Image source: Getty Images.

Social Security provides the bulk of retirement income for millions of benefit recipients, and those who earn relatively little during their careers tend to rely on Social Security even more. By contrast, if you have a high income, you can generally afford to save in a 401(k) or other retirement account to supplement your Social Security. Nevertheless, even though Social Security is set up to replace a smaller percentage of pre-retirement income for high-income earners than for low-income earners, those who make healthy salaries can expect to get substantial benefits when they retire. Below, we'll use the example of seeing how much someone making $120,000 per year can expect from Social Security at retirement.

High-income earners and Social Security's wage base limit

As it happens, workers making $120,000 per year won't have all of their income taxed by Social Security. Social Security imposes payroll taxes only on amounts up to the annual wage base limit, which for 2016 is $118,500. As a result, someone making $120,000 would pay 6.2% in payroll tax toward Social Security on the first $118,500, or $7,347. The remaining $1,500 would go untaxed.

Because not all of your income will be subject to payroll taxes, you also won't get credit for all of your wages for purposes of determining benefits. The same maximum of $118,500 will apply in setting your creditable earnings for 2016.

It's a marathon, not a sprint

To determine how much you'll get from Social Security, a single year doesn't play a very important role. The Social Security Administration looks at your entire earnings history, taking your wages and salaries from the 35 top-earning years of your career after adjusting for inflation and then figuring the average from those 35 years. If your career was shorter than 35 years, then the SSA puts in zeros for the years you didn't work.

Therefore, if your $120,000 in earnings in one year was a fluke and you typically make much less, then you won't be able to determine your benefits easily just from knowing that one year of your career history. That's where Social Security differs from some private pensions, which might look at only two or three of your best years in terms of income.

Maxing out on Social Security

Many people who earn $120,000 will have similarly high incomes going back in time. If that's the case, then there's a possibility that you'll earn at or above the maximum wage base limit each and every year for 35 years. For those people, Social Security gives you an easy answer for what to expect from benefits by providing the maximum possible monthly benefit.

For someone retiring at full retirement age in 2016, the maximum benefit would be $2,639 per month, again assuming that you had 35 years of earnings that maxed out Social Security payroll taxes. Those figures differ slightly every year, because of changes in the wage base maximum and any cost of living adjustments that might apply. For 2015, for instance, the corresponding maximum was $2,663, and the 2014 maximum was $2,642.

If you retire at a another age, your benefit will be different. For example, someone turning 62 in 2016 and taking Social Security will receive just $2,102 per month. If you wait longer to get benefits, you'll get even more. The maximum for someone taking benefits at age 70 in 2016 is $3,576 per month.

An early retirement benefit

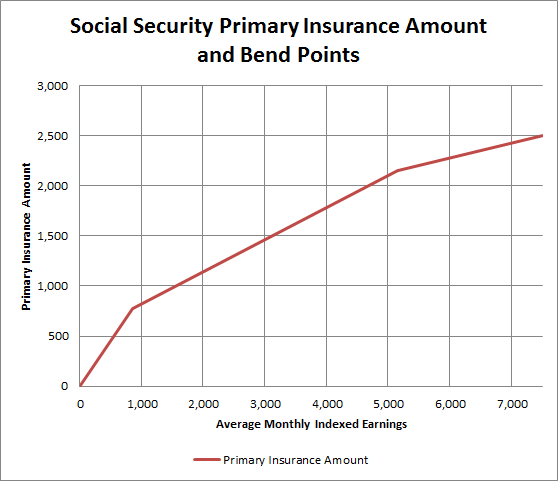

Finally, high-income individuals should understand that the way that Social Security is calculated gives them a disproportionate advantage if they choose to retire after a short career. The formula for determining the primary insurance amount that helps in figuring your monthly check looks at your average indexed monthly earnings over those 35 highest-earning years. But it also builds in a series of what are called bend points to give lower-income workers more replacement income than higher-income workers. For the first $856 in monthly earnings, you get 90% toward your primary insurance amount. From $856 to $5,157, you get 32% added to the figure, and above $5,157, each extra dollar gets you $0.15.

Image source: Author.

What that means is that if you retire early after a short career, you'll get a much higher benefit than you might think. As an example, say you work for 17.5 years at maximum income and then retire early. Your average indexed monthly earnings would therefore be half what they would be if you worked a full 35-year career. But because of the bend points, your monthly benefit would still be around two-thirds of what it would be if you hadn't retired early.

In general, those who routinely have high incomes will fare quite well under Social Security. You won't come close to replacing $10,000 per month in wage income, but what you do receive from Social Security will be a nice addition to any retirement savings that you've set aside on your own behalf.