Eaton Corp, PLC (ETN +0.88%) is down over 30% from its early year highs. That makes sense since the industrial giant has been lowering its organic growth forecasts all year long. But there's still a lot to like here, including an over 4% dividend yield backed by fairly regular dividend hikes. Here are three reasons why Eaton Corp is a buy now.

Diversification

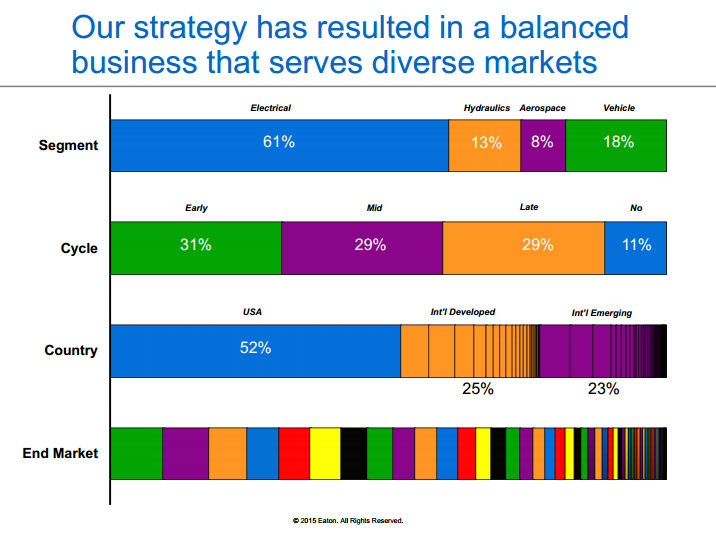

At one point in time, Eaton was focused on the auto business. But that's the old Eaton, the new Eaton is a power management business with its fingers in everything from autos to aerospace. This diversity is one of the top reasons to like the company.

Today electrical products make up around 60% of revenues, with hydraulics, aerospace, and automotive making up the rest. However, within the large electrical segment, there's really two businesses of roughly equal size, electrical products and electrical systems and services. The company has a global footprint and diverse customer base within each of these segments.

Eaton is big on diversification. Source: Eaton Corp.

Bu the company's diversification doesn't stop there. Although the U.S. is half the business, developed and emerging markets are each big contributors. And it's revenue is spread fairly evenly over the market cycle, too. So, one investment buys you a lot of diversification. Which helps explain why Eaton is still profitable despite the business headwinds it's facing.

Cash is king

The second reason to like Eaton is its ability to generate cash. For example, the company had operating cash flow of $973 million in the third quarter -- a quarterly record for the company. This even though earnings were down 25% year over year. So it's turning sales into cash even during a difficult spell.

Most investors look at earnings, and rightly so. But they aren't the only important metric and can be skewed by non-cash charges like depreciation and amortization. As a simple example, you won't find dividends on an earnings statement, they show up on the cash flow statement. That's because accounting earnings don't pay dividends, cash does.

Taking a deeper dive, through the first nine months of the year, Eaton's business generated roughly $1.6 billion in cash. Investing in and maintaining its business ate up around $370 million of that and $770 million went toward dividend payments. Although debt repayments and stock buybacks were $850 million over the span (eating into the company's cash balance, though shoring up the capital structure), both of those are somewhat optional so there's plenty of room to support the dividend and maintain the company.

ETN Dividend Yield (TTM) data by YCharts

The yield

The dividend is a key focus here because Eaton's yield is a generous 4.4% or so. That's on the high end of this company's historical range. But, as the cash flow statement shows, sustainable. The thing is, Eaton's yield seems out of line with competitors like General Electric (GE +0.40%) and ABB (ABB +0.67%), with yields of 3% and 3.3%, respectively.

Does that mean Eaton is the best business of the bunch, no. The company's operating margins have consistently trailed those of its peers. So a discount of some sort makes sense. But if you are an income investor, Eaton stands out in other ways.

For example, it has increased its dividend in eight of the past 10 years. Eaton appears to have ample cash flow to support and even grow the disbursement. And over the trailing 15 years, Eaton has grown its distribution roughly 15% a year. GE cut its dividend as a result of the 2007 to 2009 recession. ABB, while increasing its dividend on a regular basis since 2006, has an annualized dividend growth rate of around 12% over the past five years--Eaton's dividend growth over that span was nearly 14.5%.

So Eaton has paid a lot more attention historically to returning value to investors via distributions and that sets it apart from the pack. Moreover, with its shares down 30% from recent highs while the broader market flirts with record prices, it certainly appears that there's been a "bear market" in Eaton's shares.

GE's shares, for reference, have rocketed higher of late as it continues to sell off finance businesses. That looks more like investor euphoria over the company's restructuring than anything to do with the remaining business, which is facing the same economic headwinds as Eaton. And while ABB's shares are in the doldrums along with Eaton's, Eaton simply has a more compelling dividend profile.

An out of favor opportunity

All in, now looks like a good time to consider taking a position in Eaton. That's not to suggest that the tough business environment is set to change any time soon, which it won't. But that Eaton is strong enough to survive a bad market while paying investors well to stick around. This is a long-term bet on a great company that looks like it's temporarily out of favor with investors.