Interest rates have been at extremely low levels for several years, repeatedly defying predictions by bond-market commentators expecting imminent increases. Those calling for higher rates finally got one of their wishes granted in December when the Federal Reserve made its first tightening of monetary policy in nearly a decade, but in general, interest rates stayed in a much narrower range than most had expected at the beginning of the year.

Short-term rates remained near zero

The Fed has the most control over short-term interest rates, and its decision to pursue a policy of keeping its target interest rate in a tight range between 0% and 0.25% during the first 11 months of the year was effective in keeping short-term rates low throughout the year. Only toward the end of 2015, when the Fed decided to raise its target range to 0.25% to 0.50% at its December meeting, did short-term rates rise.

3 Month Treasury Bill Rate data by YCharts

The consequence of low rates for consumers was mixed. For borrowers, low short-term rates kept down financing costs on credit cards and other loans with rates tied to the short-term bond market. For savers, though, low short-term rates kept returns on savings accounts and bank CDs down throughout the year.

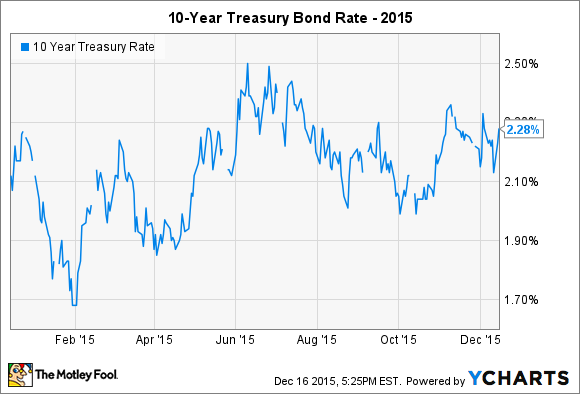

Long-term rates stayed relatively stable

Perhaps more surprising was the fact that longer-term bond interest rates also remained in a fairly tight range. After starting the year just above 2%, 10-year bond rates (TREASURY: TC10Y) reflected fears early in the year of a possible setback for economic growth, falling briefly as low as 1.7%. Yet as it became evident that the U.S. would escape some of the negative forces affecting the global economy, rates recovered, hitting a high of 2.5% near mid-year.

10 Year Treasury Rate data by YCharts

The stock market's swoon in late summer helped sent long-term Treasury rates back downward. By December, the yield on the 10-year Treasury ended up around 2.25%, as investors appeared comfortable that the Fed's decision to start lifting short-term rates would be slow and gradual enough to avoid immediate and sizable upward pressure on longer-term rates.

Inflation-indexed bonds saw a bigger rate increase

Interestingly, inflation has remained subdued, giving the Fed more flexibility in deciding when to start the process of raising rates. The rise in rates on inflation-indexed bonds, whose interest and principal payments automatically adjust to increases in inflation, was somewhat steeper than the traditional bond market, signaling that investors believed that inflation wouldn't be a major concern in the immediate future.

10 Year Treasury Inflation-Indexed Security Rate data by YCharts

At 0.8%, the inflation-indexed bond rate approached its highest point since 2013, and only a small increase from here would send rates to levels not seen since 2011. The combination of low traditional bond rates and rising inflation-indexed bond rates produces an inflation expectation that prices will remain in check for some time. Given the performance of the energy market, which is a prime determinant of prices throughout the economy, it's not surprising to have seen inflation have almost no influence on rates during 2015. The favorable trends that investors have seen on the inflation front could last well into 2016 barring a quick reversal in the downward trend in the crude oil and natural gas markets.

Mortgage rates kept homeowner borrowing costs low

Finally, on the borrowing side, most homeowners and new home-buyers benefited from continued low mortgage rates. Rates on the 30-year mortgage stayed in a fairly tight range all year, and while they rose slightly from where they began the year, 30-year rates nevertheless remained below the key 4% mark near year-end.

US 30 Year Mortgage Rate data by YCharts

2015 wasn't a hugely exciting year for interest rates, but that in itself was a surprising result, given the predictions for much higher rates that most market participants were expecting this time last year. Now that the Federal Reserve has begun the process of boosting the federal funds rate, bond yields could follow suit in 2016 and beyond. Yet most expect the moderate pace of monetary tightening to continue, and that could help keep any interest rate rise in 2016 from getting out of hand.