Image source: Getty Images.

Claiming Social Security is one of the most important financial decisions you'll ever make. Many Americans prefer to turn to the Social Security Administration for help in figuring out when to take their Social Security benefits, and the SSA provides a lot of valuable information both on its website and through its personnel. Yet a recent study from the General Accounting Office took a closer look at the way that the SSA interacts with people filing for Social Security benefits, and it found that in the process of handling in-person claims, the SSA's claims specialists didn't always provide all the key information that people need in order to make an informed choice. Below, we'll look at six key aspects of Social Security for which you might not get the facts you need from SSA personnel.

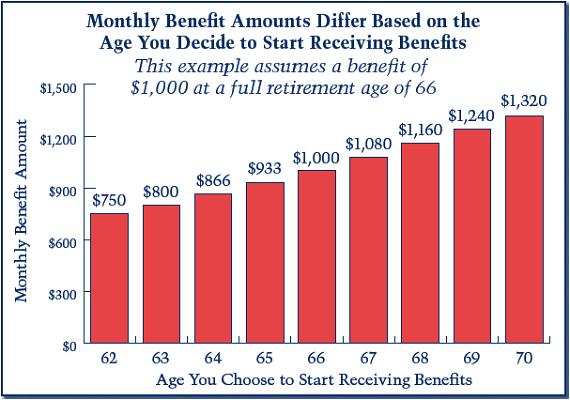

1. How claiming age affects monthly benefits

You can claim retirement benefits at any time between age 62 and age 70, and when you claim makes a huge difference in the size of your monthly Social Security check. Claim at 62, and you'll get 25% less than you would at full retirement age of 66. Claim at 70, and you'll get 32% more. All told, that adds up to a potential swing of as much as 76% in the size of your monthly benefit.

Image source: SSA.

The GAO study found several departures from established procedure among claims specialists discussing the impact of age on benefits. Almost a third of interviews didn't include discussions of how waiting can boost the size of your monthly check, and only half presented the three calculations that the SSA's Program Operations Manual System calls for: your benefit at age 62, at full retirement age, and at age 70. In addition, some claims specialists discussed break-even analysis, an issue that the operations manual specifically tells personnel not to talk about with claimants. Knowing the facts about your benefit amount is important to avoid confusion in dealing with SSA personnel, some of whom might have their own opinions about the ideal age to claim your Social Security.

2. How lifetime earnings affect Social Security benefits

The SSA bases your Social Security benefit amount on your earnings history. Specifically, the SSA looks at the 35 top-earning years after adjusting your wages and salary income for inflation. Then, a series of formulas determines your primary insurance amount, which in turn gets adjusted depending on when you claim.

The GAO study found that only about one in four interviews included discussion of how earnings affect benefits. It concluded that in some cases, especially for those who had fewer than 35 years of work experience, understanding the rule could let claimants make a better-informed decision.

3. What spousal benefits are available

Married people have the ability to receive retirement benefits based on their own work history or spousal benefits based on their spouse's work history. Although the ability to claim one benefit while leaving the other has been severely limited by recent legislation, there are still some cases in which a spouse can use strategies to maximize their total benefits.

The GAO study found that in several instances, claims specialists didn't mention that special strategies were available to boost the total benefit amount. In contrast, the study noted that the specialists who did mention those strategies helped lead claimants to make decisions that increased their own benefit by taking their smaller spousal benefit first.

Image source: SSA.

4. The impact of the earnings test on Social Security benefits

If you claim Social Security benefits before reaching full retirement age, then you can forfeit your benefits if your earnings are above certain threshold amounts. In 2016, for every $2 people who will be younger than age 66 at the end of the year earn above $15,720, they'll lose $1 of annual Social Security benefits.

SSA personnel did a good job of explaining that part of the earnings test. However, in more than a third of interviews, they didn't explain that benefits withheld under this rule would potentially lead to a recalculation of monthly benefits after the claimant reaches full retirement age. The recalculation essentially returns forfeited amounts over time, and that's an element of the test that many people don't understand.

5. How Social Security benefits get taxed

Social Security benefits can be subject to income taxation under certain circumstances. To determine taxability, you have to take your total income, including wages, investment income, taxable withdrawals from retirement accounts, and other types of income. Then add in one-half of your Social Security. If the total exceeds $25,000 for single filers or $34,000 for joint filers, then a portion of your benefits can be subject to tax.

That fact didn't usually come up in interviews with SSA personnel. The manual specifically states that claims specialists should not answer tax questions, referring them instead to IRS publications about Social Security and taxation. Yet that only serves to confuse some claimants.

6. How Social Security can address longevity risk

Finally, one of the biggest benefits of Social Security is that it pays benefits for life, no matter how long you live. That can be especially important for those with limited financial resources, and Social Security can end up being the only source of income once other funds run out.

Surprisingly, health and longevity came up in less than 10% of interviews, and then only because the claimants themselves asked questions. The study believes that providing more information could give recipients a better basis for considering when to claim.

Social Security is complicated, and expecting a perfect performance from SSA personnel is unrealistic. Nevertheless, by following the conclusions of the GAO study, Social Security could do a better job of giving retirees the facts they need to be smarter about their benefits.