This is what the industry would like you to believe is the face of for-profit education. Photo: Apollo Education Group.

Think that energy investors have had a tough year? Try being someone who invested in for-profit education at its peak in May of 2010.

While hindsight is always 20/20, few people saw the death of for-profit education on the imminent horizon. If they did, the stocks would have immediately gone to zero.

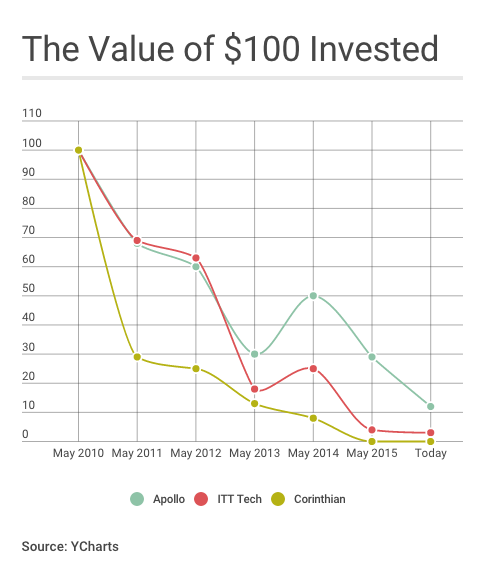

Instead, look at the steady deterioration you would have experienced if you invested $100 each in three of the largest for-profit educators at the time: Corinthian Colleges (NASDAQ: COCOQ), ITT Tech. (ESI +0.00%), and Apollo Education (NASDAQ: APOL) -- parent of the University of Phoenix.

Equal investments in these three would leave you with just $15 today. That's a total loss of 95% of your capital. But here's the kicker -- back then, the enrollment at these three schools was booming. Combining Apollo (459,000), Corinthian (112,000), and ITT (84,000), there were over a half-million Americans attending these schools -- all of which were growing.

But the seeds of destruction were clear for those who wanted to see it, and therein lies an important lesson for investors. The death of for-profit education is a good thing because fewer students will be saddled with debt and little to show for it. But it's also a triumph for our economic system, which -- eventually -- killed off an imminently fragile industry.

Skeptical from the get-go

As a former teacher, I wrote in 2011 that I'd be staying as far away from for-profit education as possible. I simply didn't think they were adding value to students. I followed that up 19 months later with a piece that bemoaned just how awful the industry was -- both as a service and an investment.

It turns out that my predictions came true -- but there are a few things I know now that I didn't then. After reading Nassim Taleb's Antifragile, I developed an entirely new way to evaluate investments -- and realized exactly why for-profit education was such a bad investment.

There are important lessons from the failure of for-profit schools for investors to heed when constructing their own portfolios.

Customer concentration risk

At first glance, it might seem ridiculous to say that for-profit schools had customer concentration risk. As I just pointed out, there were over a half-million students attending the schools. If one, or even 10,000 students decided that they were going to leave, there's no reason to believe that would mean the other students had to leave.

But here's the rub: Though students were the ones attending classes, it was the federal government that was footing the bill. This created a situation where the client (the students) and the customer (the federal government) were two entirely different entities.

How much of the money at these schools came from the feds? By 2012, federal loans accounted for more than 80% of the revenue at all three of these schools. The unrecognized risk was that one decision from one entity -- the U.S. Department of Education -- could remove funding overnight.

Indeed, that's basically what happened to both ITT and Corinthian. And recently, the Department of Defense announced that it was putting the University of Phoenix on probationary status for their recruiting techniques.

Investors in any industry need to carefully consider this risk. It can primarily be found in the company's annual report under "Risks."

A prime example would be component suppliers for popular products, like those offered by Apple. Because Apple has such high sales volume, having one's technology in an Apple product can be lucrative. But -- and here's the key -- such companies become much more fragile as a result.

Apple is the owner of the end product that's so popular with consumers. That's not the case for its suppliers. If someone comes along and offers Apple a component with the same functionality at a lower cost, a switch could be made overnight. Just like that, the previous supplier has employees firing up their resumes because they're out of business.

No skin in the game

Taleb argues convincingly that one of the greatest problems in modern society is that those in charge don't have enough skin in the game. By this, he means both exposure to financial upside if things go well, and exposure to downside risks if they don't. While the former is abundant on Wall Street, the latter simply isn't. One peek at the golden parachutes for the banking executives responsible for the Great Recession is all you need to see to understand the concept.

This was the case in for-profit education as well: incentives were misaligned up and down the industry. The government took on the risk for students enrolling who weren't ready, not the schools. Recruiters were (illegally) compensated for meeting recruitment quotas, with no downside risk if those students defaulted on loans.

And CEOs had scant skin in the game when it came to stock holdings in 2010. George Cappelli owned less than 1% of Apollo's shares outstanding, and 94% of what was reported were yet-to-be-exercised options. Jack Massimo owned 1.5% of Corinthian's shares, but 90% were also yet-to-be exercised options. And Kevin Modany owned 1% of ITT shares, with almost all actually being yet-to-be exercised options.

To be sure, this type of compensation isn't abnormal on Wall Street. But there's something to be said for an executive either having high ownership because he/she founded the company and has retained control, or because he/she made open-market purchases. That's true skin-in-the-game.

If you want to check insider holdings for your portfolio, go to the government's EDGAR database, type in your company's stock ticker, and search for the DEF 14A filing. You'll find all you need there.

Checking up on customer risk and skin-in-the-game

While the for-profit industry represents a perfect example of what can happen to investors when these risks are present, it certainly isn't limited to for-profit companies. Hopefully, this gives you two new tools and offers a different lens through which to measure risk in your own portfolio. You might be surprised by what you find.