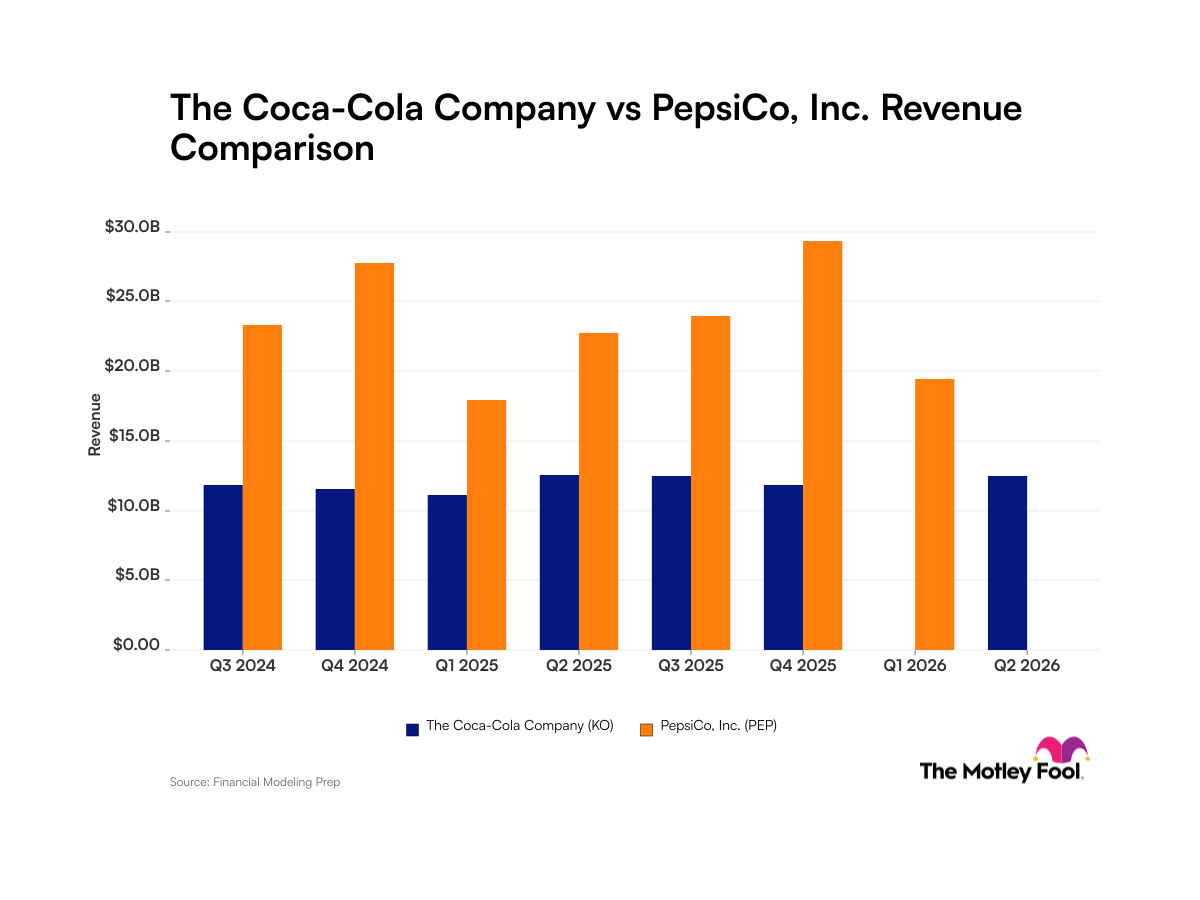

Get the heck out of America! No, this is not some xenophobic rant, but the reluctantly sensible advice that I think investors need to heed. PepsiCo’s (NYSE:PEP) second-quarter results represented the world in microcosm, with belt-tightening U.S. consumers hurting sales in the company’s North American beverage unit, while strength abroad lifted the company’s overall results to respectable levels, mirroring the results the Coca-Cola Company (NYSE:KO) reported last week.

Like Coke, Pepsi also benefited from the plummeting U.S. dollar, a phenomenon that I hesitate to label as either temporary or likely to reverse in the near future. Four percent of the 14% revenue growth the company achieved resulted from favorable currency benefits.

PepsiCo’s core results were impressive: 4% worldwide volume growth in snacks (those wonderfully awful-for-you Frito-Lay treats) and 5% volume growth in beverages. Comparable earnings per share increased 11%. On the whole, not too shabby.

However, while the company’s U.S. food results were decent, its American beverage performance was dismal enough to be alarming. North American beverage volume declined 3% in the quarter, with once high-flying noncarbonated beverages declining 4%, more than the 2% decline in their fizzy counterparts. Bottled water, which has been a growth driver in North America for several years, fell off a cliff. Volumes declined in the double digits.

What are Americans drinking instead of PepsiCo beverages? Tap water. In contrast, Frito-Lay’s rather inexpensive products have fared fairly well over the past few months, as there are few corn or potato chip faucets out there (though I have contacted a patent attorney, so don’t get any ideas).

This contrasting U.S. dynamic leads me to believe that the acid test for U.S. consumer products over the next few months will likely be whether consumers can find a company’s products cheaper somewhere else. If they can, consumers will probably migrate away from a certain brand for a comparable product sold for a lower price. If they can’t, then they’ll just have to swallow the increase and take the pocketbook hit as rising commodity costs are leaving Pepsi and its fellow drink manufacturers, like Dr. Pepper Snapple Group (NYSE:DPS) and Hansen Natural (NASDAQ:HANS), with no choice but to raise prices.

With PepsiCo shares currently trading at 18 times management’s earnings-per-share guidance of at least $3.72 for 2008, the shares seem fairly priced. PepsiCo management is usually pretty good about managing expectations, so I would not be surprised to see the company beat by a few cents. With the worst of commodity costs expected to hit in the third quarter, investors might be able to take advantage of a stock price decline to load up on a company that I think is a great long-term investment.

Related Foolishness: