How does a 403(b) loan work?

When you decide to take a loan from your 403(b), you'll need to talk to your plan administrator and sign a loan agreement. The loan agreement should detail the terms of the loan -- how much interest you'll pay and how long you'll have to pay back the loan.

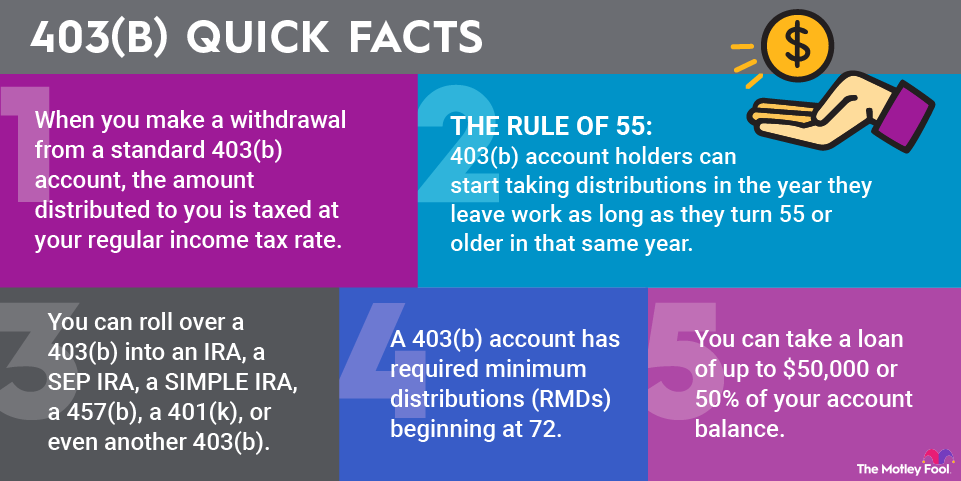

The IRS puts a limit on how much you can loan yourself. The IRS limits the amount to 50% of your vested account balance or $50,000, whichever is smaller. If you have less than $10,000 in your account, the IRS permits you to take the full balance as a loan. Certain plans may have stricter limits.

The IRS also stipulates that the loan must be repaid in equal payments occurring at least quarterly, and that it must be repaid in full within five years. Again, individual plans may have stricter rules.

Once you've taken your withdrawal, you can use the cash for whatever you need. In the meantime, you should be enrolled to make regular loan repayments from your paycheck equal to the minimum payment required to meet the terms of the loan agreement.

Unlike regular contributions to your 403(b), loan repayments do not count toward your contribution limits. The contribution limit for 2025 is $23,500, and increases to $24,500 in 2026.

In 2025, workers ages 50 to 59 and 64 and older can contribute up to $31,000 to a 403(b) with catch-up contributions, which increases to $32,500 in 2026. Those between the ages of 60 and 63 are eligible for an even higher limit, bringing the maximum 2025 contribution to $34,750 and the maximum 2026 contribution to $35,750.

Furthermore, the interest portion of the loan payment is paid with after-tax dollars, whereas regular contributions are typically pre-tax dollars.

If you have the cash to repay the loan early, you can talk to the plan administrator about creating a payoff statement to pay the remaining balance.