street "Customer Service Hall of Shame" last year and has made the list every year since 2009.

The American Customer Service Satisfaction Index found B of A to have the least satisfied customers of large U.S. banks in 2014, the fifth time in six years the bank came in last place. Worse yet, Bank of America is the only large bank that hasn't yet returned to its pre-recession level of customer satisfaction.

The list goes on and on.

Public relations nightmare coupled with poor execution

The reason for the public's vitriol and dissatisfaction with the bank is simple: poor execution and a long list of post-financial crisis scandals.

In 2010, so-called robo-signers foreclosed on thousands of homes, sometimes erroneously, putting Americans out of their homes without proper review or documentation. A federal jury found the bank liable for fraud related to mortgages originated and sold at Countrywide, a mortgage company acquired by the B of A in 2007.

Bank of America eventually settled with the Justice Department for $17 billion over these and other illegal mortgage practices in 2013.

The bank's 2011 decision to charge a $5 monthly fee on checking accounts was met with sharp customer backlash.

Even as recently as April of this year, Bank of America was again in the news after settling a global currency market fixing lawsuit filed by a group of private investors. This settlement, totalling $180 million, follows a settlement with the Office of the Comptroller of Currency last year for the same misdeeds for $250 million.

The stock has been on quite a run in recent years, but...

Over the last three and a half years or so, Bank of America's stock has done pretty well despite all of the scandals and the never-ending list of dissatisfied customers. Since December 31, 2012, the stock has risen 188%, more than doubling Wells Fargo (WFC +2.31%), JPMorgan Chase (JPM +2.00%), and Citigroup (C +2.16%).

However, don't be tricked by that seemingly strong performance. Looking at the stock over that short of a time frame is a mistake; the bank's big stock pop recently is much more a function of how bad things got in 2008-2011 rather than any fundamental improvement in the bank's long-term prospects.

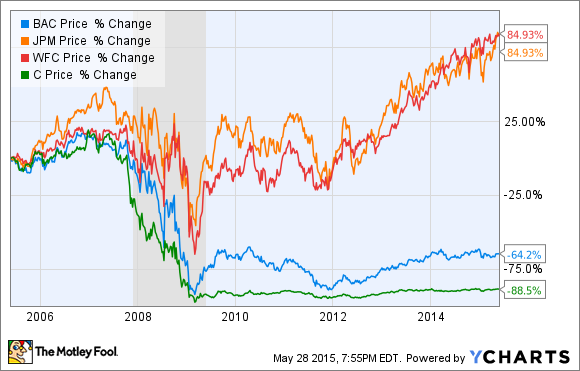

Viewing the stock over a bit of a longer time frame, it becomes clear that long-term Bank of America shareholders have done exceptionally bad, even with the recent bounce.

Taken altogether, I would say it will be another five to 10 years before we can safely say Bank of America has successfully righted the ship. Surveys like the ones highlighted here continue to prove that the bank has a long way to go to becoming an elite financial services institution. My guess is that long-term shareholders would agree.