Source: SSA.

Just about every current and former American worker wants Social Security to be there to provide valuable benefits to them and their families after they retire. Yet amid renewed concerns about the financial stability of the Social Security program, debate has heated up over whether Social Security taxes impose a proper burden on people at all income levels. As calls for moves like raising or eliminating the current $118,500 wage-base ceiling on Social Security taxes get louder, many of those on both sides of the debate don't fully understand the way in which Social Security already has elements that lead to some wealth redistribution among its recipients.

The controversy over Social Security taxes

A recent report from the Center for American Progress tackled the topic of income inequality and its impact on the Social Security system. The report noted the fact that Social Security only imposes taxes on earned income from wages, salaries, and self-employment income, leaving investment income like capital gains, dividends, and interest untaxed. In addition, it argues that as income has become less equally distributed, more of the nation's total income has gone untaxed due to the wage-base ceiling. The report concludes that what it sees as fairer taxation would have left the Social Security trust funds in stronger financial condition than they are now.

Still, one element that the report only glosses over is the fact that Social Security structures its benefits in a way that helps to even out income inequality. Specifically, the formula that calculates Social Security benefits leads to low-income individuals having a greater percentage of their earnings paid in benefits than middle- and upper-income workers. Let's take a closer look at exactly how this mechanism works.

Source: SSA.

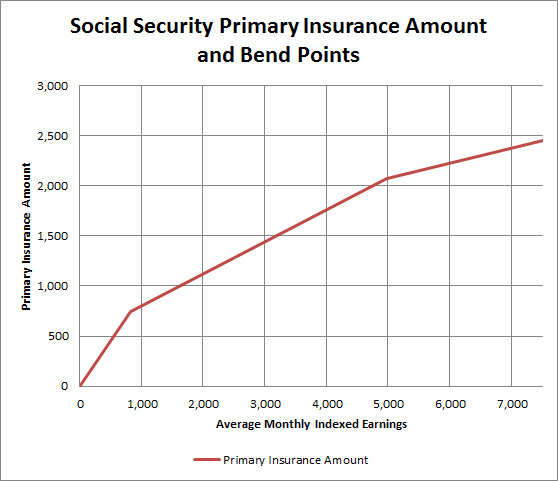

Understanding the Social Security bend points

Social Security's redistributive effect stems from the difference between how it collects tax revenue and how it pays benefits. Workers pay Social Security taxes in direct proportion to how much they earn, with the 6.2% tax starting on the first dollar of earned income and going all the way up to the wage-base limit set annually. As a result, someone who earns $100,000 a year will pay double the taxes of someone who earns $50,000. But the benefits that workers receive from Social Security, while based on lifetime earnings, don't work the same way. Therefore, while the $100,000-per-year worker will get more in benefits than the person earning $50,000, the higher benefit will be less than double the lower benefit. In this hypothetical scenario, tax money will be redistributed away from the $100,000 earner toward the $50,000 earner, and that's essentially how the Social Security system works at a larger scale.

The source of this redistributive effect is the formula for calculating the primary insurance amount, which determines your retirement benefit. First, Social Security figures out your average indexed monthly earnings, which makes inflation adjustments to prior years' income. But then, the benefit varies depending on your income level. In 2015, recipients who retire at full retirement age get 90% of the first $826 of their average earnings in monthly benefits. For earnings between $826-$4,980, Social Security adds 32% of the amount within that range to benefits. Finally, anyone earning more than $4,980 has 15% of the excess amount added to the primary insurance amount.

Source: Author calculations based on SSA formula.

To understand better how this works, let's take three workers: Pat, Chris, and Terry. To keep the example as simple as possible, we'll assume that all three had careers lasting 35 years and had constant earnings after adjusting for inflation. Pat earned $10,000, Chris earned $30,000, and Terry earned $90,000.

When you plug these earnings into the primary insurance amount formula, this is what you get:

|

Worker (Annual Earnings) |

Primary Benefit Amount |

% Higher Than Pat |

% Higher/Lower Than Chris |

|---|---|---|---|

|

Pat ($10,000) |

$746 |

- |

(42%) |

|

Chris ($30,000) |

$1,279 |

71% |

- |

|

Terry ($90,000) |

$2,451 |

229% |

92% |

Source: Author calculations based on SSA formula.

As you can see, the increases in benefits as income rises are far lower than the increase in average wages. Chris earns three times as much as Pat -- and pays three times as much in Social Security taxes during their respective careers -- but Chris's benefits are only 70% higher than Pat's. Similarly, Terry earns nine times as much as Pat but gets just over triple Pat's benefits. Even higher up the income scale, Terry gets less than double the benefits that Chris does despite paying triple the Social Security taxes. The net impact is to redistribute some of the tax money that higher-income earners paid into the system to lower-income earners' benefits.

Obviously, different people can draw different conclusions about what amount of redistribution is appropriate. Those who see Social Security's primary purpose as being a safety net will favor more redistribution, while those who see the program more like a private retirement plan won't want to see any redistribution at all. The key point, though, is that Social Security as it currently runs is not neutral in terms of income inequality and wealth redistribution, and so those proposing changes have to consider that starting point in evaluating what impact those changes would have.

Social Security is a vital part of retirement security for millions of Americans, and so it's essential to ensure the viability of the program. Yet it's easy to draw erroneous conclusions about how best to fix Social Security if you don't understand the details of the program currently.