Source: SunPower.

For all the success the solar industry has had in the last decade, the history of the world's largest solar manufacturers isn't a good one. Q-Cells once led the way, but it was overtaken by Chinese competitors and eventually became insolvent. Suntech Power was China's largest manufacturer until a couple of years ago, but it eventually had to file for bankruptcy as losses piled up.

Now, Yingli Green Energy (NYSE: YGE) holds the title of the world's largest solar manufacturer, and its financial future is in question, just like those that preceded it. Can Yingli survive where others failed, or is it time to bail on this manufacturing giant?

The art of losing money

Now that solar energy is big business and industry leaders are starting to emerge, it's hard to justify being a money-losing enterprise. But that's exactly what Yingli Green Energy is, and the numbers are pretty staggering.

Below, I've outlined the main financial numbers from the first quarter and annualized them to show what they would look like on an annual level. I think this is a better proxy than taking the trailing-12-month numbers because system costs and panel prices are falling, so the year-ago numbers are already moot.

|

Q1 2015 |

Annualized | |

|---|---|---|

|

Sales |

$432.7 million |

$1.73 billion |

|

Gross Profit |

$66.3 million |

$265.2 million |

|

Operating Costs |

$77.0 million |

$308.0 million |

|

Operating Profit |

($10.7 million) |

($42.8 million) |

|

Non-Operating Costs |

($52.7 million) |

($210.8 million) |

|

Net Income |

($63.3 million) |

($253.2 million) |

Source: Yingli Green Energy Q1 2015 earnings and author's calculations.

You can see that not only is Yingli Green Energy losing money on the bottom line, it's losing money on an operating basis. This is important to note because operating losses don't include the cost of financing $2.3 billion in debt. If Yingli Green Energy were built to last, it would be able to cover those financing costs and have something left over for shareholders.

What's even more concerning is that Yingli doesn't seem to have a path to either improve margins enough to make a profit, or pay off debt. That's a recipe for disaster in an industry where technology is becoming more important than just the cost you can make a panel for.

How Yingli Green Energy got behind the 8 ball

Reporting losses if you're growing or developing new technology would be fine, but Yingli has bet on commodity solar panels, and that's not a recipe for long-term success in solar. If you look at competitors who are making money today, they have differentiated technology and strong balance sheets.

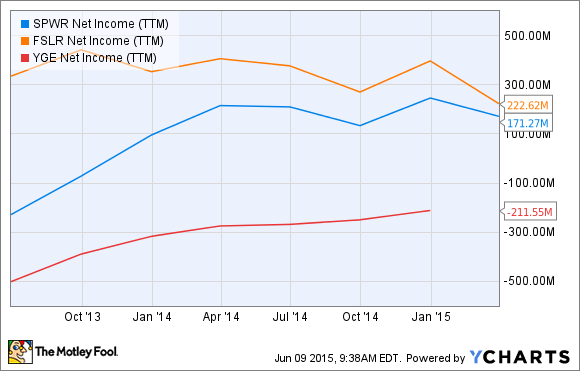

First Solar (FSLR +5.02%) and SunPower (SPWR +0.00%) are the two leaders in the space, and they're improving technology and value creation while Yingli Green Energy is losing money in the commodity solar panel market.

SPWR Net Income (TTM) data by YCharts.

Even SolarCity (SCTY +0.00%), who buys commodity solar panels, has shown that it sees technology as a differentiator long term. That's why it bought Silevo and is building its own manufacturing plant in New York. It doesn't want to be installing the same product everyone else is.

If Yingli isn't profitable with the product it has today, what is it going to do when competitors start building or buying more efficient solar panels. Yingli has no technological advantage to fall back on.

Yingli is set up for disaster

I don't see how Yingli Green Energy can dig out from under the debt it has on the balance sheet with the commodity business plan it has today. It may get a lifeline that could extend its life for a while, but before long, I think it will be in bankruptcy or insolvency, like previous companies that have led the world in solar manufacturing capacity.

For investors, this is one solar stock I would avoid despite the industry's strength in future years.