Can you invest your HSA money?

In some cases, it is possible to invest your HSA money. However, many HSA administrators require a minimum balance in your account before allowing you to invest.

Check with your HSA administrator to find out if you must meet any minimum threshold requirements in your HSA before you can invest.

Why should you invest your HSA money?

If you find out you can invest your money, the next big question is whether you should.

HSAs were established primarily to pay for your health expenses with pre-tax dollars if you have a high-deductible health plan. But they are also excellent retirement savings accounts with important benefits.

Arguably, the biggest upside for HSAs is that they offer a triple tax advantage:

- You don't have to pay federal income tax on your contributions.

- You won't be taxed on withdrawals for qualified medical expenses.

- Your earnings from investments won't be taxed.

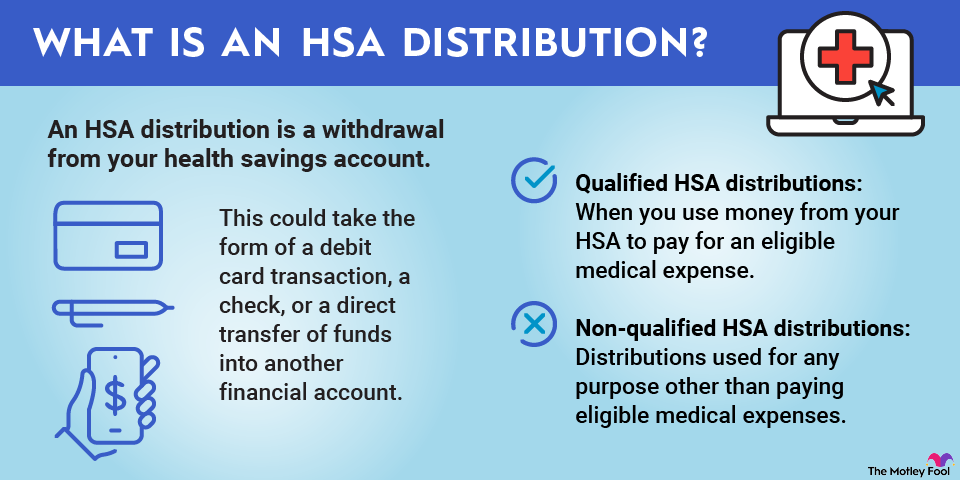

You benefit from the first two tax advantages even if you don't invest your HSA money. However, if you do invest your HSA money, the third advantage helps you as well.

There is a caveat to this advantage, though. If you withdraw HSA money before you turn 65 for reasons other than qualifying medical expenses, you'll be taxed at your ordinary income tax rate. You could also incur an additional 20% tax penalty on HSA distributions for non-qualified reasons.

Investing HSA money can be an especially attractive option for some. If you have maxed out your other tax-protected retirement savings account contributions and you still have additional money to invest for retirement, HSAs provide a great way to boost your overall retirement savings.