As a recent college graduate, I've faced many firsts: the first time I have to ask myself if things are age appropriate, the first time I have to think about retirement plans, and my first time furnishing an apartment. Fortunately, thanks to technology, furnishing an apartment is easier than ever. That's how I came across Wayfair (NYSE: W), a company you might not have heard of unless you're in the market for a seashell lamp.

Who is the player?

Wayfair is a Boston-based company founded in 2002 that has quickly grown into the second-largest online retailer of furniture, home décor, and housewares. The business is a marketplace structure in which over 7,000 manufacturers ship over 7 million products directly to the customer.

Wayfair operates the following websites: Wayfair.com, AllModern.com, JossAndMain.com, BirchLane.com, and DwellStudio.com. Each site has a specific distinguishing factor, from flash sales to specific styles. Additionally, the company also collects revenue from retail partners and Wayfair Media Solutions, which gives select manufacturers, retailers, and other advertisers access to a large customer base.

Going for the Gold!

- Growing top line

Since the company's inception 13 years ago, net revenue has grown at a compound annual rate of 69.2%. From fiscal 2013 to fiscal 2014, revenue increased 44%. As revenue increases from an increase in customers as well as number of purchases per customer, management continues to reinvest in the company to allow it to grow. While the 44% growth rate is certainly not sustainable forever, management has specific goals, including acquiring more customers, investing in consumer experience, increasing repeat purchasing, adding new suppliers, and investing into technology and operations. Additionally, Wayfair plans to continue expanding internationally, pursuing strategic acquisitions, and launching new brands.

- Capable management

For successful growth, the people in charge must execute well. Wayfair has a history of adapting. The company began by operating multiple furniture sites grouped by purpose (i.e., allbarstools.com). Later, management realized customers could access both targeted products and as inadvertent goods if the site was grouped by style rather than by purpose, so Wayfair reorganized.

Both co-founders, Niraj Shah and Steve Conine, remain actively involved with the company, including retaining voting control. Wayfair has also recently brought in outside experts, including Jeremy Delinsky as chief technology officer and Liz Graham as vice president of sales and services. Delinsky comes with over a decade of experience serving as CTO and chief product officer at an electronic health records software maker. Graham most recently headed information-technology operations at HubSpot, and before that spent 14 years at Comcast overseeing all aspects of customer service.

The scorecard so far...

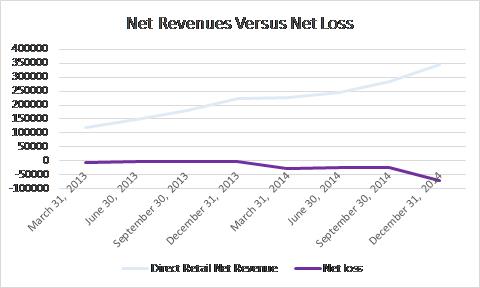

Over the last 12 months, Wayfair's retail net revenue has increased, driven largely by an increase in the number of active customers. The company now has about 3.2 million customers, a 53.78% increase from a year ago. While the number of customers is increasing, net revenue per customer per order has remained constant, with an average order just over $200. However, the number of orders per customer has also increased over an extended period of time. All of these numbers considered, one might expect the bottom line to grow as well.

However, the company has continued to operate at an increasing net loss. This net loss is a result of increased spending on advertising; merchandising, marketing, and sales; and operations, technology, and general and administrative expenses. All of those costs are aimed at driving revenue growth.

For example, in 2014, advertising expenses were about 14.5% of total revenue. Gross margin for 2014 was only about 23.5%. Although the high costs and smaller gross margin can be attributed to the increase in revenues, the company acknowledges that these percentage cannot continue forever. Once a substantial customer base is acquired and making repeat purchases, Wayfair plans to decrease its advertising expense. In the long run, Wayfair projects to have advertising expenses decrease to 6-8% and gross margins to increase to 25-27%.

Place your bets...

All things considered, Wayfair is focused on providing a broad selection of furniture at varying price points and styles to an international audience. Although the company is operating at a net loss, the competitive edge, top-line growth, and skilled management make Wayfair's future look much brighter than my apartment (which currently has no lamps).