A 401(k) can be a great home for your retirement savings, but to get the most out of yours, you have to understand how it works. It's also important to make sure you're eligible for your workplace's 401(k) and have a backup plan if not so you are still able to save for your future.

Here's a closer look at everything you need to know to open and maintain your 401(k), or choose a different retirement account if a 401(k) isn't available to you.

What's so great about 401(k) accounts?

What's so great about 401(k) accounts?

A 401(k) is a popular type of employer-sponsored retirement plan that's available to all employees 21 or older who have completed at least one year of service with the employer, usually defined as 1,000 work hours in a plan year. Some employers enable new employees to join right away, even if they haven't met this criterion yet.

In 2023, you're allowed to contribute up to $22,500 to a 401(k), or up to $30,000 if you're 50 or older. In 2024, those amounts rise to $23,000 and $30,500, respectively. These limits are much higher than what you find with IRAs, and they enable you to set aside a fairly large sum annually.

Most 401(k)s are tax-deferred, so your contributions reduce your taxable income each year. You must pay taxes on your distributions in retirement, but you may be in a lower tax bracket by then, in which case you would save money. Some employers also offer Roth 401(k)s. You pay taxes on contributions to these accounts now, but you'll get tax-free withdrawals in retirement.

Some employers also match a portion of their employees' 401(k) contributions, which can make the task of saving for retirement a little easier. Each company has its own rules about matching, so consult with your HR department to learn how yours works.

How do you open a 401(k)?

How do you open a 401(k)?

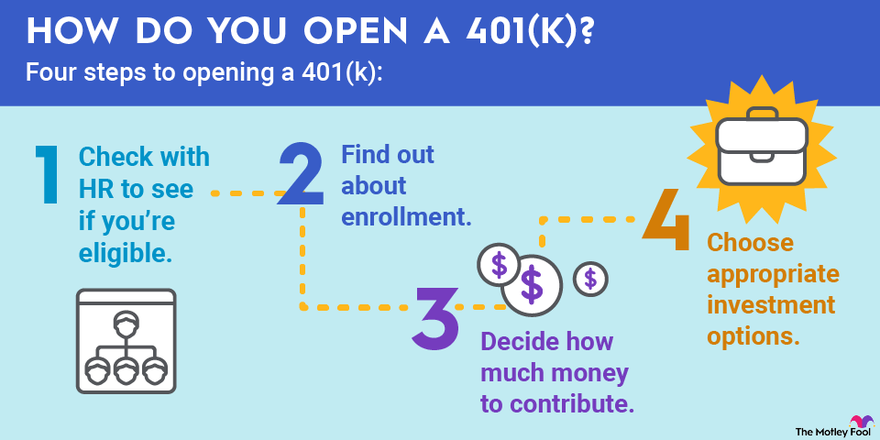

Do the following to open your 401(k):

- Figure out if you're eligible. Check with your HR department to see if you can sign up right away or if you must wait.

- Find out if you have to do anything to enroll. Some employers automatically enroll eligible employees in the plan.

- Decide how much money you plan to contribute. Ideally, you'll base this amount on your estimate of how much you need to save monthly to retire comfortably. You can usually choose between contributing a set dollar amount and contributing a percentage of each paycheck.

- Choose appropriate investment options for your contributions. Focus on finding a low-fee option, such as index funds and ETFs, and make sure you keep your money diversified between stocks and bonds and among many sectors to better shield you from significant loss.

Talk to HR about enrolling in your 401(k)

Talk to HR about enrolling in your 401(k)

If you're interested in opening a 401(k), talk with your employer to learn about how your company's plan works. If your employer automatically enrolls employees and withholds a default amount of their paychecks, you can change the amount yourself at any time. You can also opt to stop contributing to the plan if you're not interested in doing so right now.

Other companies require participants to declare their desire to participate in the 401(k). You'll have to fill out paperwork saying that you'd like to contribute to the plan and how much money you'd like to set aside initially. You can always change this later.

You'll also need to choose your beneficiary -- the person you'd like to inherit your 401(k) if you die -- when you sign up. Usually you choose a primary beneficiary and a secondary, or contingent, beneficiary who will inherit the 401(k) if the primary beneficiary is deceased or doesn't want the money.

What if I don't have access to a 401(k)?

What if I don't have access to a 401(k)?

If you don't work for a company that offers a 401(k), you can save for retirement using one or more of these other accounts:

- 403(b): A 403(b) is similar to a 401(k), but it's available only to public school employees, select ministers, and employees of tax-exempt organizations.

- SIMPLE IRA: A SIMPLE IRA is designed for self-employed individuals and small business owners. It offers fairly high contribution limits and has mandatory contribution requirements for employers.

- SEP IRA: A SEP IRA is available to self-employed individuals with or without employees. Contribution limits depend in part on annual income.

- Solo 401(k): A solo 401(k) is simply a 401(k) that a self-employed person can open for themselves. Contribution limits are higher than for traditional 401(k)s because you can make contributions as both employee and employer.

- IRA: Anyone can open and contribute to an IRA if they're earning income throughout the year, but these accounts have more restricted contribution limits.

Related retirement topics

How to maintain your 401(k)

How to maintain your 401(k)

You can't just forget about your 401(k) after you've set it up. You must regularly revisit it to determine if you need to make any changes to your contribution amount or to your asset allocation. Check on your plan at least once or twice per year or following any major life event that could affect your finances or retirement plans.

First, look at how your investments are performing. Small losses here and there are to be expected, especially if you have a lot of your money invested in stocks. However, if you're routinely losing money, that's a sign something needs to change. You may also want to consider moving some of your money around if it's underperforming major market benchmark indexes, such as the Dow Jones Industrial Average and the S&P 500. In this case, switching to an affordable index fund that tracks these benchmarks may provide better and more predictable returns.

You should also evaluate how much money you're contributing to your 401(k). Income usually rises over the course of one's career, so you may feel more comfortable contributing more of each paycheck as your income grows. Some people choose to start small and increase their contributions by 1% of their salary every year until they reach their goal amount.

Be smart with your 401(k)

Opening a 401(k) is a smart step on the road to a comfortable retirement, but it's not quite as simple as signing some papers and setting aside a percentage of your paycheck. You have to understand the rules, choose your investments wisely, and continue to maintain your plan for as long as you own it. If you do that, you can feel confident that you're giving yourself the best shot at a secure retirement.